gopixa

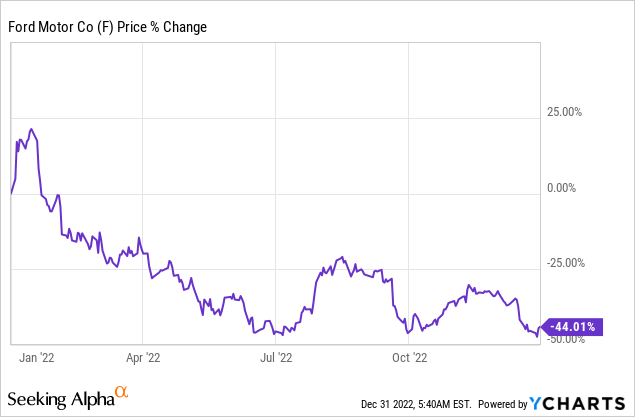

Shares of Ford (NYSE:F) went into a new down-leg in December, experiencing a 17% draw-down in a relatively short period of time due to growing economic concerns and persistent inflation. Considering that Ford already sees material headwinds regarding commodity costs for FY 2022 and inflation remains high heading into FY 2023, I believe that Ford’s valuation will remain under pressure and that investors will be able to buy Ford at a lower price next year!

A positive catalyst: Electric vehicle growth set to ramp up

Ford reported strong growth in its electric vehicle segment in November. During the month of November, Ford sold 6,255 electric vehicles, showing an impressive year-over-year growth rate of 102.6%. Ford’s EV sales are growing twice as fast as the overall EV market segment, according to Ford’s sales break-down.

A model that remained especially popular with US buyers is the Mustang Mach-E sport utility vehicle, of which Ford sold 3,539 units, showing an increase of 14.6% year over year. Ford is also starting to ramp up sales of the F-150 Lightning electric pickup truck — which has started selling this year — of which the car brand sold 2,062 in November compared to zero sales in the year-ago period. In October, Ford sold 2,436 F-150 Lightning trucks. Ford has said that it is going to ramp of F-150 Lightning production aggressively in the next few years, which means the company could see a sales volume of 65-70 thousand (my estimate). Electric vehicle growth is likely going to remain strong throughout FY 2023 as adoption is rising and Ford is making an effort to improve its EV product line-up.

Source: Ford

Increased free cash flow guidance

Ford recently increased its free cash flow guidance for FY 2022 and expects to generate $9.5B to $10.0B in free cash flow, which reflects an increase from Ford’s earlier guidance of $5.5B to $6.5B in free cash flow. However, Ford did not increase its EBIT guidance for FY 2022.

The free cash flow guidance was increased due to strong pricing power as well as strong adoption of electric vehicle products such as the F-150 Lightning, the Mustang Mach-E sport utility vehicle and the e-Transit… most of which are brand-new models that have only recently launched.

Expect margin pressure to build in FY 2023

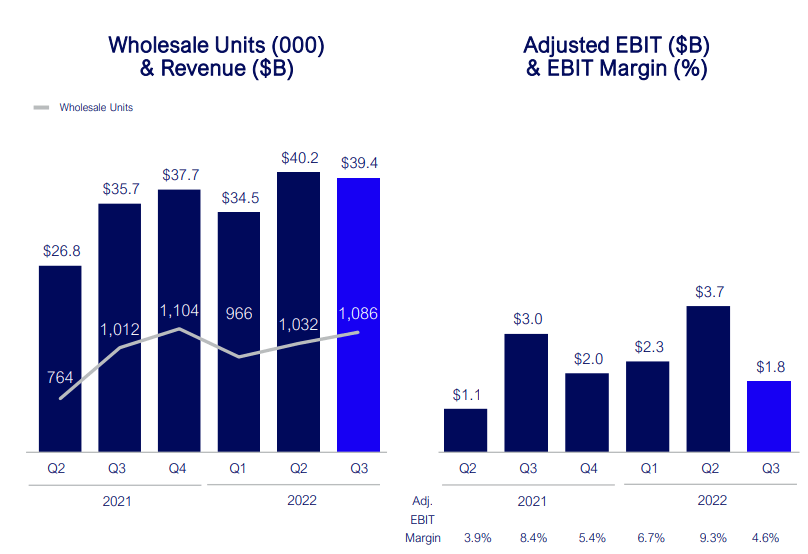

Ford’s third-quarter saw wholesale volumes rise 7% year over year to due to easing supply chain constraints and an improved electric vehicle line-up. However, costs are on the rise as well and Ford’s adjusted EBIT declined $1.2B year over year to $1.8B due to inflationary headwinds and higher commodity prices. Because of those cost headwinds, Ford’s adjusted EBIT margin declined 3.8 PP year over year to 4.6% and 4.7 PP quarter over quarter. Ford has guided for up to $9B in higher costs in FY 2022 due to higher commodity prices and inflation, and margins are therefore set to come under further pressure, especially if a deeper global recession were to weigh on wholesale volumes and costs in FY 2023.

Source: Ford

Ford’s valuation and yield

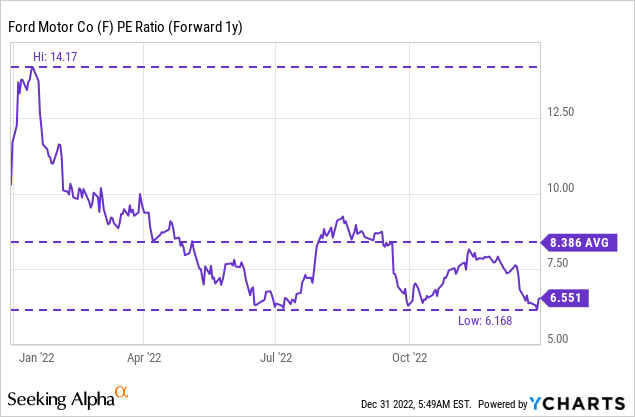

After a 44% decline in pricing this year (I warned about Ford’s correction potential in November), shares of Ford are currently valued at a forward P/E ratio of 6.6 X and a P/FCF ratio of 4.8 X. Although Ford’s valuation is low based off of both earnings and free cash flow, economic risks have grown greatly and the US economy could be forced to deal with a recession in 2023. Additionally, inflation remains high — it was 7.1% in November — and poses a significant challenge for Ford and other car brands that have to deal with higher supplier costs.

Risks with Ford

Ford, I believe, is going to see a major change in operating conditions in FY 2023 due to growing economic pressure — with a recession increasingly likely — which could result in higher supplier costs as well as margin pressure. A decline in wholesale volumes, slowing product demand in a high-inflation world and weakening pricing power are also potential risk factors for Ford’s valuation. Because of these risk factors, especially inflationary headwinds, I also believe that Ford is going to see a year-over-year drop in free cash flow in FY 2023.

Final thoughts

Shares of Ford dropped into a new down-leg in December and lost about 17% of their value. While shares are clearly not expensive, Ford faces cyclical earnings risks as economic risks are growing and inflation remains a major headwind in FY 2023. Although Ford raised its free cash flow guidance and the valuation is also generally attractive from an earnings/free cash flow perspective, changes in operating conditions strongly indicate that Ford has diminished earnings potential in FY 2023!

Be the first to comment