onurdongel/iStock via Getty Images

VTOL Looks To Deliver On The Upside

Bristow Group (NYSE:VTOL) has many bullish factors going in its favor. The company deals in oil and gas flight services, fixed-wing services, and government services. The underlying fundamentals for Bristow’s business, including offshore energy and government services, are improving significantly. Some of the company’s international businesses are also showing promise. But the bigger driver will be the new government contracts. The acquisition of British International Helicopters will also supplement the organic growth.

The stock is relatively undervalued versus its peers. The company’s cash flows depleted in 1H 2022 following the buy-in agreement of the PBH (power-by-the-hour maintenance program). In this environment, investors might want to buy with the expectation of a steady return in the short-to-medium term.

Strategy In Different End Markets

VTOL’s November 2022 Presentation

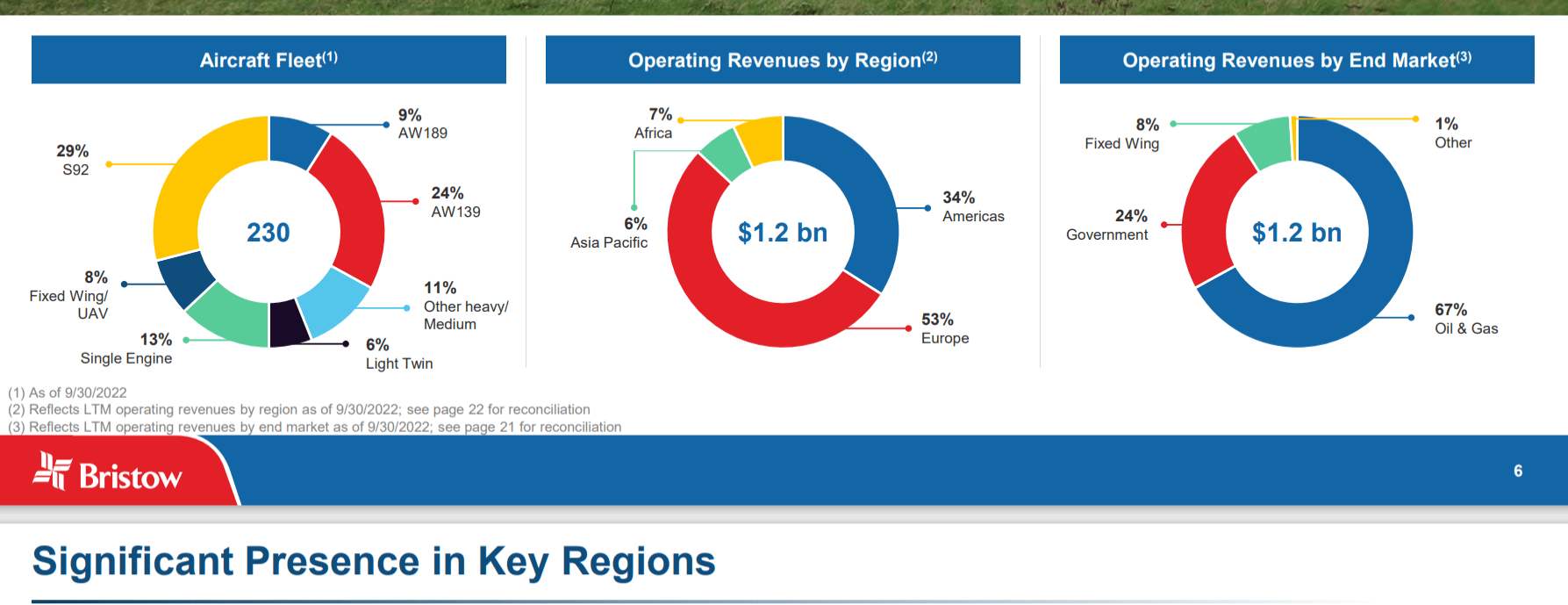

The offshore energy industry recovered in 2022. While the US offshore rig count remained unchanged at 16 in Q3 2022 compared to Q2, it inched up to 18 in the first week of December. In this environment, VTOL will benefit from new government contracts and improved activity levels at the fixed-wing business in Australia. The recent contracts propelling the company are the Netherlands SAR (search and rescue) contract and the Dutch Caribbean Coast Guard contract. The UK SAR contract has also increased pace in recent weeks. The UK SAR contract accounted for ~21% of its FY2022 revenues. Its recently acquired British International Helicopters (or BIH) has a contract with the UK Ministry of Defense. The company would leverage this position to gain additional contracts in Cyprus, Brunei, and Oman.

VTOL’s November 2022 Presentation

In the oil & gas business, the company looks to gain the advantage of the improving US Gulf of Mexico activity. Outside of the US, the management sees recovery in Nigeria and new contacts in Brazil. Among other services, it secured a multiyear search and rescue contract in Norway. However, these contracts are unlikely to take effect before 2H 2023. Overall, the company’s topline should get a fillip in 2H 2023.

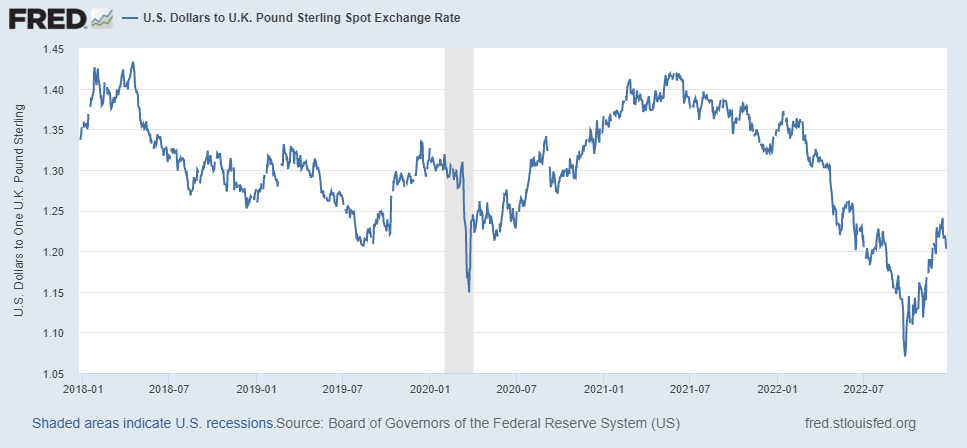

FRED Economic data

Investors may note that foreign currency impacts the company’s earnings. The primary headwind for VTOL is the US dollar’s appreciation against the British pound. By Q3-end, the UDS appreciated 8.5% against GBP compared to Q2. Since then, however, USD has depreciated by a similar margin. A weaker USD is a positive for VTOL’s margin. According to its estimates, for every GBP movement of 0.01, the US dollar exchange rate will affect the projected FY2023 adjusted EBITDA by ~$1.5 million.

FY2023 Forecast

Bristow Group’s Q2 2023 Press release

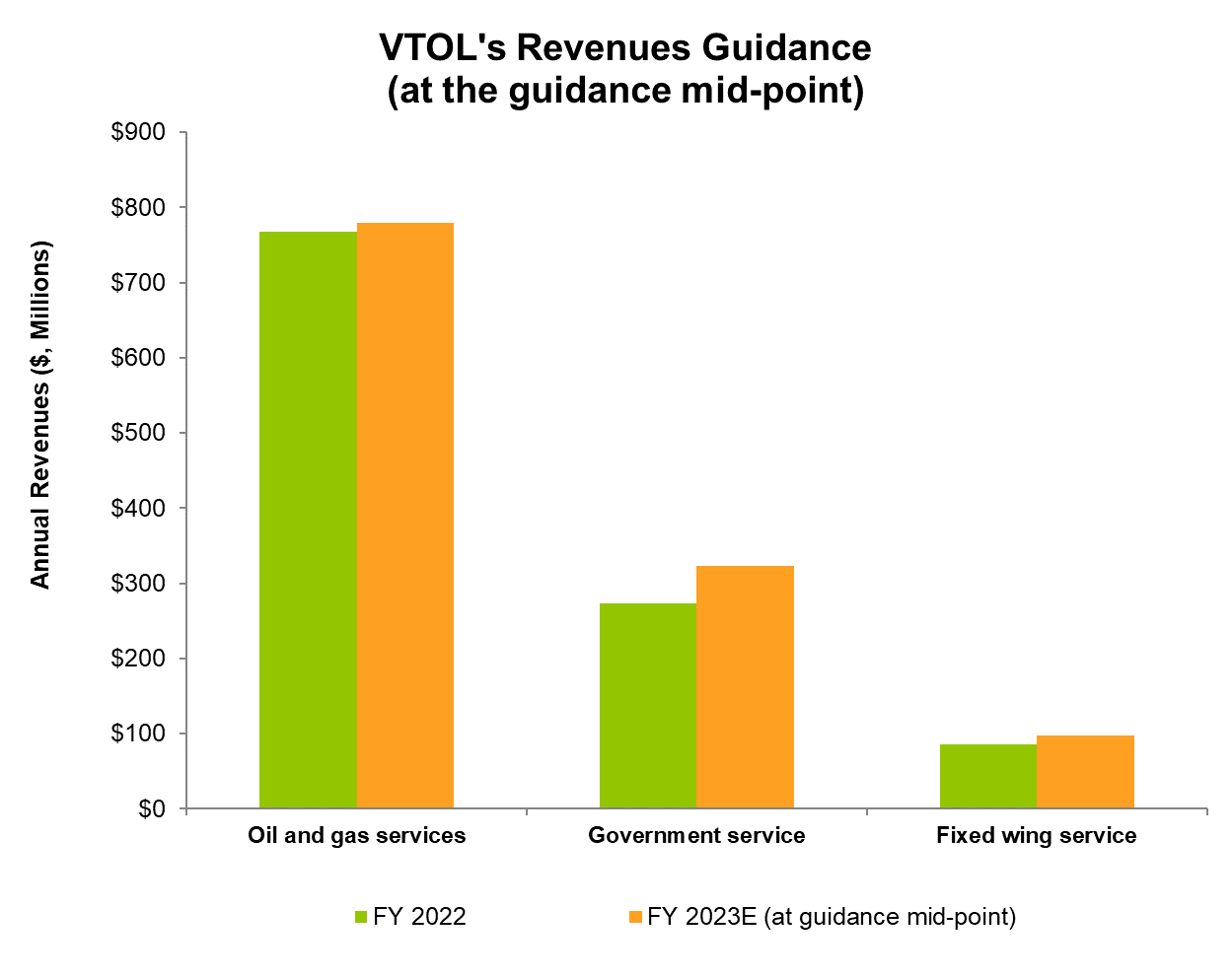

In FY2023, the company’s management expects revenues in the Oil and gas services segment to increase by 2% (at the guidance mid-point) year-over-year. The Government service segment can increase by 18%, while revenues in the Fixed wing service segment can increase by 14%. The EBITDA guidance for FY2023 is $150 million (at the guidance mid-point) is nearly unchanged compared to the FY2022 adjusted EBITDA.

Explaining Q2 2023 Performance Drivers

VTOL’s Filings

In Q2 2023, Bristow Group’s Fixed wing service segment performed better than the rest. Revenues in this segment increased by 12% quarter-over-quarter in Q2 due primarily to additional lease payment collections from Cougar Helicopters. Improved asset utilization in the African region contributed to the growth. Similarly, revenues from fixed-wing services increased due to higher utilization. Although revenues from Government services remained unchanged from Q1 to Q2, sales in the Oil and gas services segment increased modestly (1% up). Higher utilization of oil and gas services in Africa contributed to the rise.

Adjusted EBITDA decreased by 3% due to a higher amortization charge related to the acquisition of British International Helicopters (or BIH). However, net income gained significantly (315% up) in Q2. In Q2, VTOL recognized a $10.2 million foreign exchange gain because the US dollar strengthened the British pound and other currencies. Also, during the quarter, it disposed of three helicopters and recognized a net gain of $3.4 million as opposed to a $2.1 million loss on the sale of assets in the previous quarter.

Cash Flows And Leverage

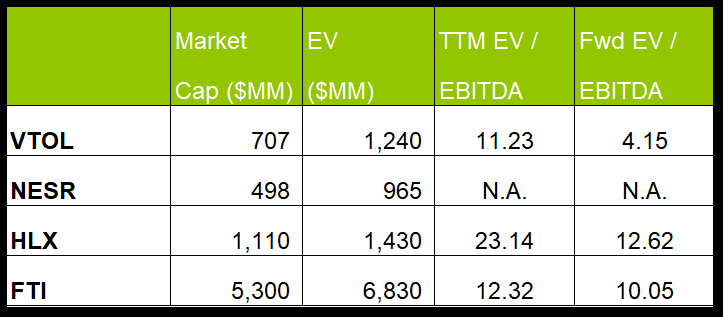

VTOL’s debt-to-equity was 0.66x as of September 30, 2022, which was higher than the peers’ (NESR, HLX, and FTI) average (0.42x). Its liquidity was $251 million as of that date. In Q2, it funded PBH buy-ins, the purchase of BIH, and share buyback from its liquidity and cash flows.

VTOL’s cash flow from operations (or CFO) in 1H 2023 deteriorated significantly compared to a year ago, associated with the PBH buy-in agreement. So, a year ago, free cash flow (or FCF) turned negative from a positive FCF. It also plans to increase its capex budget for FY2023 by 45% compared to FY2022.

Target Price And Relative Valuation

Seeking Alpha

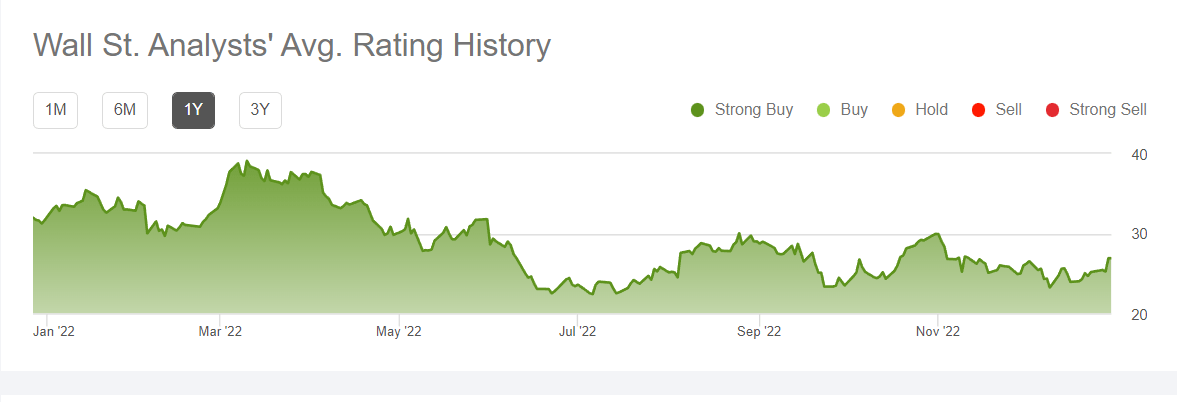

Over the past three months, two sell-side analysts rated VTOL a “buy” (including a “Strong buy”), while none recommended a “Sell” or a “Hold.” The stock’s return potential using the sell-side analysts’ expected returns is 47% at the current price.

Seeking Alpha

VTOL’s forward EV-to-EBITDA multiple will contract more steeply versus the current EV/EBITDA than its peers, which implies its EBITDA will increase more sharply than its peers. This should typically result in a higher EV/EBITDA multiple than the peers. The company’s EV/EBITDA multiple (11.2x) is lower than its peers’ (NESR, HLX, and FTI) average of 17.7x. So, the stock is undervalued at this level.

What’s The Take On VTOL?

