HeliRy

YPF Sociedad Anónima (NYSE:YPF) is an Argentine integrated oil and gas company that has long been somewhat controversial in the investing community. The traditional fossil fuel industry has surprisingly not attracted as much attention from many investors as we would think over the past year despite being by far the best-performing sector and one of the only ones to deliver a positive return. As a result, most energy companies are incredibly cheap, and YPF is certainly not an exception to this. In fact, as we will see in this article, it is almost ridiculously so. Although there are some risks associated with the firm, it may be worth considering for investment as it has significant growth potential over the next few years.

About YPF Sociedad Anónima

As stated in the introduction, YPF Sociedad Anónima is an Argentine integrated oil and gas company. It is by far the largest company in Argentina in terms of revenue and has been a major part of the country’s economy for about one hundred years. As such, it was deemed to be critical for national security, and the Argentine government owns 51% of the outstanding shares. This is an ownership structure that will certainly make many American investors nervous, although it is relatively common in many other countries around the world.

Unlike what we see with many European energy companies that also have government control, in the case of YPF its ownership by Argentina has proven to be both a positive and a negative over the years. One reason for this is that Argentina has had a number of financial crises over the years as the government has defaulted on its debts nine times over its relatively short history (it formally gained independence in the 1810s). The nation also has a history of military coups and government instability, which would certainly represent a risk to any investment in the country.

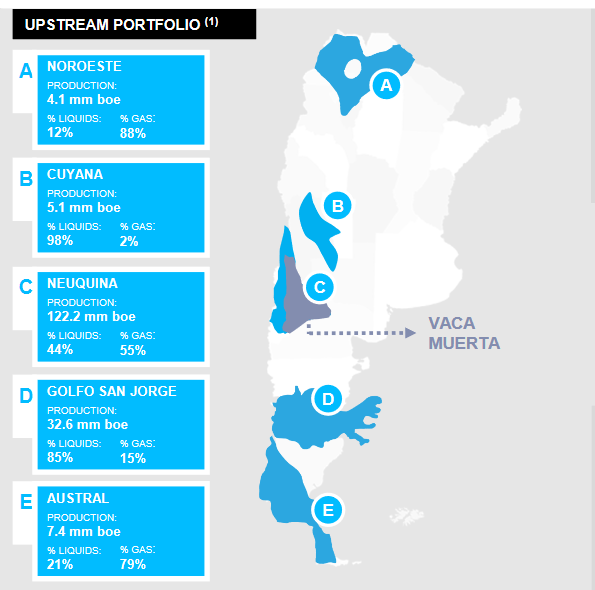

Despite the risks though, YPF certainly has a lot of potential due to the enormous resource reserves possessed by the South American nation. According to the U.S. Energy Information Administration, Argentina has the fifth largest oil and gas reserves in the world. A significant percentage of these are in the Vaca Muerta Basin, which is believed to be the second-largest deposit of shale oil in the world, after the Eagle Ford Shale in Texas. The United States and Argentina together hold about 38% of the world’s shale oil reserves. The Vaca Muerta is not the only hydrocarbon deposit in the nation, either. In fact, YPF holds interests in five different deposits throughout the country:

YPF Investor Presentation

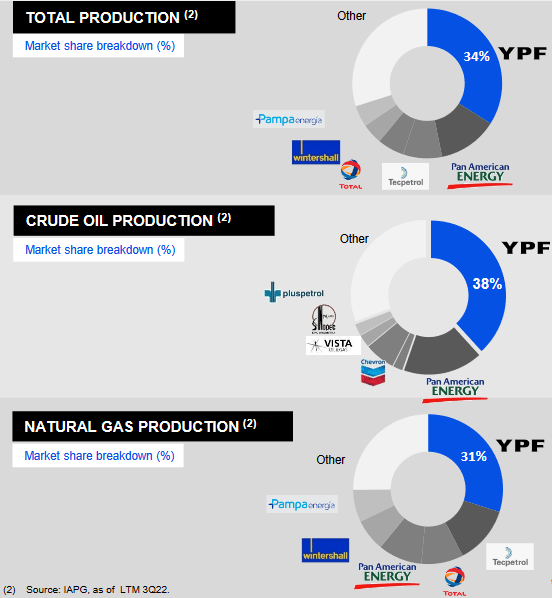

As might be expected for a government-controlled energy company, YPF holds interests in every major oil project that occurs in the nation. In fact, the company produces 38% of all crude oil and 31% of all natural gas extracted in Argentina:

YPF Investor Presentation

This is a very good position to be in today. As everyone reading this is no doubt well aware, the price of crude oil has risen substantially over the past twelve months. As of the time of writing, West Texas Intermediate crude oil is up 7.58% over the past year following a steep decline in the second half of the year:

Business Insider

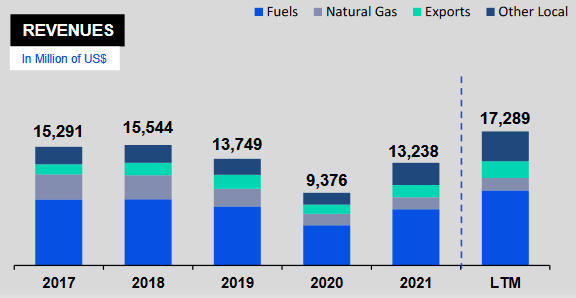

YPF is not able to realize these prices, though. One reason for this is that Argentine oil sells at a discount to West Texas Intermediate crude oil. This discount currently averages about 20% but it has been as high as 40% in the past. However, a more important thing that has been preventing YPF from fully exploiting the improvements in the energy pricing environment lately has been price controls imposed by the Argentine government on crude oil and gas. This is not an “official” government policy, but the government is running policies that result in oil and gas being sold at a very large spread to world energy prices as it is attempting to counter the impact that high energy prices have on the economy. As a result, YPF’s revenues have not increased by nearly as much as those of most other traditional companies over the past year:

YPF Investor Presentation

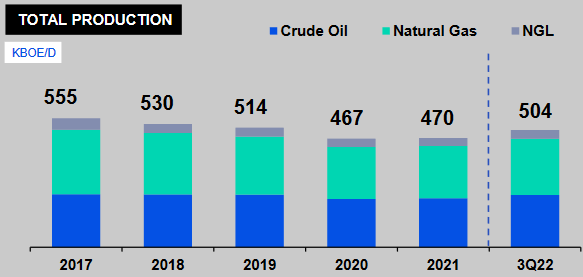

This is probably one reason why the company has not grown its production very much despite its substantial reserves. As we can see, YPF has generally kept its production flat-to-declining regardless of energy prices:

YPF Investor Presentation

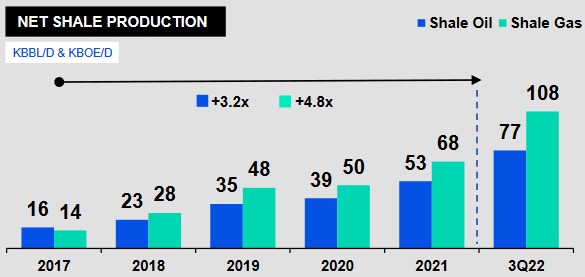

At this point, many readers will likely point out that this does not look like a very good energy investment. Indeed, if it did not have a catalyst to change the situation, then I would agree with that sentiment. This catalyst comes from the company’s large position in the Vaca Muerta shale plays, which YPF has just begun to develop. The company has been aggressively increasing its production in this region over the past few years:

YPF Investor Presentation

It is currently working to expand this further. The reason that this becomes a catalyst for growth is that the company can begin exporting this oil. YPF has already indicated that by the end of 2023, the company will be producing more shale oil than it can refine. The nice thing about oil exports is that YPF will be able to avoid the government’s de facto price controls and sell crude oil at world prices, which are considerably higher. YPF has projected that it will generate an extra $300 million in 2023 revenue and $4 billion in 2026 revenue at $90 crude oil.

I somewhat doubt that things will play out that well for the company, as $90 per barrel West Texas Intermediate seems very optimistic for 2023 given the potential for the United States and Europe to enter into recessions in the very near future. That may be reasonable for 2026, though, which we will discuss in just a few minutes. We need to keep in mind that Argentine crude oil sells at a discount to West Texas Intermediate as well, which will reduce YPF’s ability to fully capture the world oil price. It is uncertain whether or not the company took this into account when crafting its estimates and if it did, what discount it used.

