tdub303

Synchrony Financial (NYSE:SYF) operates in a highly cyclical industry. But it stays robust amidst macroeconomic volatility. Revenue growth and margins are impeccable, showing a stable performance. Also, its fundamental soundness is evident with its excellent and conservative liquidity position. This aspect allows it to remain sustainable and well-capitalized even during another recession.

Moreover, dividends are continuous with a decent yield. The stock price moves sideways, although quite hammered. Even so, a potential undervaluation can make it an ideal entry point for investors.

Company Performance

The consumer finance industry tends to operate in a highly cyclical environment. And Synchrony Financial is no exception to this trend. The past two years have hindered its growth. But thankfully, it has navigated the rugged market with ease and prudence. Its operational efficiency and prudent portfolio management have been its cornerstones.

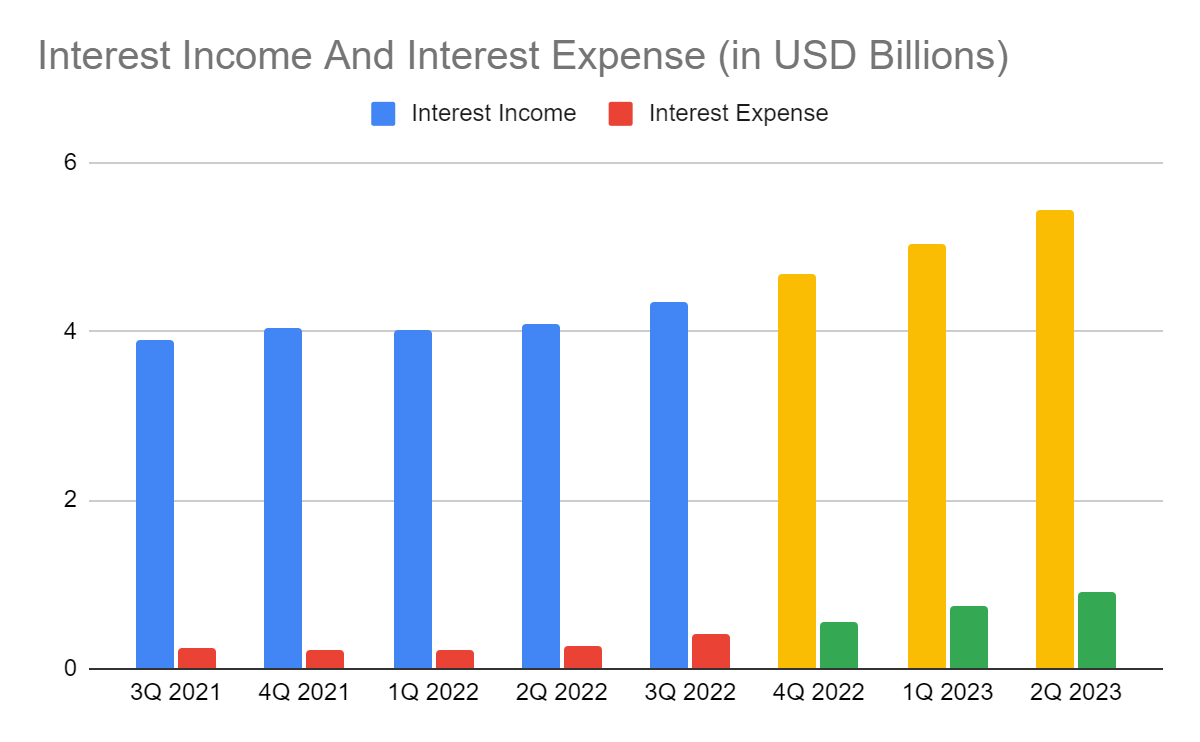

Today, Synchrony shows its resilience and durability through its well-balanced growth and viability. Interest income amounts to $4.34 billion, an 11% year-over-year growth. We can attribute this decent growth to several key factors. First, its core competencies include its deep ties with massive retailers. It has credit card contracts with e-commerce giants, such as Amazon (AMZN) and eBay (EBAY). It even reaches one of the East Asian Giants named Cathay Pacific (OTCPK:CPCAY). These affiliations ensure a solid revenue stream to sustain its capacity and expand. It is even more vital today as e-commerce and tourism fire up.

