Feverpitched

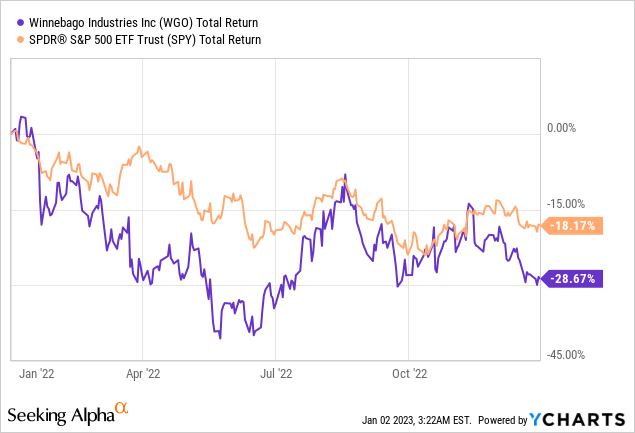

Winnebago Industries, Inc. (NYSE:WGO) offers premium recreation vehicles (RV) and marine products to support outdoor recreational activities in North America. Like many other industry stocks, its stock price has been declining for almost a year now. However, I think WGO is an overlooked opportunity, given the improvement of its profitability and market positions. Here I will share some of my thoughts.

The recent quarter is actually not bad

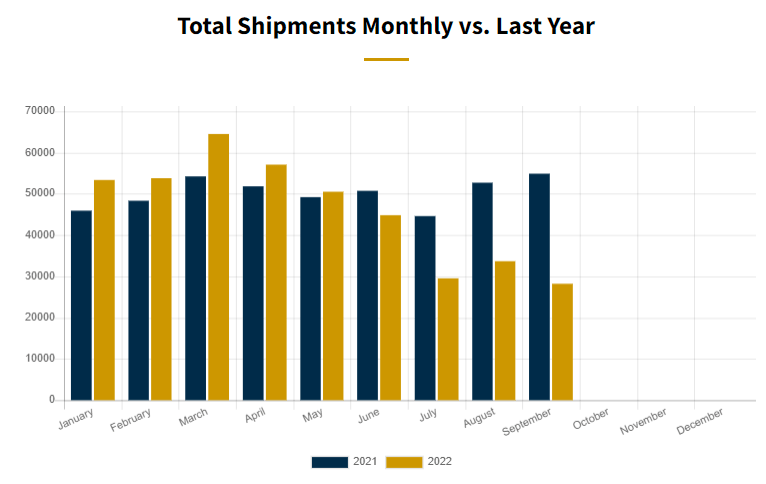

WGO has both EPS and revenue beats for fiscal 2023 Q1. The revenue declined 18% to $953M compared to $1.2B last year. Gross margin also consolidated to 16.8% but still higher than pre-pandemic levels. The towable segment was down 46.7% to $434M due to demand weakness and the normalization of dealer inventories. The motorhome segment grew 10.1% to $463.3M, mostly due to price increases. The marine segment is the most significant driver growing 65.7% to $131.4M. The gross margins, EBITDA margin, and backlogs are also all higher than the prior year. Overall, WGO’s sales perform better than THOR Industries (THO), which decreased 21.5% YOY. RVIA (RV industry association) also has reported a worse 54% RV shipment drop. So WGO is outperforming the industry and has shown some resiliency under headwinds.

RV shipment (RV industry association)

The fear of another cyclical disaster

Some of the fear for WGO may come from its historical performance during the economic downshift. In the 2008 crisis, WGO dropped 89%. In 2018, WGO dropped 57% under concerns about demand vs. supply and tariff impacts on profits. During the downturn this year, WGO dropped 47%. While the stock price has come down a lot, it is still not at the magnitude of previous ones. The macro environments have not bottomed yet, meaning the business environment for WGO is not getting better. The recent WGO price decline is discounting future earnings misses or surprises as it is unclear how WGO can hold its financial position for the next 12 months.

How different is WGO pre vs. after COVID

During the conference call, WGO CEO shared his thoughts about WGO’s strategies and progress in recent years. The company is much different now versus pre-COVID in 2019. First, 1B revenue has been added from acquired businesses. The Newmar and Barletta brands both are fast growing and will be bigger and more profitable in the future, which provides good diversification of their product lines during recessions. Secondly, the profitability of all business lines is dramatically different and should be sustainable moving forward. Although the recent quarter was under the impact of multiple headwinds such as supply chain disruptions, inflation, interest rates, etc., WGO still managed to get a Gross Margin of 16.8%. There is also a 50M impacts from the Mercedes-Benz Chassis recall, which is temporary. The management believes that WGO could maintain a double-digit EBITDA margin even in a more challenging environment like right now. Thirdly, WGO only had 9% of the share in RV space in 2019 and 3.3% in 2016, now, they have 13 points of the share. They had 0 shares in the marine pontoon market in 2019, now they have almost 7%. I believe WGO is a much stronger company than before, which should offer more resilient investment returns.

Previous acquisitions proved to be good

Acquisition deals are usually not a good thing for investors as companies often overpay and synergetic expectations often turn out to be not as good as expected. Since 2017, WGO has made four acquisitions: Grand Design, Newmar, Chris Craft, and Barletta. All of them offered 30%+ CAGR revenue growth in the last three years. The marine segment is especially under an exploding growth trajectory, recently 66% YOY and accounted for 14% of our revenue. Barletta was a startup only founded just five years ago and acquired in August of 2021. Now, its market share approaches almost 7%. This shows a lot about the capital allocation capabilities of the management.

An evaluation that is hard to resist

WGO’s recent 5-yr average earning is $189.7M while possessing a tangible book value of only $200M. This showed its strong historical operational efficiency. The company has no long-term debt before 2017. Their long-term debt load has increased significantly to $590M because of those major acquisitions. This is a little concerning. However, these debts were raised when interest rates were low. Around 200M free cash flow should cover debt interests well enough (TTM interest expense $37M). WGO also rarely dilutes its shares as the weighted average shares outstanding stayed at the 30m to 32m level since 2017.

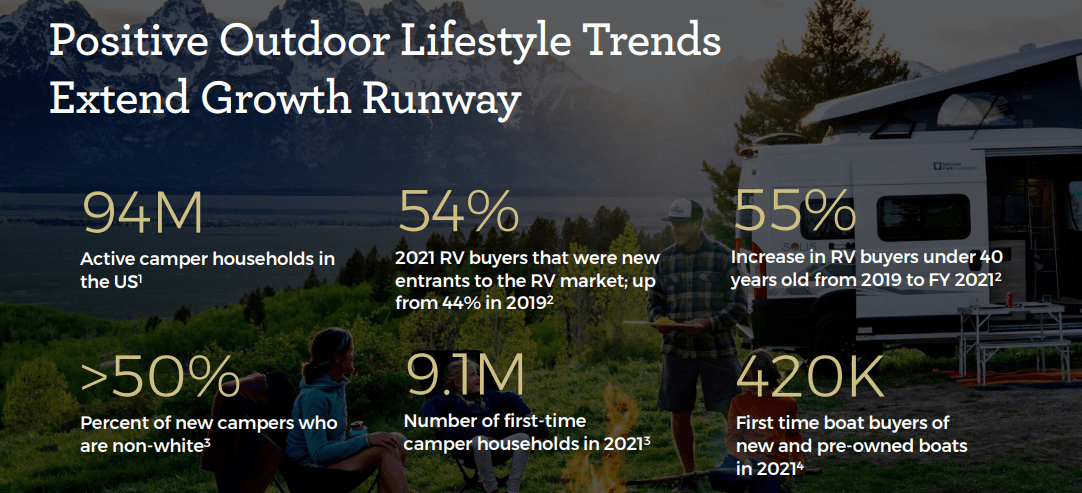

The management recently released its 2025 strategic targets with revenue of $5.5B, a Gross margin of 19%, and a free cash flow of $400M. If WGO can achieve this, the current $1.6B market cap will be extremely cheap (25% free cash flow return). Given this target is only based on a future CAGR of 5%, which is totally achievable. Given the positive trends of outdoor lifestyle (below), WGO is in a great position to offer shareholder returns (current P/E is at a historical low).

Outdoor Recreation trend (WGO investor presentation)

Bottom Line

WGO has proven to be a profitable and quality company. There are no risks of bankruptcy, and the long-term industry trends should be very positive. As the current market and macro conditions continue to deteriorate, it should offer a great opportunity for investors. Yes, WGO is not a fast grower and operates a hot business. However, it can often be overlooked by the market which gives an advantage to normal investors.

Be the first to comment