cemagraphics

WisdomTree (NYSE:WT) has a different business profile within the asset management industry and relatively good growth prospects ahead, but its current premium valuation is not attractive for investors.

Business Overview

WisdomTree is an asset management company, which is focused exclusively in exchanged-traded products, including exchange-traded funds (ETFs), and other exchange-traded instruments. It serves both retail and institutional customers, being a relatively small asset manager measured by its assets under management (AUMs) of about $85 billion. Its market value is $843 million, also showing its small size in the financial industry.

The company has a quite unique business model, given that usually asset managers are more focused on ‘managed’ or active funds, rather than passive investments, which typically have higher management fees and are therefore more profitable for asset management companies.

Indeed, most of its competitors offer both active and passive funds, enabling them to reach a higher total addressable market than WisdomTree, which can be seen as a negative factor for WisdomTree’s growth prospects. Despite its different business approach, its closest competitors are other ETF providers, such as BlackRock (BLK), Invesco (IVZ) or State Street (STT).

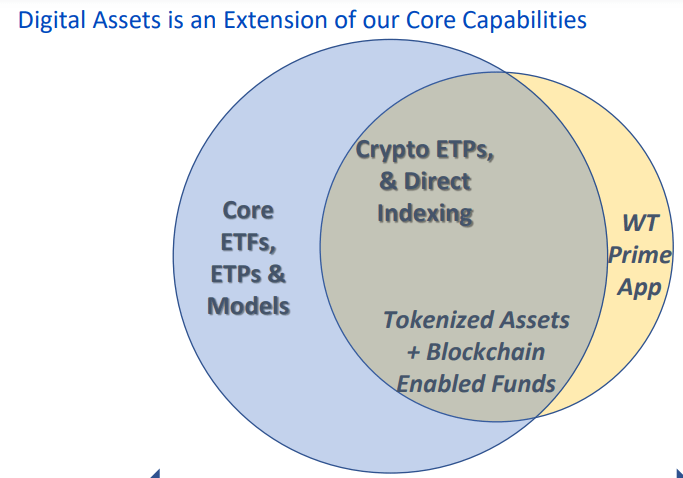

WisdomTree launched its first ETF in 2006 and currently has a much wider product offering, including digital assets. This shows that WisdomTree has adapted its business model to new developments in the market, remaining focused on providing passive investing instruments.

Its current product offering includes U.S. equity, international developed equity markets, emerging market equity, fixed income, commodity & currency, alternatives, plus cryptocurrency. Beyond offering indexed funds, it also provides alternative funds that invest based on factor investing, which are funds that make their investment allocations based on fundamental metrics, such as earnings growth, dividend yield, share price momentum, beyond others.

Most of its funds employ quantitative investment, based on proprietary indexes, being a distinctive factor to competitors. Usually, most ETF providers follow a capitalization weighted methodology based on third-party indexes, such as the S&P 500 Index that is provided by S&P Global (SPGI), while WisdomTree by developing its own indexes can differentiate from other ETF products, and also save costs by not paying fees to index providers.

Growth Prospects

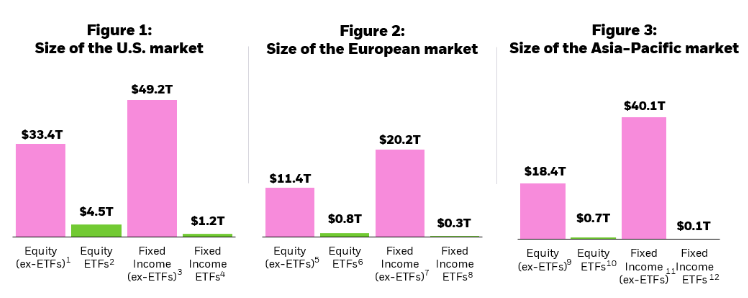

The ETF industry has grown immensely over the past two decades, as investors switched gradually from active investments to passive investing. According to iShares, despite this growth, the market share of ETFs is still relatively low compared to the total market, as shown in the next graphs. For instance, while U.S. Equities ETFs have some $4.5 trillions of AUMs, they only represent some 12% of total equity assets, thus there is still plenty of growth ahead both from potential overall market growth plus market share gains to non-ETF assets.

ETF assets (iShares)

While WisdomTree is not among the largest ETFs providers in the U.S., it is also expected to have tailwinds from industry growth and also from its one growth initiatives. The company has grown historically both organically and through acquisitions, which has led to a much more diversified product offering and AUM distribution, than some years ago. Additionally, it also has expanded its product offering to crypto and digital assets, being complementary to its core offering.

Digital Assets (WisdomTree)

According to WisdomTree’s most recent AUM data, most of its AUM are in the U.S. (68% of total), while the rest is in Europe. Its largest product is U.S. equity, representing some 30% of total AUM, followed by commodities & currencies (27%), and fixed income (18%). This means that WisdomTree is now well diversified regarding asset classes, a very different profile than I last covered the company, when it was heavily exposed to equities, namely international hedged equities in European and Japanese stocks.

As the company generates the majority of its income from ETF fees, which are directly related to AUM, this means its growth prospects are also mainly tied to its size. Indeed, the ETF industry is to a large extent based on pricing, which means that margins are relatively low and are not expected to change much in the foreseeable future.

Moreover, regarding earnings growth, the company can also report some growth due to improved efficiency, trough cost cutting or simplifications of processes, even though significant gains in this area may be difficult to achieve in a recurring way.

Over the long term, by being completely focused on exchange traded products, WisdomTree is in a good position to benefit from the structural trend of money moving away from active products towards passive investing, boding well for its growth over the next few years.

Financial Overview

Regarding its financial performance, while WisdomTree has a good growth history since its inception, supported by rising AUMs and an expanded product offering, its growth in recent years has been more muted.

In 2021, the company was able to report positive net inflows throughout the year, which together with positive market returns, led to a significant increase in AUM to more than $77 billion at the end of the year, compared to $67 billion at the end of 2020. This AUM growth supported revenues, which increased by 22% YoY to $294 million, while its net income was $61 million (+43% YoY). Its return on equity ratio was 18.6% in the year, which is a good level of profitability.

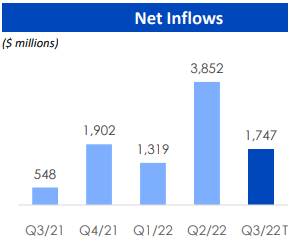

During the first nine months of 2022, WisdomTree continued to report positive net inflows despite the challenging market backdrop, even though total AUMs have declined due to lower market returns to some $70 billion at the end of Q3.

Net inflows (WisdomTree)

Due to lower AUMs, its revenue declined to $72 million in Q3 (-9% YoY), and its adjusted net income was $9.3 million (-43% YoY) as cost increased due to inflationary pressures and compensation accruals.

Going forward, according to analysts’ estimates, WisdomTree is expected to grow gradually its revenues in the coming years to some $370 million by 2025, while its net income is not expected to improve much and be about $58 million by 2025. Given that a large part of the company’s revenues are directly related to capital market returns, investors should take earnings estimates with caution as the probability of error is quite high. Despite that, WisdomTree has been able to gain net inflows in recent quarters, which was a tough period for financial markets, showing that its business strategy is bearing fruit and this should likely lead to higher revenue and earnings in the next few years.

Regarding its balance sheet, WisdomTree had a net debt position of only $15 million at the end of Q3, which means that it has a solid financial position and does not need to retain much cash in the near future. Despite that, its quarterly dividend has been stable since 2018 at $0.03 per share, which at its current share price leads to a dividend yield of about 2%.

Conclusion

WisdomTree has an interesting business profile due to its focus on exchange-traded products, which should benefit from industry growth tailwinds over the next few years. However, I don’t see any real competitive advantage over its peers to make it much larger, which means that most likely WisdomTree will remain a relatively small asset manager in the near future.

Regarding its valuation, it is currently trading at more than 22.5x forward earnings, at a premium to its own historical valuation on over the past five years (19.8x earnings), and also at a premium to its peers’ average (about 14x earnings). Therefore, I’m not particularly bullish on WisdomTree right now, and would wait for a lower price to consider its shares.

Be the first to comment