Interest Income And Interest Expense (MarketWatch And Author Estimation)

Second, SYF maintains prudent portfolio management. We can see it in its excellent credit quality. Loans are well-diversified and balanced and cover a wide range of industries. The largest portions are composed of home and auto and digital loans. It is no surprise since these are the primary products of the company. Also, interest rates and property prices are skyrocketing. As such, more borrowers turn to reputable companies offering more favorable borrowing costs. Despite the exciting loan growth, SYF remains conservative. Its substantial credit loss allowance is logical since many loans are unsecuritized. We can also see its impressive portfolio in investment securities. These are debt securities, which often fare well in a high-inflation environment. Most of these are government-backed debt securities, making them more inflation-linked. They have a better hedge for valuation losses, allowing them to maintain high yields.

Third, its continued digitalization improves its efficiency and widens its coverage. It helps SYF to cater to more individuals and businesses. Even better, e-commerce continues to boom and expand. It is one of the manifestations of digital transformation. As such, cashless transactions have increased over the past decade. It has accelerated in the last two years, making digital wallets and credit cards a staple. In turn, Synchrony products have more appeal to its partner companies and customers.

Lastly, macroeconomic changes appear to work in its favor. Inflation leads to higher interest rates. The interest rate hikes help SYF generate more loan yields as more people turn to it. It hypes up some more, given the continued inflation lull. The current pattern increases the purchasing and borrowing power of customers and businesses.

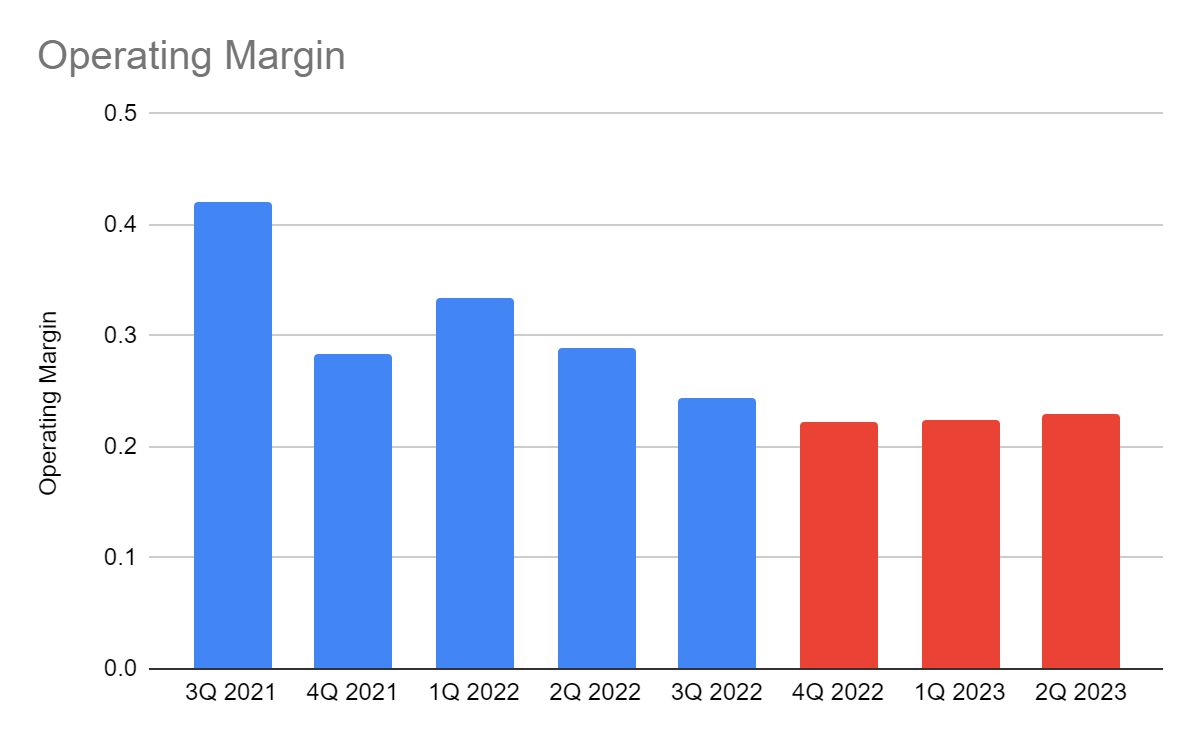

Meanwhile, interest expense shows a drastic change. It should not be a surprise since most deposits are interest-bearing. Despite this, the difference between interest income and expense remains stable. Also, non-interest expenses are still manageable, showing efficient asset management. Non-interest income is only half its value in 3Q 2021, driven by the 26% increase in loyalty programs. The operating margin is now 24% versus 42%. Even so, the company remains viable and stable. Also, it shows balanced growth while ensuring customer satisfaction and stabilizing expenses.