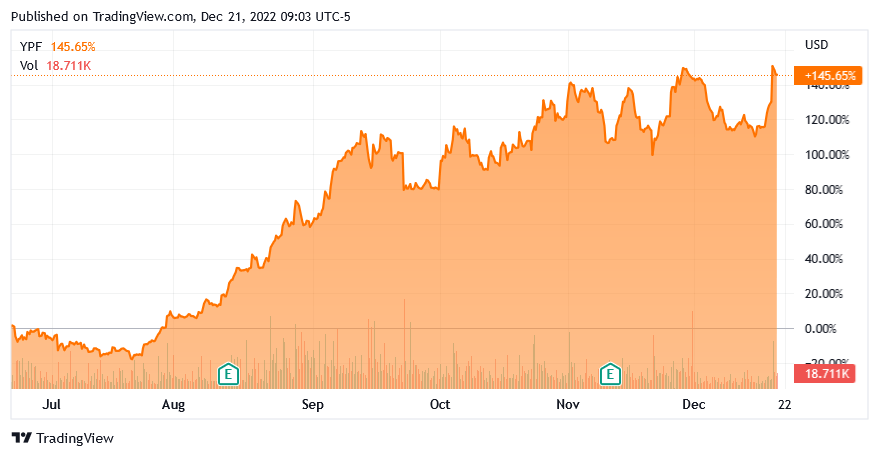

As mentioned earlier, Argentine crude typically sells at a discount of 20% to West Texas Intermediate crude oil, but it has sold at larger discounts in the past. Either way, this scenario would increase far more than revenues as it should have a positive impact on cash flow and EBITDA, too. This is likely why the company’s stock has appreciated by 145.65% in the past six months despite oil prices declining over that period:

Seeking Alpha

This steep appreciation does not mean that the stock has become expensive, though. In fact, it looks very cheap. There may be reasons for that though beyond the general risks related to the Argentine government so let us investigate further.

Fundamentals Of Crude Oil

Contrary to what politicians and environmental activists want you to think, the global demand for crude oil and natural gas is not going anywhere. In fact, the fundamentals point to both rising demand and rising prices going forward. According to the International Energy Agency, the global demand for crude oil will increase by 7% and the global demand for natural gas will increase by 29% over the next twenty years:

Pembina Pipeline/Data from IEA

Perhaps surprisingly, the natural gas demand growth will be driven by international concerns about climate change. These concerns have induced governments all around the world to impose a variety of incentives and mandates that are meant to reduce the carbon emissions of their respective nations. Among the most common of these incentives is encouraging utilities to retire old coal-fired power plants in favor of renewables. Unfortunately, renewables are a flawed solution because they are quite unreliable. After all, wind power does not work when the air is still and solar power does not work at night. Battery technology is nowhere near capable of overcoming these problems so the usual solution is to supplement renewables with natural gas turbines. This is because natural gas produces much fewer carbon emissions than other fossil fuels and has the reliability to ensure the “always-on” performance that we have come to expect from the electric grid.

The case for crude oil may be more difficult to understand as many Western governments have been actively attempting to discourage the consumption of crude oil. However, it is a very different story in the various emerging nations around the world. These nations are expected to see tremendous economic growth over the projection period, which will have the effect of lifting the citizens of these nations out of poverty and putting them firmly into the middle class. These newly middle-class people will naturally begin to desire a lifestyle that is much closer to that of their Western counterparts than they have now. This will require increased consumption of energy, including energy derived from crude oil. As the populations of these nations are higher than those of the developed nations, the growing crude oil consumption in these regions will more than offset the stagnant-to-declining production in the world’s wealthier nations.

This would seem to create an opportunity for oil and gas companies to increase their profits by simply increasing their production and selling into this rising demand. This is highly unlikely to happen, however. The oil and gas industry is under tremendous pressure from politicians and activists to improve its sustainability and from shareholders to increase its returns. The energy industry has also taken a few blows over the past decade as there have been two commodity price crashes. This generally resulted in the industry significantly underinvesting in production capacity. According to Moody’s, the industry must increase upstream spending by $542 billion in order to avoid a supply shock. There is no reason for it to increase spending to this degree given the aforementioned pressure. In addition to all of this, we are seeing disappointing production in areas like Norway that have actually been working to increase their output. Thus, it seems almost certain that the demand growth for crude oil will exceed the supply growth, which economic law tells us results in rising prices. This will naturally benefit YPF, particularly as it grows its shale production and begins exporting. In fact, Argentina is one of the only nations in the world that actually can increase its production so the company might be uniquely positioned to take advantage of the current situation.

Financial Considerations

It is always critical that we examine the way that a company finances itself before investing in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid. As this is typically accomplished by issuing new debt to repay the maturing debt, a company’s interest expenses can increase following the rollover depending on conditions in the market. In addition to this, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a firm’s cash flows to decline can push a company into financial distress if it has too much debt. Given the volatility of commodity prices, this can be an especially big risk for an energy company.

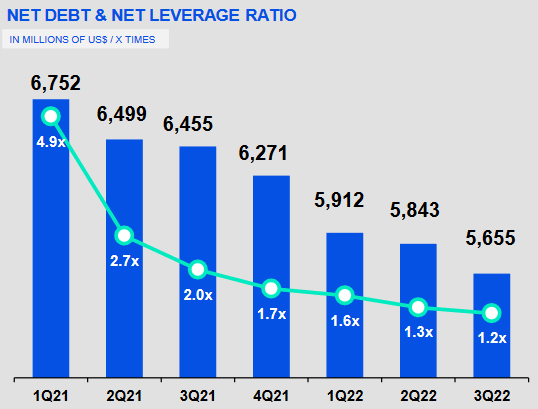

One metric that we can use to evaluate a company’s debt load is the leverage ratio, which is also known as the net debt-to-EBITDAX ratio. This ratio essentially tells us how many years it would take a company to completely pay off its debt if it were to devote all of its pre-tax cash flow to that task. YPF currently has a leverage ratio of 1.2x based on its most recent trailing twelve-month EBITDAX, which is the end result of a series of improvements since the first quarter of 2021:

YPF Investor Presentation

The company’s current leverage ratio is not unreasonable, although it is quite a bit higher than the sub-1.0x ratios possessed by some of the best American shale oil drillers. The company’s management has generally been expressing a desire to reduce its debt further so we may continue to see improvements here as it brings its export business online. Overall, the company’s debt is certainly not too bad, though.

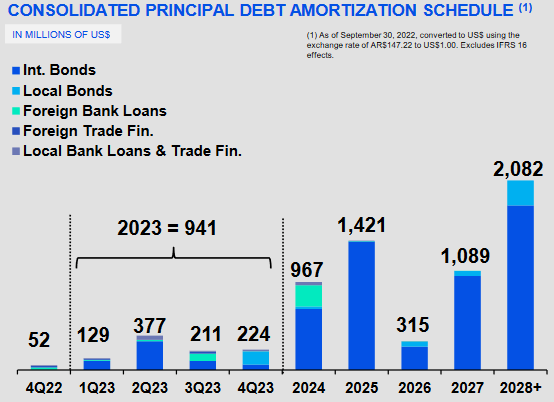

Further evidence that the company’s debt is quite reasonable can be found by looking at its maturity schedule. As we can see here, the company has minimal debt maturities until 2025:

YPF Investor Presentation

It does not overall have any outsized amount of debt maturing in any given year. This is nice because it minimizes the amount of debt that the company will have to roll over during any given year. An energy company can sometimes encounter problems if it attempts to roll over too much debt during a year like 2020 when nobody is willing to finance energy-sector debt. The fact that the company’s debt is staggered helps to avoid problems like this. The fact that it does not have a huge amount of debt maturing until 2025 also gives the company time to generate the cash flows needed to pay down some of that before maturity. This reinforces our conclusion that YPF’s debt load is nothing that we really need to worry about.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of an integrated energy company like YPF, we can value it based on its forward price-to-earnings ratio. This ratio essentially tells us how much we are paying today for each dollar of earnings over the next year.

According to Zacks Investment Research, YPF will generate current-year earnings of $4.71 per share and next-year earnings of $2.89 per share. This gives the company a forward price-to-earnings ratio of 1.80. Here is how that compares to some of the company’s integrated peers:

|

Company |

Forward P/E Ratio |

|

YPF S.A. |

1.80 |

|

Exxon Mobil (XOM) |

7.72 |

|

Chevron (CVX) |

9.03 |

|

Suncor Energy (SU) |

4.90 |

|

Equinor ASA (EQNR) |

5.10 |

As we can see, YPF appears substantially undervalued relative to its peer group. With that said, we do see that every company in the industry is quite cheap considering that the S&P 500 Index (SP500) has a forward price-to-earnings ratio of 19.12 today. We can assume that YPF should receive a discount to its peers due to the fact that it is in Argentina, which is a riskier country in which to operate than some of these other companies do. However, even if we were to assume that YPF deserves a 50% discount because of this, that would still give the company a fair valuation of at least 2.45 so it appears remarkably cheap even given that discount. Overall, YPF is substantially undervalued at the current price and is quite likely a worthwhile purchase at the current price.

Conclusion

In conclusion, YPF Sociedad Anónima is a somewhat underfollowed integrated energy company that could soon become a major producer and exporter of shale oil to the world. The market does not appear to recognize though as the stock remains incredibly cheap despite the run-up that it has seen over the past six months. The company does admittedly have some risks due to the sometimes volatile nature of Argentine politics but that is still priced into the stock. Overall, YPF Sociedad Anónima looks like a strong buy today.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment