Lintao Zhang/Getty Images News

China Dismantles Its COVID-Zero Policies

China has stunned the world with its rapid U-turn from its stringent “dynamic COVID-zero” restrictions that have stung its economy. The turnaround was even more dramatic as Chinese President Xi Jinping maintained his unrelenting commitment as he secured his unprecedented third Presidential term, pledging to continue China’s tough stance on stamping out COVID.

However, China has been rapidly dismantling its unsustainable COVID defenses, which irked its population, as they went to the Streets to protest against incessant lockdowns. Xi’s about-turn received praises of pragmatism in his policymaking as he looks to position China for growth in 2023.

China’s Politburo was reportedly looking to raise 2023’s GDP growth rate by over 5%, given the malaise in 2022. Accordingly, China plans to raise its per-capital GDP to the level of a “medium-developed country by 2035.” Such a goal would require China to post annual GDP growth rates “at 5% or higher through 2030.”

Therefore, it’s increasingly clear China needs domestic demand to play a critical role, bolstering its faltering exports as the world moves closer to a recession in 2023. As such, it shouldn’t be surprising that China has mustered a decisive flip-flop in its COVID policies in record fashion as China moves toward a full reopening.

Accordingly, the KraneShares CSI China Internet ETF (NYSEARCA:KWEB) recovered nearly 85% from its October lows toward its recent highs. Hence, Chinese stock investors who seized on the battering in October have outperformed the S&P 500 (SPX) (SP500) markedly, as it retreated recently as the Fed is expected to remain hawkish through 2023.

As such, the hammering in Chinese stocks, particularly its tech sector, could be lifted significantly in 2023 as Xi Jinping looks toward the private sector to spur consumption and growth. Accordingly, Xi’s top economic advisor and premier-in-waiting, Li Qiang, articulated that “the government would create a ‘favorable environment’ for the private sector.” As such, we believe the commentary forebodes well for KWEB’s leading constituents, given their critical role in helping drive China’s consumption recovery.

China: Full Reopening Expected By Mid-2023

Accordingly, economists have coalesced around a full reopening of its economy in mid-2023 as China looks to pursue its growth agenda. However, doubts remain given the resurgence of COVID cases as China pushes hard to reintegrate with the world.

Despite the sharp rise in cases, China has moved to downgrade the “management of COVID-19 from the top level to the second highest level, effectively removing the legal justification for aggressive COVID-19 restrictions.” This is a decisive break from its COVID-zero policies. If there’s still any lingering doubt about the will of Xi Jinping and his Politburo would hunker down due to the resurgence in cases, this decision should settle it.

Accordingly, it also paved the way for China to scrap quarantine requirements for inbound travelers from January 8, requiring only a negative COVID test outcome within 48 hours of departure. Furthermore, it has also lifted the most stringent restrictions on outbound travel, no longer requiring airlines to cap the number of international flights and passenger capacity.

Furthermore, the policy maneuvers occurred while China’s COVID cases reached new heights. Therefore, we believe that Chinese stock investors should be assured that a subsequent recovery in domestic demand and its property sector should further lift buying sentiments moving forward.

Fund Managers Turned Highly Pessimistic In October, But Savvy Investors Were Not

Accordingly, market strategists and fund managers have lifted their buying sentiments recently, anticipating an improvement in China’s economy. However, they were also highly pessimistic at its October lows, as they feared the one-man rule of Xi Jinping after the CPC’s 20th National Congress.

Despite that, astute investors have already anticipated that China would not sustain its harsh COVID restrictions in 2023, despite the massive pessimism in October.

Accordingly, China’s leading e-commerce behemoth Alibaba (BABA), surged nearly 70% from its October lows to its recent highs, while China’s leading NEV player BYD (OTCPK:BYDDF), recovered almost 40% from its October lows toward its recent December highs.

Takeaway

We have already anticipated a pullback in Chinese stocks as investors took profits, even with these fund managers turning more bullish after getting concrete policy signals from China’s Politburo. But, it’s also essential for investors to understand that the market is a forward-discounting mechanism.

Therefore, it’s more important to parse and assess the moves by market operators and avoid paying too much attention to the euphoria or gloom generated by the mainstream media.

