Oselote

Our June piece on NGL Energy Partners LP (NYSE:NGL) was not too popular with the bulls. Not only did we put out a sell on the common, but we also suggested that NGL Energy Partners LP PFD UNIT CL B (NYSE:NGL.PB) and NGL Energy Partners LP PFD UNIT CL C (NYSE:NGL.PC), both would ultimately hit the zero mark.

The common stock can bounce between now and that point of course. Even the publicly traded preferred shares remain completely detached from reality as they trade in the double digits. Ultimately, we expect all of them to also go to zero. Exact timeline remains slightly in doubt. We are downgrading the common shares and preferred shares to a Strong Sell.

Source: Pain Ahead, Sell Common And Preferreds

A radical stance? Perhaps. But it has been one that has worked with the common shares dropping 50% and the preferreds down over 33%. We recently upgraded the common shares but left the preferred shares on a sell rating as we did not see very pleasant prospects for them. We examine the Q2-2023 numbers and tell you why we are handing you another upgrade.

Q2-2023

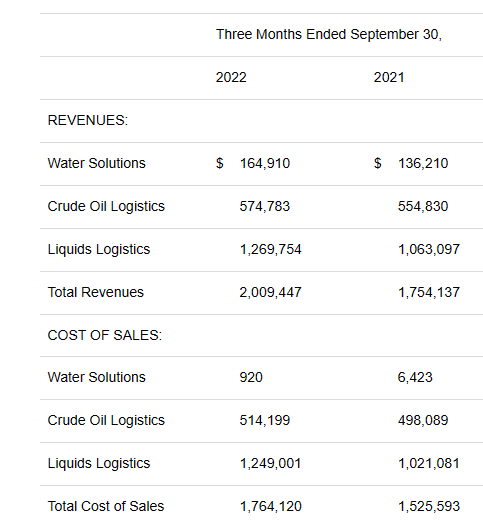

NGL has a fiscal year ending in March so the September 30, 2022 quarter is the second quarter of fiscal 2023. Adjusted EBITDA for the Q2-2023 dropped to $142.2 million, compared to $146.3 million for the previous year. This was despite record revenues in the water solutions segment. NGL processed approximately 2.27 million barrels of produced water per day during this quarter, a 28% increase vs last year. Revenues were up 21% and matched a good deal of the increase. Revenues were not an issue in all three segments, but expenses more than matched the bump.

NGL Financial Results

In favor of the bulls was the reaffirmation of the annual EBITDA guidance and continued confidence in paying off the 2023 maturities that lie dead ahead. While that does sound good, there are certainly challenges for the company as a whole.

That $600 Million Guidance

NGL got a big boost from oil prices in 2022. The company has direct exposure via the skimmed oil it recovers. Obviously when it guided for fiscal 2023 in early 2022, it did not have an idea that these revenues would shoot up.

Revenues from recovered crude oil, including the impact from realized skim oil hedges, totaled $32.9 million for the quarter ended June 30, 2022, an increase of $16.9 million from the prior year period.

Source: Q1-2023 Press release

Revenues from recovered crude oil, including the impact from realized skim oil hedges, totaled $24.2 million for the quarter ended September 30, 2022, an increase of $4.9 million from the prior year period.

Source: Q2-2023 Press release

Despite this boost, adjusted EBITDA has struggled.

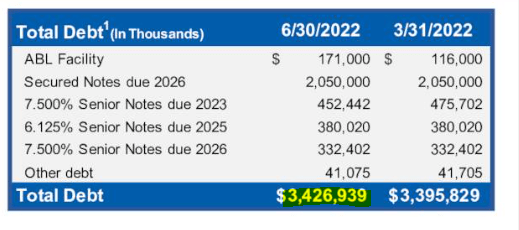

Net debt went up in the first quarter of the year, albeit marginally.

NGL Presentation

During the second quarter, it went up yet again.

NGL Financial Results

Management was asked about this and referenced the upcoming heating season buildup as the key factor.

Linda Bridges

Yes. I think I can address what I think the question was, which really was — I think he — Will had referenced the liquidity drop of $111 million. Again, liquidity, as we define it is cash plus available borrowings, available capacity, I’m sorry, on our ABL facility.

Our ABL facility will naturally increase in borrowings, meaning capacity or excess capacity will decrease on the ABL facility as we build inventory into the fall — during the fall period. We build that inventory to support our propane and butane businesses. They’ll begin liquidating that inventory in the second half of our fiscal year. So, [Technical Difficulty] would be expected to build back up as we use proceeds from the liquidation of inventory to repay those borrowings on our ABL facility.

So, this is a very consistent trend that you’ll see in our borrowings where you have increases in late summer, early fall, and then you’ll start seeing decreases as we exit the blending and heating seasons into the spring.

Source: Q2-2023 Conference Call Transcript

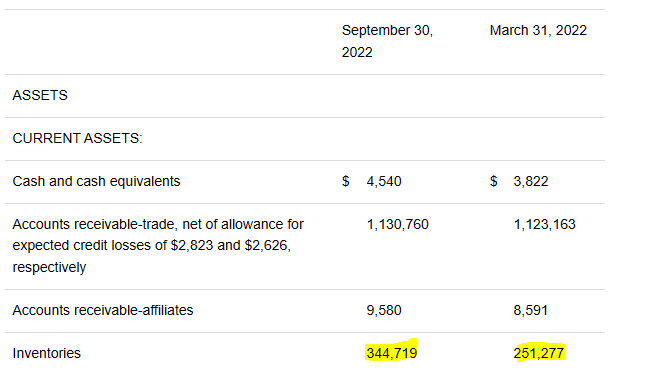

The same can be visualized here.

NGL Financial Results

Ok, so that $93 million inventory increase more than explains the debt increase over the last two quarters. Nonetheless, NGL should be deleveraging faster at this point if it wants to be able to refinance at anything resembling tolerable rates.

Verdict

The first aspect here is that if we have a very strong heating season, NGL likely benefits from its propane business and that could buy it some time. So far that appears to be the case. On the other hand, the tailwind from higher crude oil prices is now in the rear-view mirror and the comparatives will get tough in the next two quarters. While common and preferred equity dance where they wish, the bonds tell the real story and it is quite an interesting one.

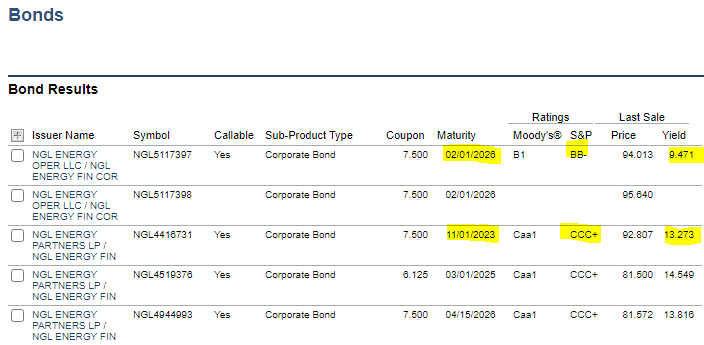

In June 2022, when we penned our bearish piece, the 2023 maturities had a yield to maturity of 13.27% while the longer dated secured debt yielded 9.47%.

Finra June 2022

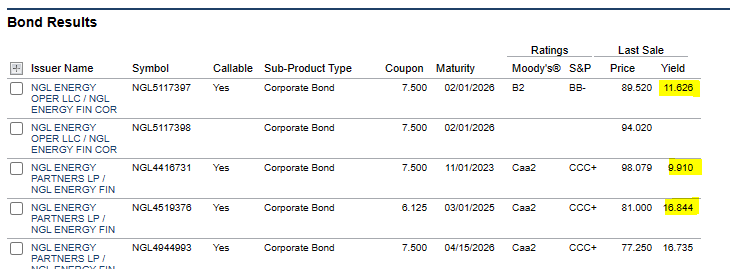

The 2023’s have actually compressed markedly and are now offering under 10%.

Finra

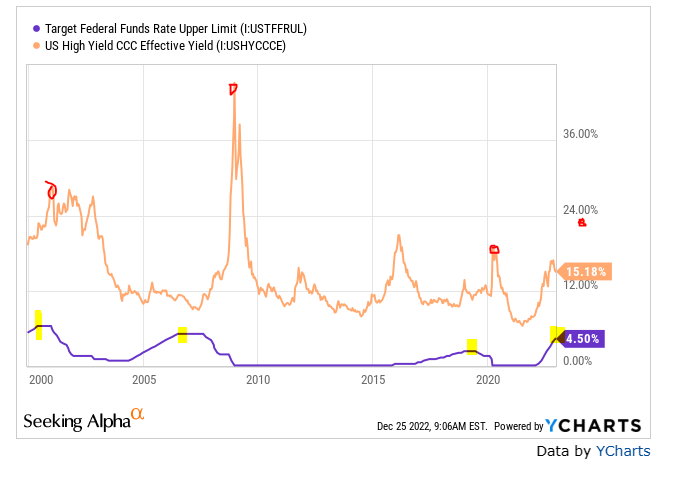

Stunningly enough, all other maturities look worse and the near 17% yield to maturity of the 2025 bonds is suggestive of extreme distress. Some of this is of course generalized credit conditions, but we expect these to worsen over time as the delayed impacts from Federal Reserve tightening enter the system. Historically the final peak after Federal Reserve tightening is well after they stop, and they have not yet stopped hiking.

Y-Charts, Author’s Coloring

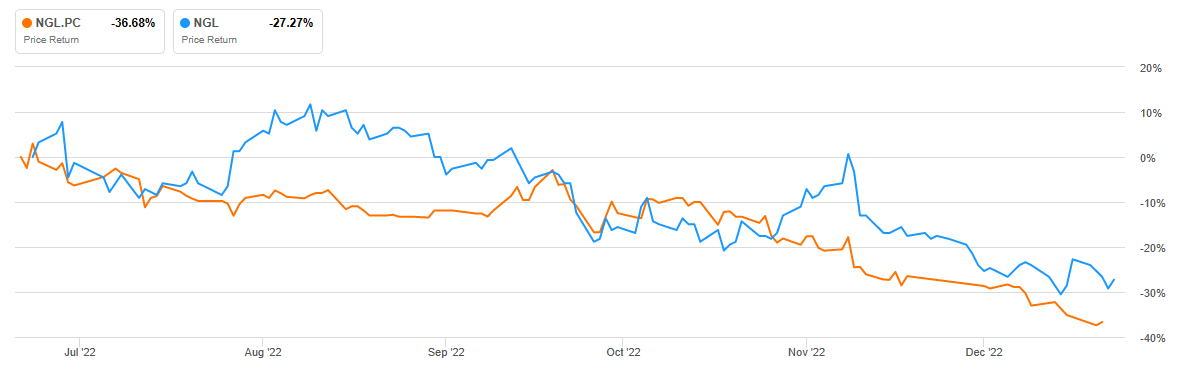

The risks remain extremely high for the longer term and the probability of a single dollar of distribution being paid on the preferred shares remains close to zero. But at this point the risks are getting better priced in and that leads us to our upgrade. If readers remember, we upgraded the common shares to a hold in September as the risks were getting fairly priced in.

Seeking Alpha

We are seeing the same on the preferred shares now. If we add in the accumulated distributions that theoretically have to be paid, the underperformance is even worse. More than half of the current preferred share value is comprised of these accumulated distributions (60 cents a quarter for 8 quarters). At this point they should perform in line with the common shares. We also expect them to get forcefully converted into common shares at some point and the relative pricing looks fair. Some might complain that this stance is at odds with our longer-term outlook of a wipeout. Our defense is that a “Sell” call is a “Short Sell” call and we only use it when we see perfect setups. We will add that every single sell rating and subsequent shift to a hold has been profitable on these securities.

Tipranks

We see no reason to have a Short Sell rating at this point and hence we are upgrading the preferred shares to a Hold/Neutral rating.

We look forward to the next quarterly results from NGL to see if they can indeed deliver on their promises.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints. We strongly recommend you have a Merry Christmas and a Happy New Year.

Be the first to comment