This year, I expect more enticing prospects for Synchrony. The inflation lull continues, which can help stabilize interest rate increments. The e-commerce and travel hype may continue. I will discuss more of them in the next section. Interest income may increase further. Meanwhile, the operating margin may stabilize before bouncing back.

Operating Margin (MarketWatch And Author Estimation)

How Synchrony Financial May Fare This Year

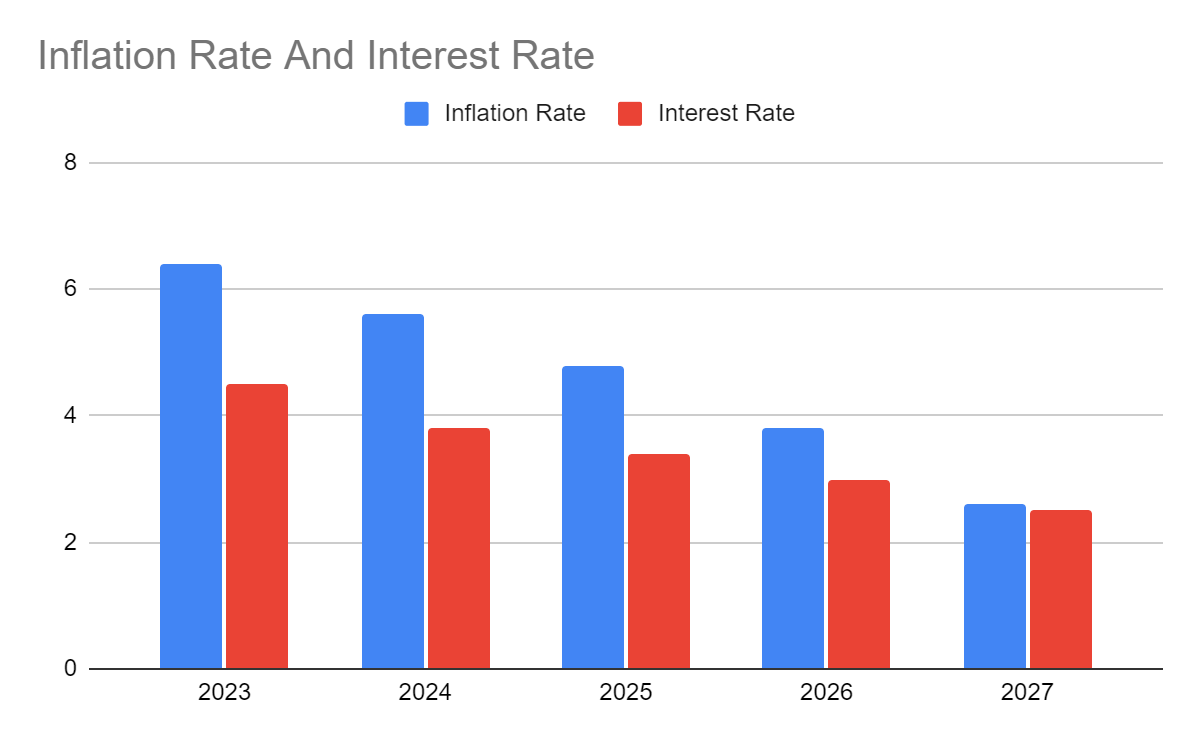

Synchrony Financial is a promising General Electric (GE) spin-off, which keeps expanding today. It remains an industry staple as its popularity increases. Various factors may contribute to my optimistic view of its performance this year. First, macroeconomic indicators may become more manageable this year. Thanks to the decreasing pattern of inflation. Projections are more optimistic, unlike the bleak estimates in 2Q 2022 when it peaked at 9.1%. But at 7.1% today, it may keep decreasing further. The hype in some industries, especially real estate, cools down. Other countries, like the G20 members, also see an inflation downtrend. With that, I expect interest rates to increase some more, but increments may slow down. I also set its peak at 4.5%, lower than the consensus of 5-5.25%. Mortgage rates may go in the same direction before stabilizing. These changes may increase the borrowing capacity of individuals and businesses. Hence, the purchase volume of its products may keep increasing.

Inflation Rate And Interest Rate (Author Estimation)

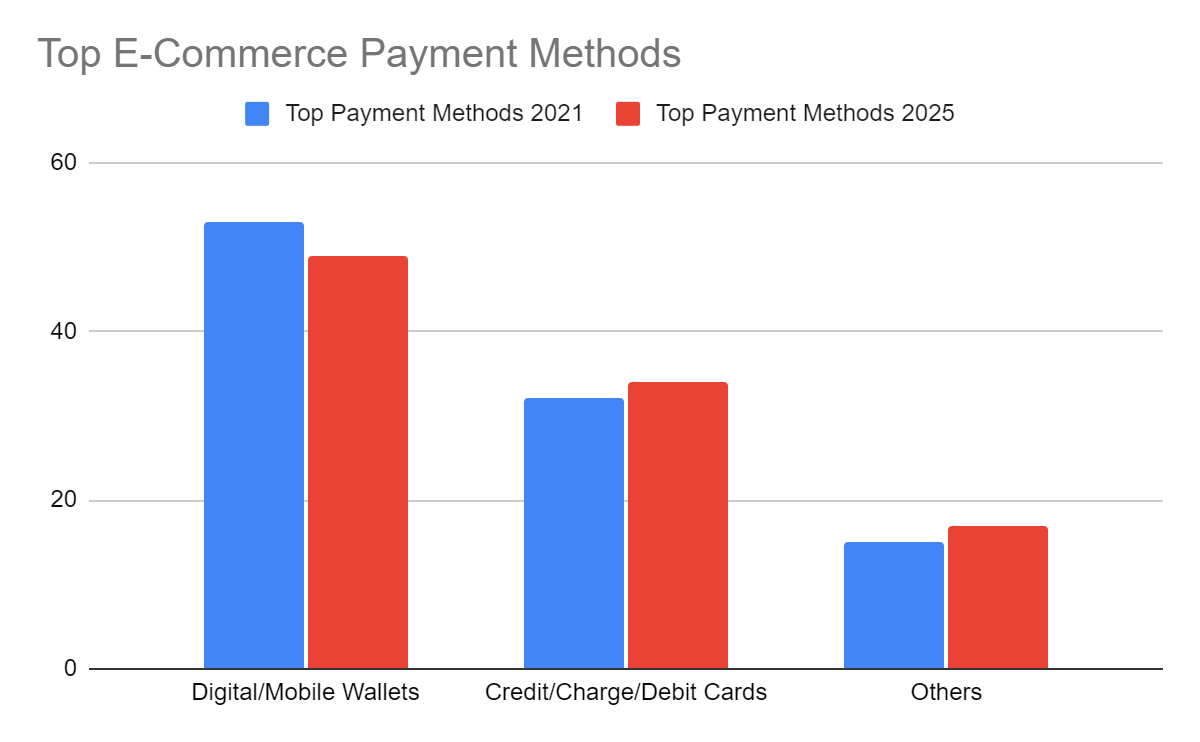

Digital transformation is a potential growth driver for the consumer finance industry. In recent years, credit cards have become more popular as cash transactions decreased. It is essential today as e-commerce expands further. It allows virtual transactions, making more consumers shift to cashless methods. As of today, 27% of the population is part of e-commerce shoppers. Over 70% remains unpenetrated, so there may be untapped potential across regions. If internet access improves, especially in MEA, more markets may be penetrated. By 2025, e-commerce sales are expected to reach $7.4 billion. This expansion may have a direct impact on SYF, given its affiliation with AMZN and EBAY. Right now, cards comprise 32% of global e-commerce payment methods. It is estimated to increase to 34% in the following years. Credit cards remain far second to mobile wallets. But SYF has a deep connection with one of the leading mobile payment methods, PayPal (PYPL). As such, it remains an industry staple, especially in e-commerce. More prospects may be anticipated.

Top E-Commerce Payment Methods (Statista)

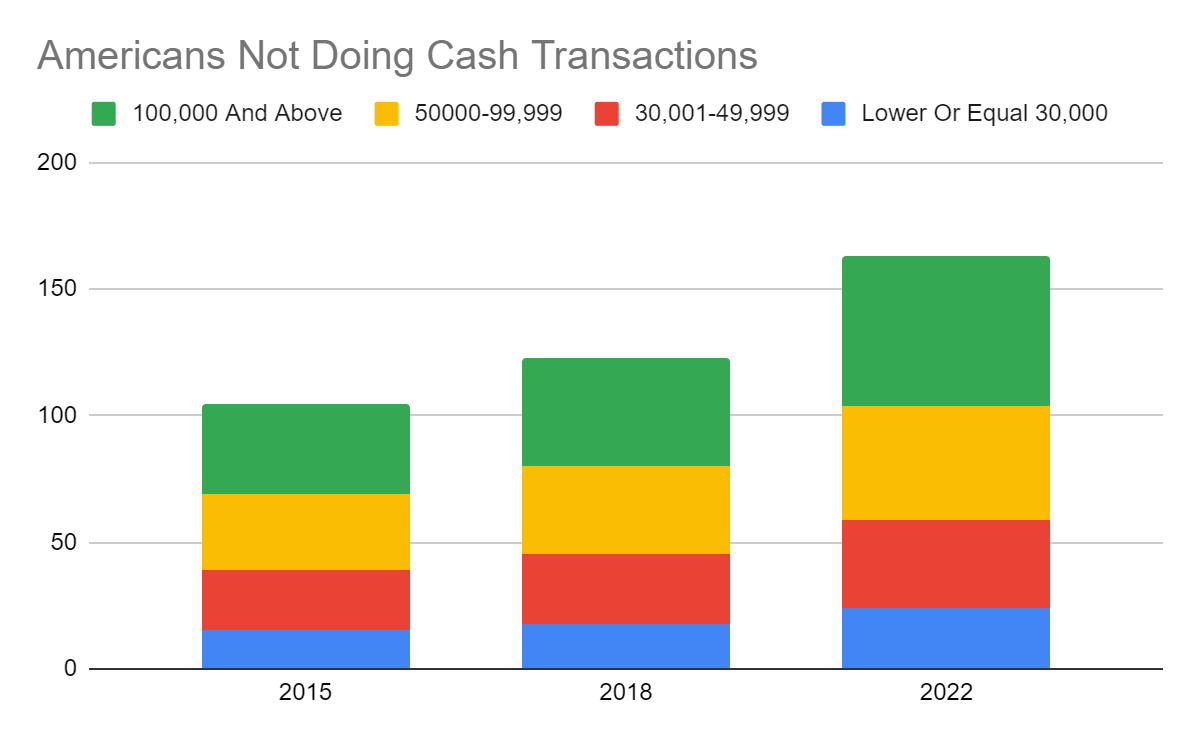

The prevalence of hybrid work setups may also become another growth driver of SYF. As business activities are done remotely, more transactions may become cashless. Even for personal use, cashless transactions are now the preferred payment method. As of 3Q 2022, 41% of Americans no longer used cash for their transactions. Even more noticeable is the inverse relationship between cash usage and income levels. We can see that as income levels increase, cash transactions decrease. But overall, cash transactions across all income levels are decreasing. This pattern is consistent with mobile wallets and credit cards. Another driving force will be the travel hype this year. It can expand the credit card performance of many companies. SYF and CPCAY may move in tandem further. Over 90% of individuals have travel plans this year, and over 80% will either spend more or the same as in 2022. Moreover, search traffic for international flights is now 62% versus 55% last year. With the easing of restrictions and increased business activities, tourism may accelerate.

Americans Not Doing Cash Transactions (Pew Research Center)

Of course, we must not discount the potential recession. But I believe, the bubble burst in the home and auto market is far from reality. First, property and car inventories remain low. Although sales are cooling down, their availability cannot meet the current market demand. The unemployment rate remains far from the Great Recession. It remains low and stable. Income levels are also higher than in the last two years, given the current average wages in the US. Therefore, customers still have decent buying and borrowing power. The purchase volume of SYF products may remain stable.

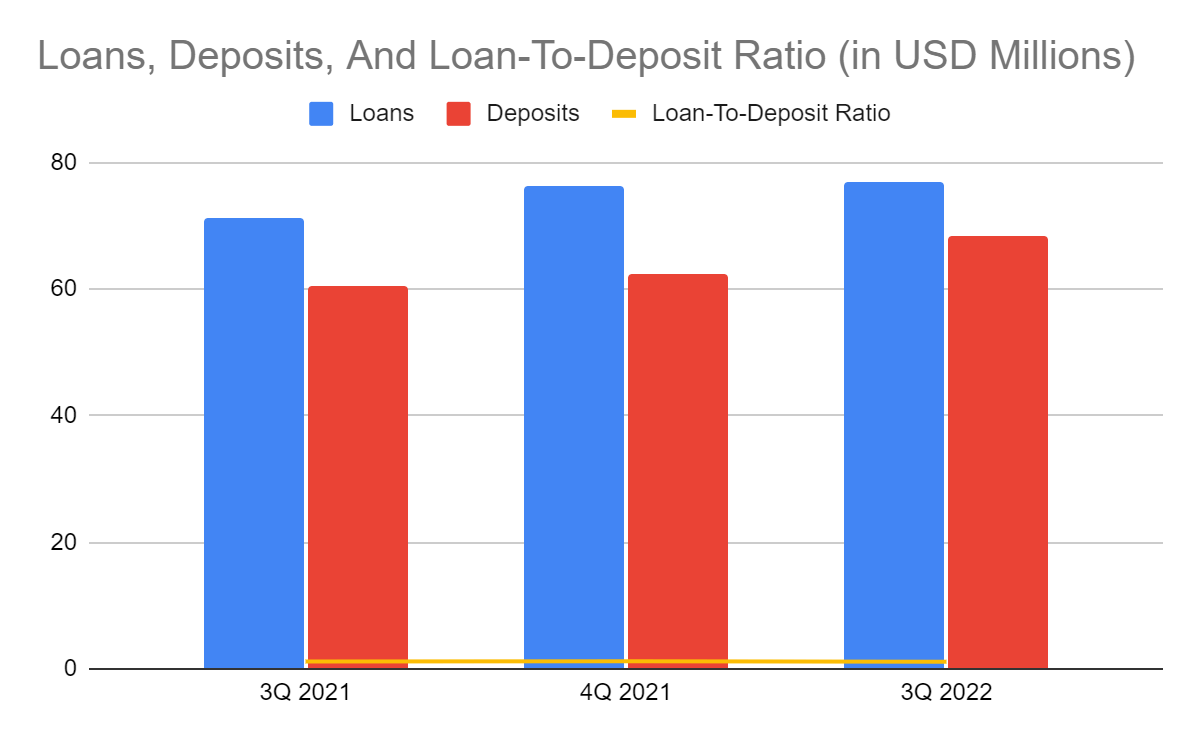

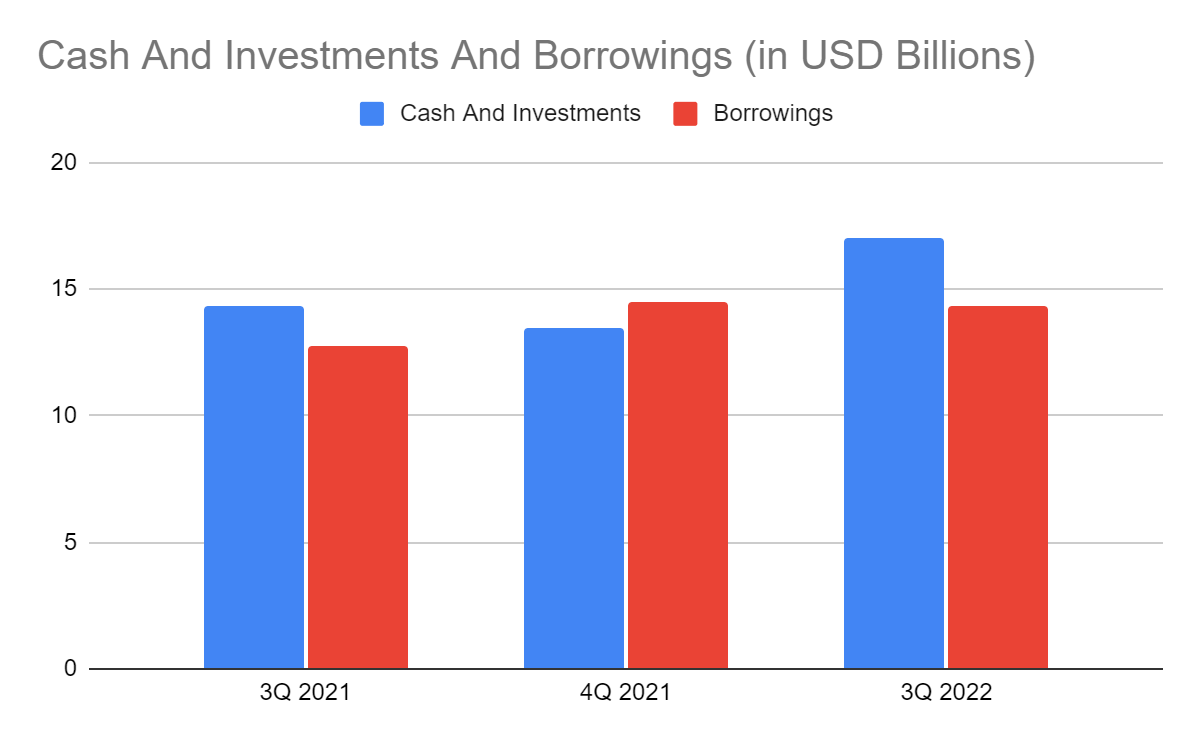

But what makes Synchrony a solid company is its market and financial positioning. Its popularity and deep customer ties with industry stalwarts make it durable. Even more important is its adequate capacity to sustain its operations. Loans are interest-sensitive and well-diversified across different products. They have excellent quality as delinquencies remain manageable. Even better, provisions remain above 10%, showing conservative loan management. The loan-to-deposit ratio is decreasing, which may work better in a high-interest environment. It must increase its reserves to ensure liquidity, and right now, it is on the right path. SYF may also increase interest rates to entice more deposits, improving liquidity. Moreover, cash reserves remain adequate. Cash and investments can cover all borrowings even in a single payment. Net Debt/EBITDA is only 0.49x, showing that the company earns more than enough to cover borrowings. It has more reserves to sustain dividend payments. It is no surprise it raised shareholder value by $1.1 billion, most of which came from share repurchases. Synchrony Financial stays a secure company with balanced growth and fundamental stability.

Loans, Deposits, And Loan-To-Deposit Ratio (MarketWatch)

Cash And Investments And Borrowings (MarketWatch)

Stock Price

The stock price of Synchrony Financial has moved sideways after its continued rebound. But it remains lower than the 2022 highs and even pre-pandemic averages. At $33.47, it has been cut by 30% from its price last year. Its recent PTBV of 1.51x shows an upside