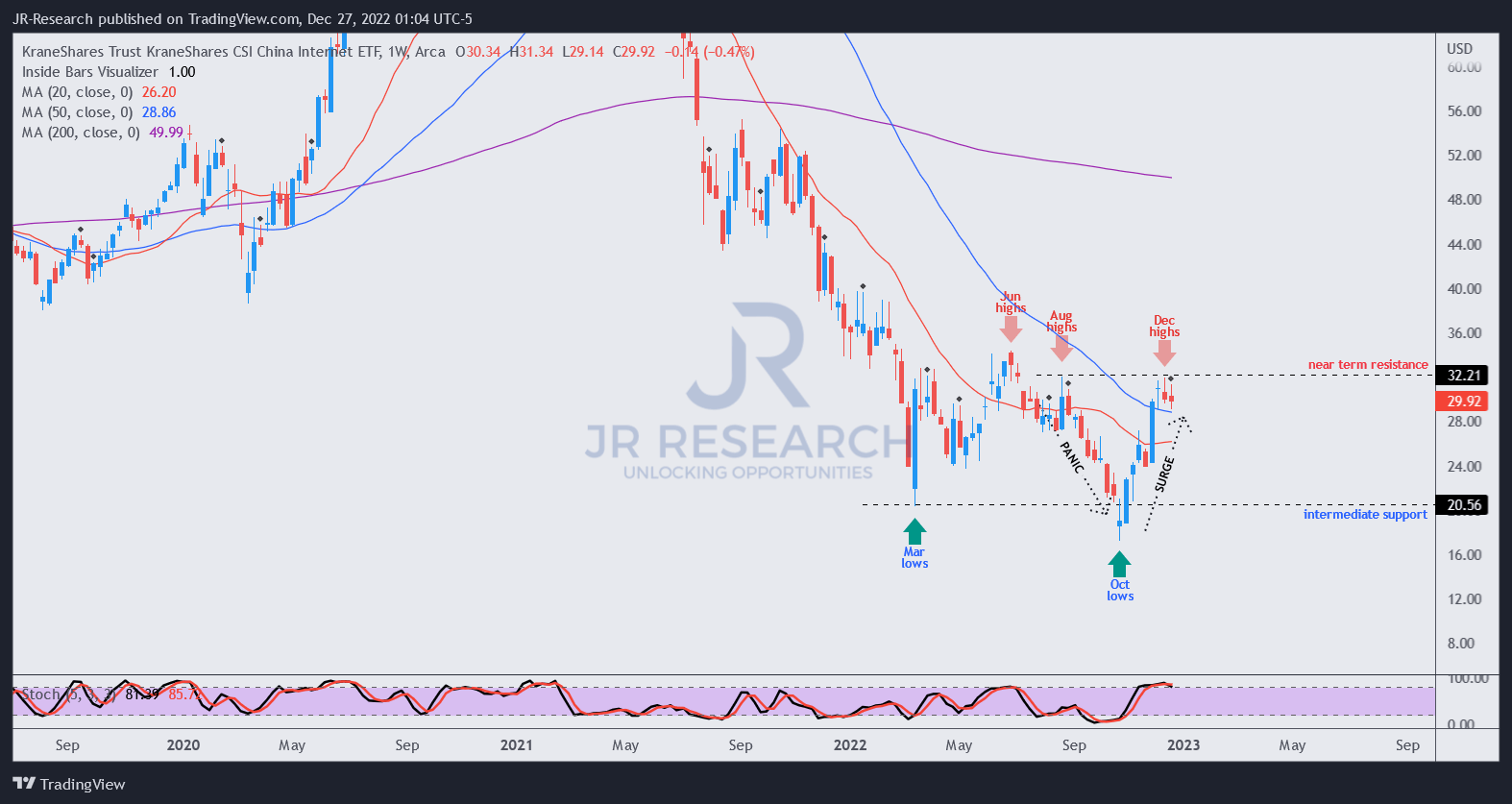

KWEB price chart (weekly) (TradingView)

Taking a closer look at KWEB’s price chart, investors should better understand what we highlighted. Its October lows were an astute bear trap, predicated against the lows of March, forming a potent double-bottom that eviscerated the sellers at those lows. Recall that the trap was formed when investors’ sentiments toward Chinese stocks were highly pessimistic.

However, by the time investors await concrete signals from China’s Politburo on its COVID reopening, the surge has already occurred, with KWEB in well-overbought levels. Moreover, a pullback is looking increasingly likely, as its buying momentum has also stalled. Hence, investors looking to add exposure can consider waiting for a retracement first.

Notwithstanding, we believe there is a plenitude of opportunities to invest in fundamentally strong Chinese stocks in 2023 as China looks to mend its political ties with the US and Europe.

Rating: Revised to Hold (Previous: Buy)

As always, stay safe and Happy Holidays!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment