naphtalina/iStock via Getty Images

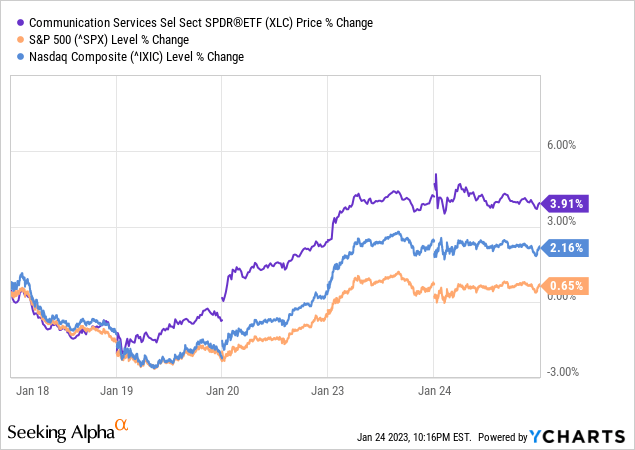

According to SA, the Communication Services Select Sector SPDR Fund (XLC) exhibited an average weekly PriceVol of 9.8, which is above the S&P 500’s 7.5. Now, the PriceVol indicator measures market volatility. Still, a comparison of the price performances for the last five days shows that it is XLC that has outperformed the broader market, by more than 3% as per the deep blue chart below. Noteworthily, the Communications ETF has also outperformed the tech-heavy Nasdaq Composite, despite the two sharing many common names as I will detail later.

The aim of this thesis is to show that this outperformance of XLC with respect to the Nasdaq may continue as its holdings are more fitting to invest in the current low-growth environment due to interest rates being much higher than in 2021. For this purpose, I will start by going through the fund’s holdings, and explore the sector exposure in the context of the divide between OTTs and the pureplay telcos which are categorized as diversified telecommunications service providers.

Revenue Growth of OTT Vs Pureplay Telcos

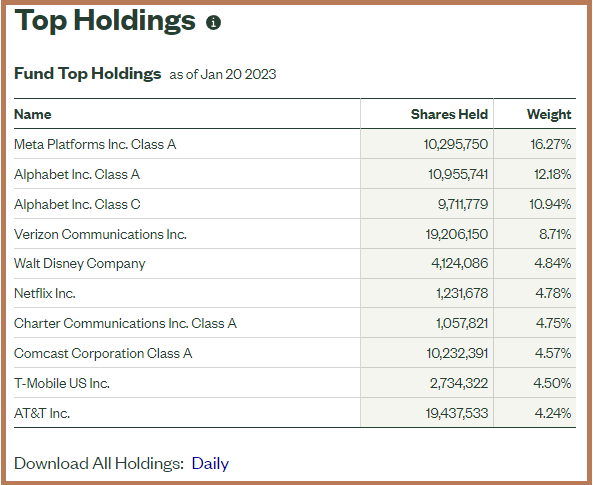

First, a glance at the fund’s top holdings shows that big tech names like Meta Platforms (NASDAQ:META), Alphabet (NASDAQ:GOOG) (GOOGL), and Netflix (NFLX) with their combined weight of nearly 45% may mask the relatively more pureplay, (but also diversified) telecommunications services operators like Verizon (VZ), T-Mobile (NASDAQ:TMUS), AT&T (T) and Comcast (CMCSA). These four form part of the more traditional telecom operators or telcos group.

XLC Fund holdings (www.ssga.com)

In the second group, there are the OTT (Over The Top) platforms, such as Meta’s WhatsApp, Alphabet’s YouTube or Netflix, and other video streaming companies which tend to consume a large chunk of the bandwidth of telecommunications infrastructures, be it local or international.

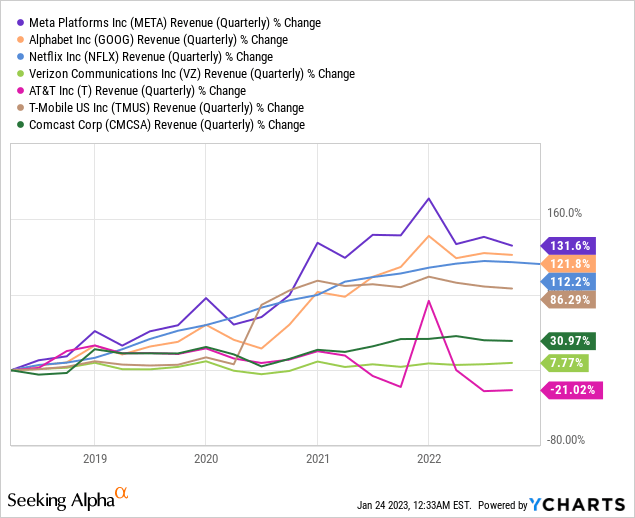

These two groups have known different growth paths, and as shown by their above 100% quarterly revenue growth during the last five years, the OTT group has been able to profit from fiber and mobile cellular networks which span from their data centers to users throughout the country, and this, without necessarily participating in the massive investment efforts required in modernizing these.

