imantsu

Xylem (NYSE:XYL) plays in attractive end markets, but the stock has run up a lot, is richly valued, and may be due for a pullback. The dividend yield is too small, and the company has high debt levels. Investors can consider selling covered calls to generate income. The company’s revenue grew well in 2022, but volumes may be taking a hit. Investors with good gains may consider selling to book some profits. Other investors looking to buy may have to wait patiently for a pullback.

Price increases bolster revenue

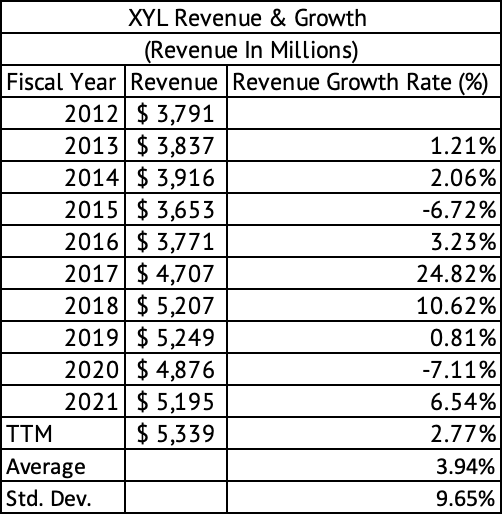

The company operates in three segments, Water Infrastructure, Applied Water, and Measurement & Control Solutions. The company’s average annual revenue growth since 2012 was 3.9% (Exhibit 1). The company showed good revenue growth in its segments in Q3 2022. For instance, its revenues in the Applied Water segment grew by 20% organically, the fastest of any division. The company’s Measurement & Control Solutions Segment showed a 15% organic revenue growth. The Water Infrastructure segment saw organic revenue growth of 13%. The company was able to beat the effects of inflation by increasing prices. But, the price increases may be beginning to take their toll on sales growth, with orders down 7% year-over-year in Q3 2022.

Exhibit 1:

Xylem Revenue & Growth Rate (Seeking Alpha, Author Compilation)

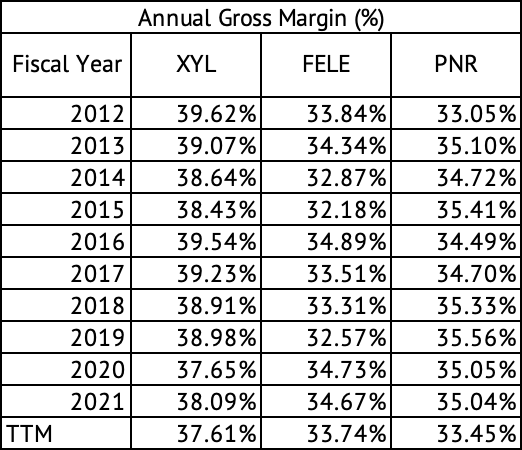

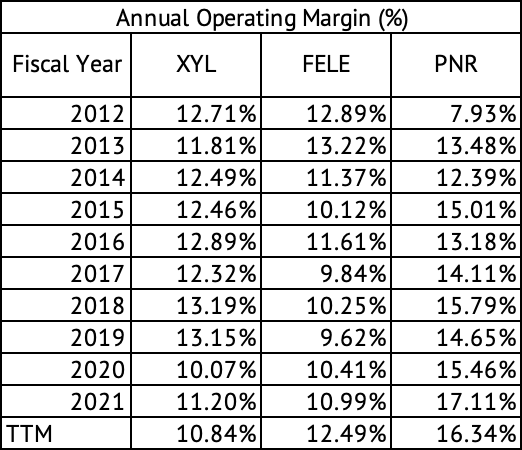

Over the past decade, the company has reported consistent gross margins with low standard deviation. The company has averaged 38.8% in gross margins (Exhibit 2), higher than its competitors, Franklin Electric (FELE) and Pentair (PNR). But, the company’s operating margins (Exhibit 3) are lower than its competitors. Xylem’s research and development investment is one reason for the lower operating margin. The company spends over 3% on R&D.

Exhibit 2:

Xylem, Franklin Electric, and Pentair Gross Margin (%) (Seeking Alpha, Author Compilation)

Exhibit 3:

Xylem, Franklin Electric, and Pentair Operating Margins (%) (Seeking Alpha, Author Compilation)

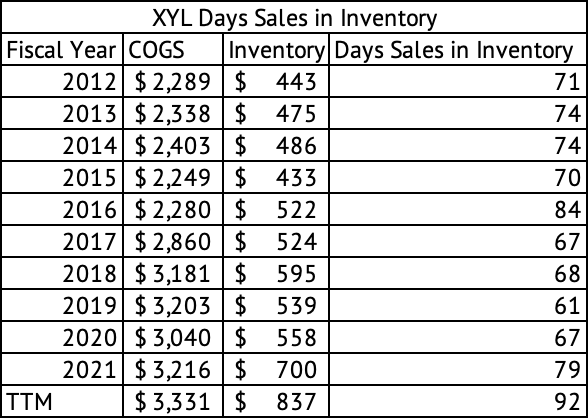

Increase in Inventory

Many companies in the industrial and consumer staples sector have seen a steep rise in the carrying cost of inventory. A combination of high inflation and slowing demand may have contributed to this increase in inventory. Based on the data for the past twelve months, the company is carrying about 92 days of sales in inventory (Exhibit 4). This inventory is the highest held by the company in the past decade. This increase in inventory may dampen cash flows and profitability for the new few quarters in the fiscal year 2023.

Exhibit 4:

Xylem Days Sales in Inventory (Seeking Alpha, Author Calculations)

Dividends, share buybacks, and debt

The stock pays a low 1.09% dividend yield. The Vanguard S&P 500 Index ETF yields 1.6%, and the 2-year treasury yields 4.3%. The payout ratio is a manageable 46%, and over the past five years, the company has grown the dividend by an average annual rate of 10%. The low dividend yield is another reason to avoid this stock.

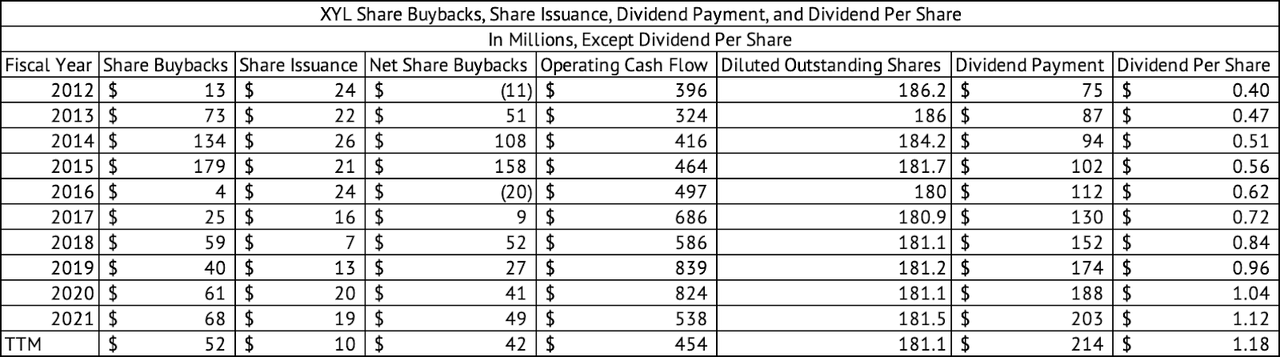

Since 2012, the company has spent over $700 million on share buybacks (Exhibit 5). But, its share issuance of about $200 million reduced the effectiveness of the buybacks. The company’s diluted outstanding shares reduced from 186.2 million in 2012 to 180.9 million at the end of Q3 2022, a reduction of 2.8%. The company has enough operating cash flows to cover its total trailing twelve-month dividend payment of $214 million.

Exhibit 5:

Xylem Share Buybacks, Share Issuance, and Dividends (Seeking Alpha, Author Compilation)

The company’s current cost of debt has been low due to low-interest rates over the past decade. For example, the company issued $400 million in 4.375% Senior Note due in 2046. But, with the 2-year U.S. Treasury Note yielding 4.3% today, borrowing costs for companies have gone up. The company will have to pay a much higher rate on its long-term debt, given its high debt-to-EBITDA ratio of 3.6x. At the end of Q3 2022, the company carried total long-term debt of $1.88 billion and short-term liabilities of $483 million.

Valuation

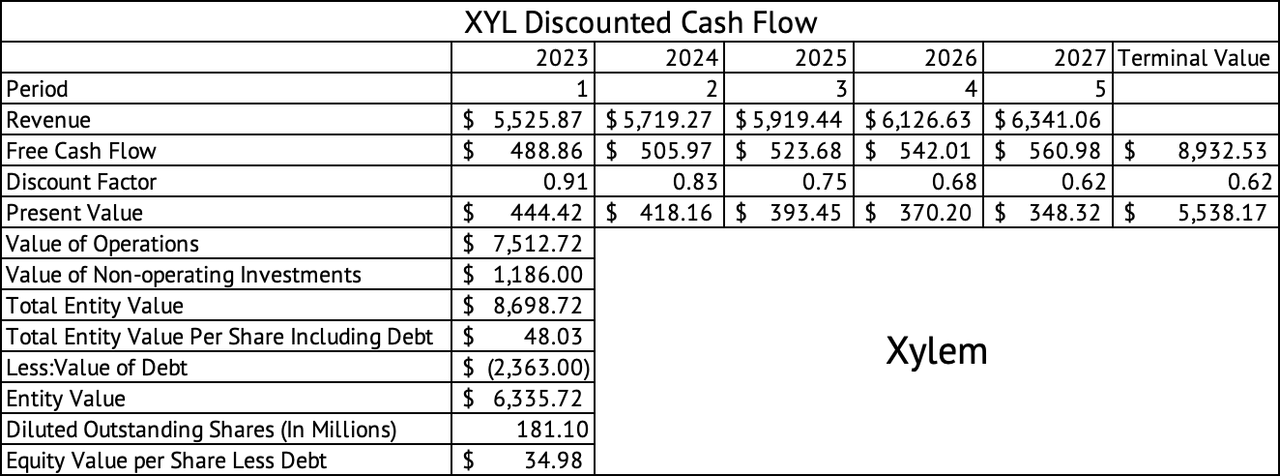

The company is overvalued based on a discounted cash flow method and valuation metrics. The company trades at a trailing GAAP PE of 62x and a forward GAAP PE of 58x. Its five-year average forward GAAP PE is 38x. A discounted cash flow [DCF] model for Xylem yields a per-share value of approximately $48 (Exhibit). Although the company has grown its revenue quickly in the past year, the DCF model assumes a long-run growth rate of 3.5%. The company is overvalued, trading at around $109.

Exhibit 6:

Xylem Discounted Cash Flow (Seeking Alpha, Author Estimates and Calculations)

The company’s average annual revenue growth since 2012 was 3.9%. Based on this historical average growth rate, a 3.5% average long-term growth rate is a reasonable assumption. The company’s weighted average cost of capital [WACC] was 9.6% based on a U.S. 10-year rate of 3.75%. A discount rate of 10% was applied to the cash flows. Free cash flow was derived by subtracting capital expenditures from operating cash flow. Based on this free cash flow measure, the company’s average free cash flow margin was 8.85%.

Xylem’s run may be over

The company’s stock went on an impressive run in the past six months, returning 42.8%. This run was punctuated by two monthly returns of 17% in July and October 2022 (Exhibit 7). Given this positive momentum, the company outperformed the Vanguard S&P 500 Index ETF (VOO). The stock is down 6.6%, while the Vanguard S&P 500 Index ETF is down 18.6%. The stock is volatile, with a beta of 1.11. For every 1% monthly change in the S&P 500 index, the stock can be expected to change by an average of 1.11%.

Exhibit 7:

Xylem Monthly Returns [Jan 2022 – Nov 2022] (Data Provided by IEX Cloud, Author Calculations)![Xylem Monthly Returns [Jan 2022 - Nov 2022]](https://static.seekingalpha.com/uploads/2022/12/25/saupload_usJlfFTKsAl2XXgPMThxDWAnNx5ajgh6HwL56rbtz5xsMp08E4gOIDPGSWwPhlffcazqmG9tjJUJ2uqdpw4uAP3ojJmQk0vJLcfewW8j0BJKR9HFR-EQnEKoLMw6jMx5rMjRTRcG__Yo-IXODMmzUjNkHXqxmi3HHakppdVeJ6rHPl4lPZ3hxotp_23UJA.png)

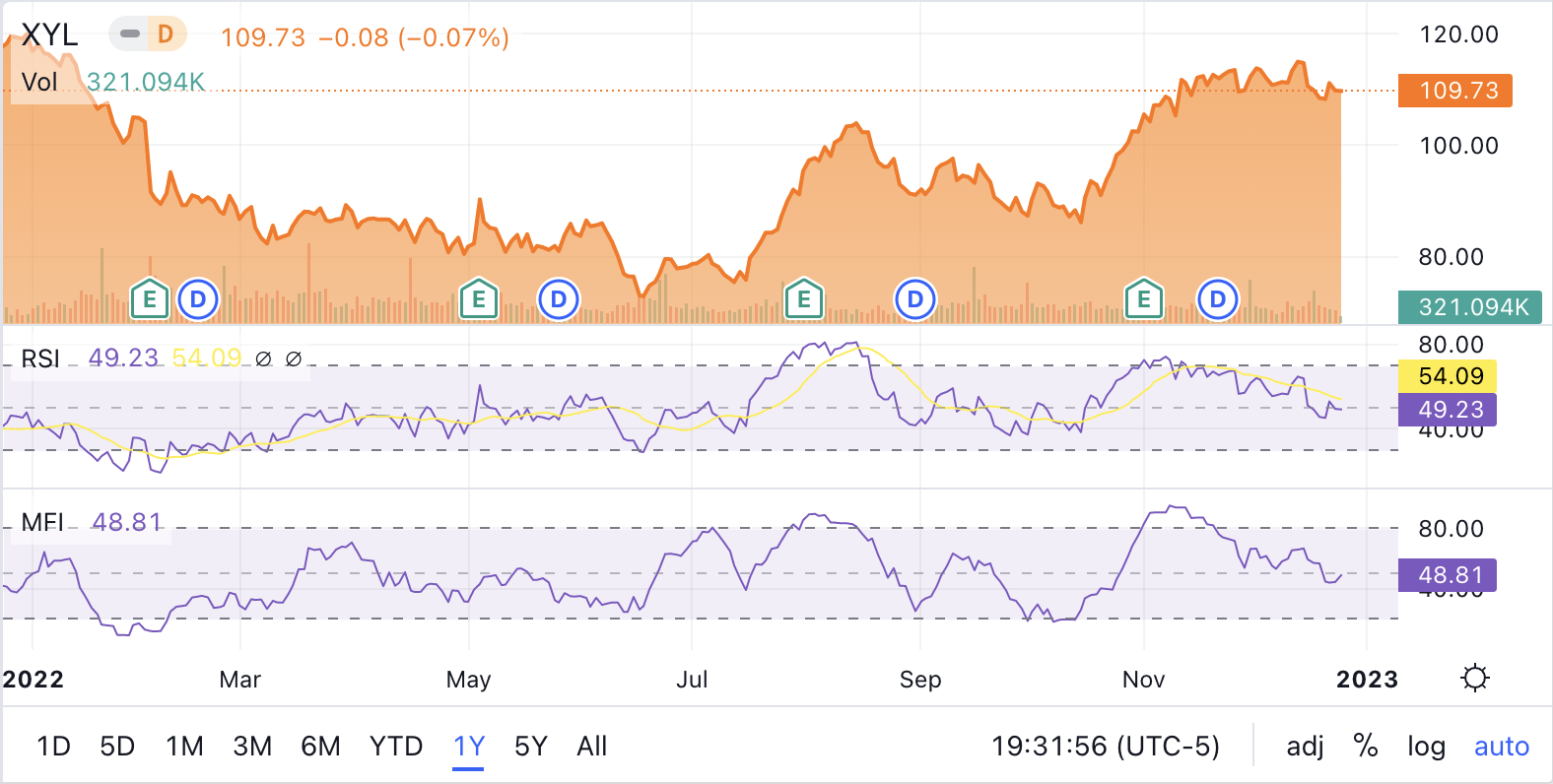

The RSI and MFI technical indicators show the fading momentum in the stock, with the indicators trending lower (Exhibit 8).

Exhibit 8:

Xylem RSI and MFI Technical Indicators (Seeking Alpha)

Sell covered calls

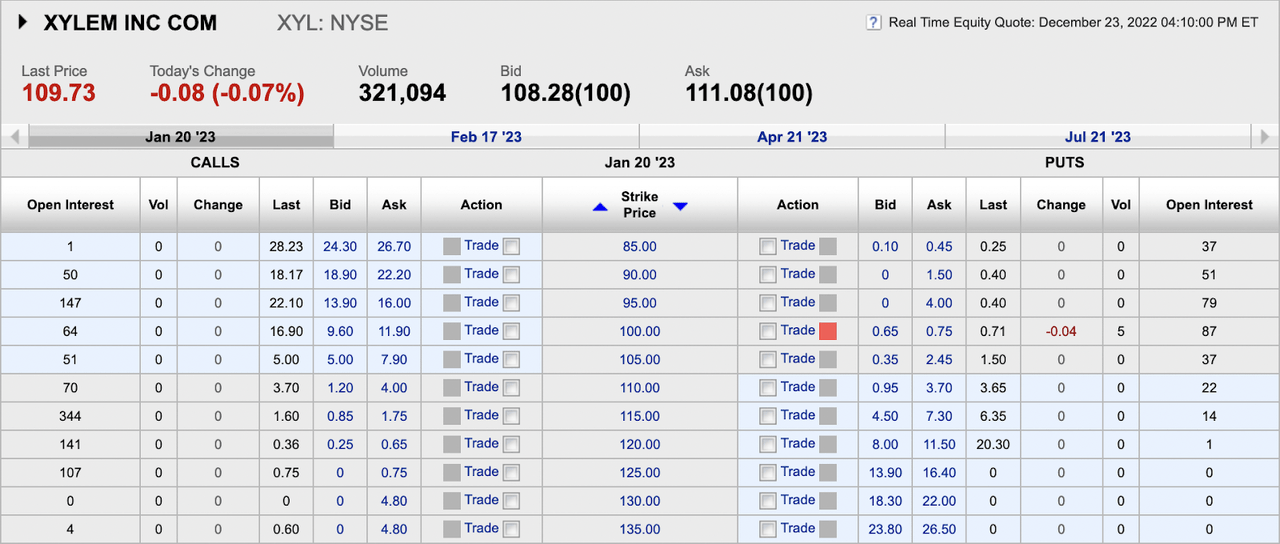

Given the stock’s run and fading momentum, this may be the opportune time to sell covered calls on this volatile stock. Jan 20, 2023, $110 strike price calls last traded for $3.70, yielding 3.3% (Exhibit 9). If the positive momentum continues, the stock could be called away. But, if an investor is sitting on good gains and is indecisive about booking profits, covered calls may be a way to take the decision out of your hands. Covered calls may not be a good strategy if the yield on cost is over 3% and you wish to continue earning the dividend income.

Exhibit 9:

Xylem Call and Put Options (E*Trade)

Xylem is overvalued based on various valuation metrics and using a discounted cash flow estimate. The company has shown good revenue growth over the past year, but price increases may finally take a toll on sales volumes. Investors may consider selling covered calls to generate income as the stock’s momentum fades. The dividend yield does not provide much income. Investors may be better off waiting for a sell-off to buy Xylem at a more attractive valuation and gain a higher dividend yield.

Be the first to comment