FatCamera

Summary

I recommend to hold off any purchase of American Well Corp. (NYSE:AMWL). I think AMWL’s biggest concern, like that of other shareholders, is when the company will begin making money. AMWL stated that they are optimistic about the future and that their path to profitability in the long term has not changed, but the uncertainties with the macro environment in 2023 forces me to seek more margin of safety.

Company overview

AMWL is a telehealth company. The company offers complete digital healthcare solutions for hospitals, insurance companies, employers, and doctors.

Too many resources under utilized

Unfortunately, modern healthcare is ineffective, costly, convoluted, and disjointed. As a result, the entire ecosystem faces significant difficulties. My opinion is that telehealth can be crucial tool in resolving these important underlying problems.

By far, the most significant problem that telehealth solves is wasteful use of resources. The shortage of primary and specialty care providers is a problem in both urban and rural areas of the United States, making access to appropriate care one of the most pressing problems in the American healthcare system today. The patient’s condition may worsen rapidly, they may choose to forego treatment, or they may miss out on an otherwise curative opportunity because of the delay in receiving care. The emergence of new diseases, such as the deadly COVID-19, and natural disasters only exacerbate these access problems. COVID has clearly showed how fast limited resources can be depleted if there is no statewide or national back-up.

A lot of these problems, in my opinion, can be solved by telehealth. It removes obstacles to access, allowing for more effective distribution of primary, urgent, and emergency care. Patients can get care when it’s most convenient for them, without having to worry about spending a lot of time traveling. With telehealth, hospitals can also consult with experts in real time to improve diagnosis and treatment.

Telehealth also helps to reduce overall cost of healthcare

In 2021, Americans have spent an unprecedented $4.3 trillion on healthcare. I think telehealth can play a major role in helping to curb these rising costs. In response to the need for low-acuity episode care at lower costs, telehealth visits can be used to satisfy the demands of health plans, health systems, and consumers. Telehealth can also be used by healthcare systems to improve operational efficiencies such as resource utilization. The reduction of caregivers’ commute times and better distribution of their workloads are two prime examples of this type of application.

AMWL platform health plans differentiates from peers

I believe that the AMWL platform for health plans includes a number of features that set it apart from competitors and therefore should support its ability to maintain pricing power. To begin, because AMWL serves the needs of a healthcare network in addition to AMG, its physician referral base is considerably larger than that of the latter. Network effects will likely favor AMWL’s provider-facing platform, making it the preferred choice among medical professionals. Second, the clinical aspects of AMWL’s programs are also improved by the breadth of their physician network and their incorporation into the processes of the healthcare system as a whole. This paves the way for a seamless transition to in-person care in the event it becomes necessary without disrupting existing data or plans. Third, it is more difficult to establish a customer base for a health system without an existing network of patients. This is especially true for high-value products like virtual primary care plans, which are in high demand among health plans and employers. Fourth, AMWL’s features are tailored to the needs of health plans with provider assets or a preference for providing the technology to community physicians.

Strong flywheel effect

With its flexible infrastructure, AMWL can expand in step with its customers’ demands for digital health care services. Clients typically start with a single use case. As the scope of a client’s digital care solutions expands, they will likely need to add modules to assist new use cases applicable to a wider range of patients or members. There are currently over 40 modules or programs in the AMWL product line, each of which provides the workflows necessary to deliver care across myriad of unique use cases while keeping a uniform appearance for each customer. AMWL’s growing capabilities make it possible for them to work with both telehealth industry newcomers and established, rapidly expanding market leaders.

In essence, AMWL built its system so that it would continue to benefit its users even as their needs changed and expanded. This design, in my opinion, gives AMWL a significant flywheel effect. The greater demand for AMWL’s services, in turn, makes it easier for AMWL to recruit doctors. In addition, as more information is gathered in this loop, AMWL can more effectively release products that address patients’ concerns.

The converge platform

AMWL’s original platform was compatible with 160 telehealth systems before Converge was implemented. Due to the inefficiency of this, and anticipating a spike in demand for telehealth services in 2020, AMWL developed a single platform called Converge to unify all of its services across all devices and all geographic locations. Converge is designed to give doctors, patients, and insurers each their own personalized screens. This enables users to appear on a patient’s screen anywhere, allowing for more flexible and responsive care delivery. Patients can sign up for telehealth visits and receive text messages notifying them when clinicians are available, eliminating the need for them to wait in an online waiting room for extended periods of time. With Converge’s help, communication between various parties, such as health care providers, insurers, and government agencies, is streamlined, leading to more time and money saved.

Strong 3Q22 results but still faces near-term uncertainties

All in all, AMWL’s 3Q22 earnings report was better than expected. The company’s total revenues were slightly ahead of consensus, and its adjusted EBITDA was significantly above. Following this solid performance, management has reduced its adjusted EBITDA guidance for FY22 from -$195 million to -$185 million at the midpoint. However, management has signaled a shift in attention to the lower end of their guided revenue range, which they have maintained at $275 million to $285 million for FY22. They also reaffirmed 2022 as a transition year, during which they will invest heavily in R&D to upgrade and migrate customers to their Converge platform.

Valuation

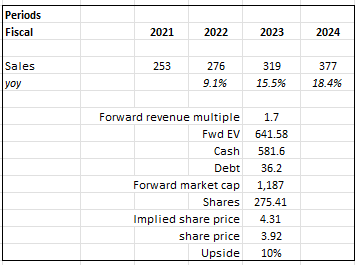

I believe AMWL is worth 10% more than the $3.92 share price today. I note that AMWL is still experiencing a very strong long-term secular trend that should enable it to grow over the long-term so long as it continues to enhance its product. However, as I stated earlier, investors are now focusing more on profitability than growth. As such, management upcoming commentary during 4Q22 earnings will be a key catalyst.

While my model indicates minimal upside today, the key variable is valuation multiple. If management can show strength in their guide to profitability, I believe AMWL could see a valuation re-rating upwards, which will further boost the upside for the stock.

Own calculations

Risks

Weakness in internal controls

Although AMWL has taken steps, such as hiring a new CFO and launching new initiatives, to address the material weakness in financial controls, it is usual for this to be remedied gradually, resulting in cost increases to the G&A line.

Higher interest rate environment hurt discounted value

Even though it’s not specific to AMWL, I think investors’ wariness of stocks with uncertain future cash flows is a contributing factor here. Even though AMWL has no debt, a rise in interest rates hurts companies like AMWL that are valued using DCFs because of their longer time horizons.

Conclusion

I believe that AMWL is not a good investment at the moment due to the company’s lack of profitability and uncertainty surrounding the future of the healthcare industry.

Be the first to comment