This feat has been made possible by their business model which has consisted of taking advantage of the era of cheap money where interest rates were low to grow rapidly through acquisitions and offering an array of services varying from search, advertising, and interactive media. In this way, they have delivered some of the most extraordinary growth rates commonly in the double digits and often flirting with the triple digits. As such they have been rewarded by investors with their market capitalization reaching hundreds of billions of dollars.

On the other hand, except for mobile network operator T-Mobile which delivered five-year growth of 86% (above brown chart) as of 2020 after its Sprint acquisition, the ones which are at the low end of the spectrum for growth are telecom operators (telcos) like Verizon, AT&T, and Comcast.

Sector Exposure and Challenges

These telcos have not been able to monetize the investment they made in fixed lines or wireless largely due to their more linear growth models which essentially depend on growing the number of subscribers. Now, they have surely diversified into media and streaming activities, but not with the same degree of success as the big techs, as shown by their relatively lackluster revenue growth.

However, there are challenges ahead for big tech. First, borrowing costs are increasing rapidly which has inflated the value of deals during prospecting for acquisitions. Second, as shown by scrutiny of Microsoft’s proposed $69 billion Activision Blizzard (ATVI) deal, regulators are likely to be tougher in letting big tech grow bigger just by swallowing their competitors.

On the other hand, more used to organic growth, telcos have a better chance of adapting to the current high-interest rate environment if they are able to grow without increasing debts. Now, with a $43 billion spin-off of WarnerMedia and outsourcing the IT infrastructure for both its 5G core and access networks to Microsoft’s Azure, AT&T is indeed adopting a more capital-light strategy.

As for Verizon, except for the media part which was offloaded to Apollo in 2021 for $5 billion, it has chosen to maintain the integrity of its business model by combining part of the infrastructure, the network layer, and the distribution of connectivity and communication services. It can thus offer a wide range of services and meet the needs of different customer segments.

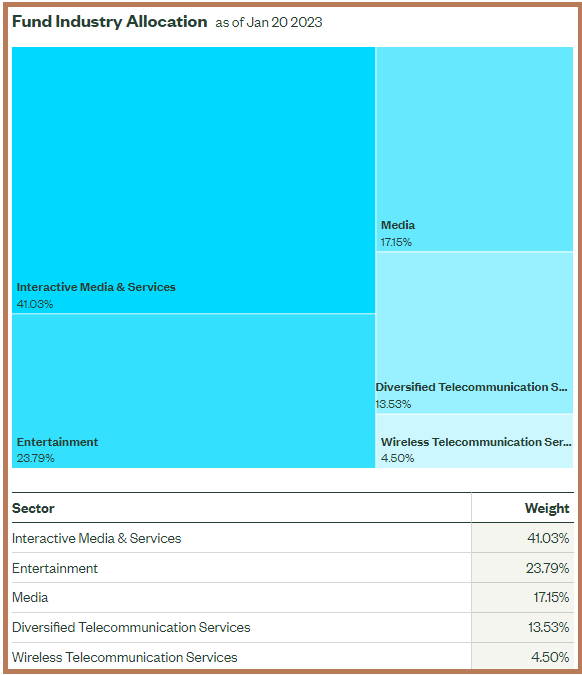

Pursuing further, with its Infinity product line, studio production, and cable businesses, Comcast is a telecommunications conglomerate. In fact, just on its own, it constitutes 4.57% of XLC’s weight and forms part of the 17.15% that the ETF dedicated to the Media sector as per the fund allocation diagram below.

XLC Sector Exposition (www.ssga.com)

Then, telcos have taken steps to end the vicious circle of spending high Capex for low gains by offloading assets to reduce debt or finance future investments. This follows in the footsteps of offloading tower assets to towercos like American Tower (NASDAQ:AMT) in the previous decade.

However, the question is what to do with the big techs in XLC’s portfolio. Well, their profitability should suffer from higher interest rates for sure, but, some will suffer more than others.

First, after a slow start in building its metaverse, Meta is rapidly expanding, with a deal signed with the NBA (National Basketball Association) for providing at least 50 games in VR mode. Also, Meta’s Quest, (or the headset required to play in Meta’s Horizon Worlds) is the NBA’s official VR headset. As For Netflix, its shares have surged after it added 7.66 million subscribers globally, reaching 230.75 million members. This increase in membership is not necessarily due to advertisements, but, the use of AI to propose new movies based on subscribers’ tastes in addition to better controlling unauthorized usage (users sharing their passwords). Also, as seen with Microsoft’s ChatGPT venture, AI should drive new avenues of growth for big techs like Google, which is also optimizing costs with the departure of 12K employees.

XLC is Better for a Low-Growth Environment

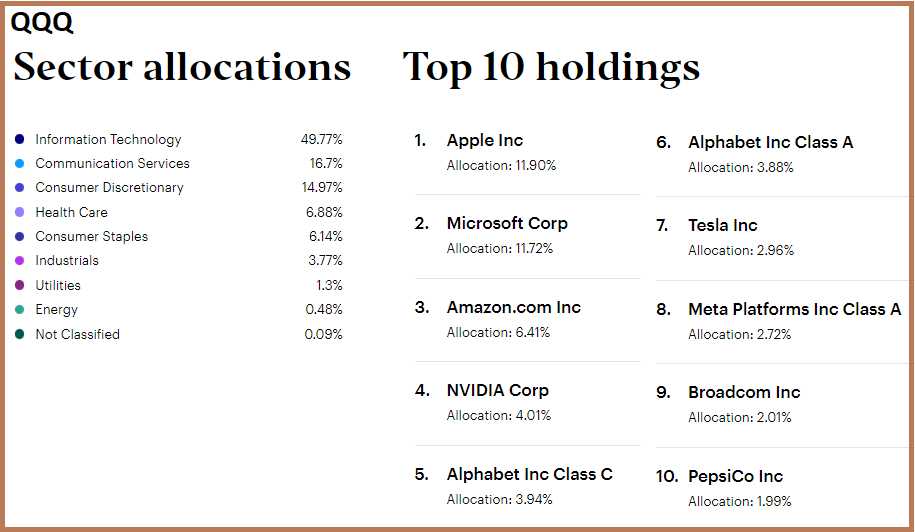

Therefore, by going through the sector exposure and challenges faced by the holdings, be it OTTs or pureplay telcos, this thesis has shown that there are opportunities for XLC as a whole in 2023. Furthermore, with more weight allocated to organic growth-focused telcos, and communications-oriented tech names as per the above list, I think the ETF represents a more balanced approach to investing in growth at the current juncture than in the Invesco QQQ Trust (QQQ) which tracks the Nasdaq-100 index.

QQQ Holdings (www.invesco.com)

The reason is that QQQ whose holdings are shown above is more sensitive to the Federal Reserve interest rate hikes. Thus, in case there is spiraling inflation or one where higher wages lead to higher commodity prices, monetary policy is likely to see a continuation in tightening. Even in the case that inflation does not rise, the Fed is not likely to bring down interest rates for fear of letting things go out of control. In this case, the tech-heavy ETF is likely to suffer more in a low-growth environment engendered by higher borrowing costs, and its holdings will have to strive to deliver the level of revenue and earnings growth that can justify their higher valuations. As a matter of fact, it has a price-to-earnings ratio of 20.36x compared to only 13.51x for XLC.

Now, the fact that XLC is better for 2023 is also supported by Goldman Sachs’s (GS) research.

Concluding with a Dose of Caution

For this matter, since the economic conditions at the beginning of this year, at least up to now, are not very different from last year, we can learn from the historical performance of ROE or Return on Equity. According to Goldman, ROE which has been lackluster for the S&P 500 for the past three quarters and on a year-to-date basis, will suffer from a further drop. The causes are headwinds from both higher borrowing costs and taxes which will adversely impact margins. Consequently, after rebalancing its “growth basket”, whose ROE outperformed the S&P 500’s by 10% in 2022, the investment bank recommended XLC as part of a list of other stocks.

Moreover, considering a 10% outperformance of the communications ETF for 2023 (or just like 2022), out of which 3% has already been achieved as per the introductory chart, I have a price target of $57.65 (53.88 x 1.07) based on a 7% increase applied to XLC’s share price of $53.88.

Ending with a cautionary note, which explains my neutral position on the ETF, investors are reminded that this is likely to be a volatile earnings season for tech stocks with the contagion effect likely to be felt by XLC as well. Additionally, there is the possibility of a recession occurring this year, but, again, Goldman Sachs also hints that this could be avoided.

Be the first to comment