potential. If we use the average multiple of 1.74x and the current TBV multiple of 22.1x, the target price will be $38.45. It shows a potential upside of 14% in the stock price. At first, I was bothered by the changes in tangible book value and share repurchases. But it is a wise move to preserve the intrinsic value of the stock. The current macroeconomic volatility still affects the company. But the thing is, SYF has adequate capacity to sustain its share repurchases. The intrinsic value using the PTBV multiple is logical for the company.

Moreover, dividends are enticing as they stay consistent and well-covered. They have a decent dividend yield of 2.7%, which is way higher than the S&P 500 average of 1.68%. Also, the dividend payout ratio is only 14%, showing adequacy. To assess the stock price better, we will use the DCF Model.

FCFF $915,000,000

Cash $12,000,000,000

Borrowings $14,300,000,000

Perpetual Growth Rate 4.8%

WACC 9.2%

Common Shares Outstanding 458,900,000

Stock Price $33.47

Derived Value $42.45

The derived value also conveys stock price undervaluation. There may be a 27% upside in the next 12-18 months. Investors may see a potential entry point to make a position.

Bottom line

Synchrony Financial is a secure and robust company in the consumer finance industry. It balances growth with fundamental stability, given its sustained viability and excellent liquidity. It stays adequate to sustain dividend payments with decent yields. Also, the stock price shows undervaluation, which may be an entry point to make a position. The recommendation is that Synchrony Financial is a buy.

Be the first to comment