Seeking Alpha

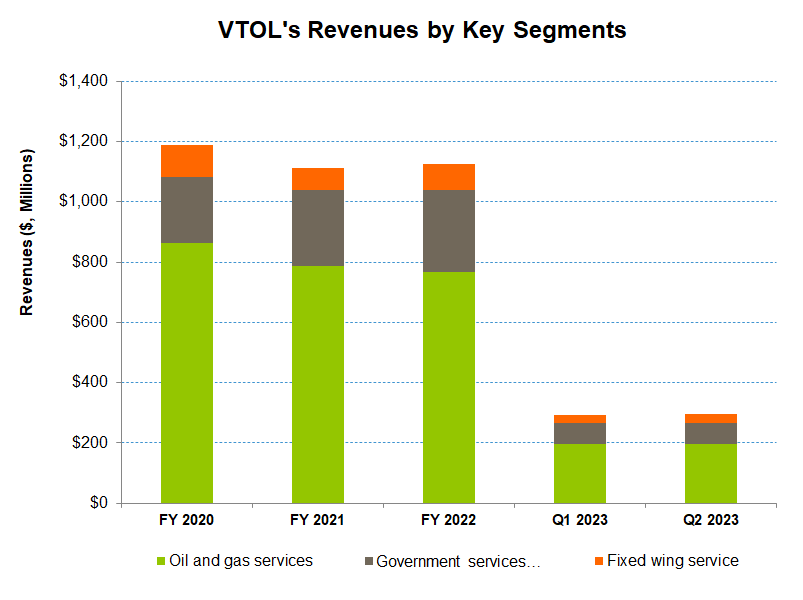

The energy business is poised to improve in 2023, particularly in the US Gulf of Mexico, Nigeria, and Brazil. Oil and gas services still drive a significant part of VTOL’s revenues (67% in Q2), but non-energy (i.e., Government and fixed-wing services) have become an important driver (33% of its sales). However, the primary headwind for VTOL is the US dollar’s appreciation against the British pound in the recent past.

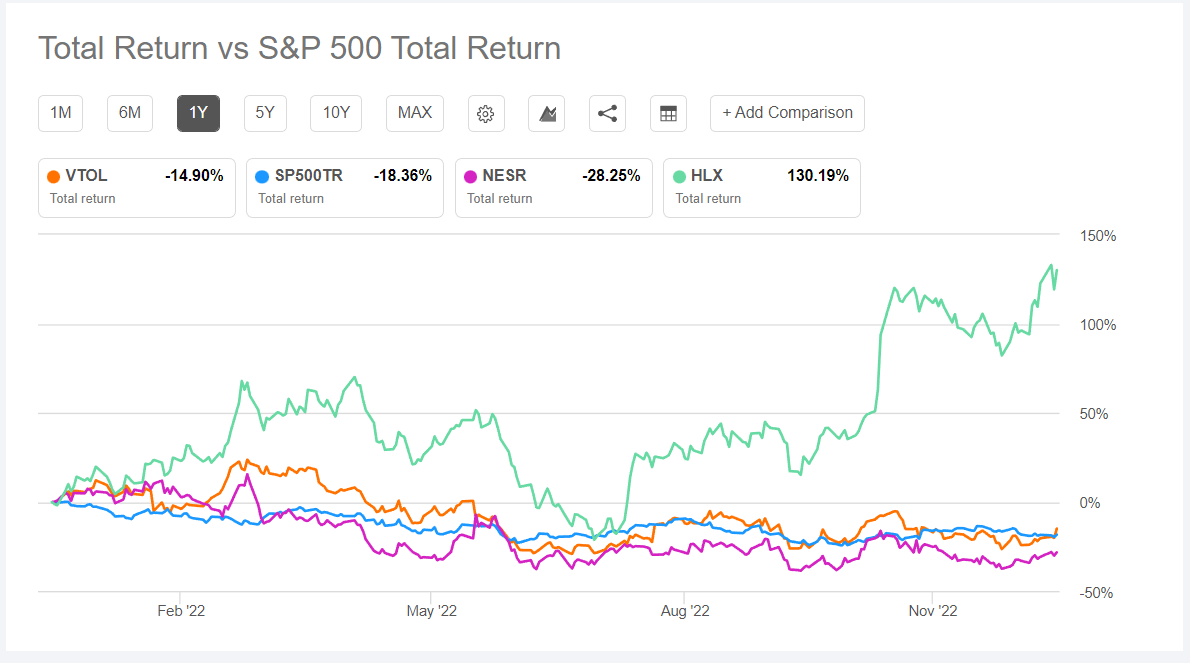

Plus, cash flows weakened severely in 1H 2022. So, despite the positive outlook, the stock marginally outperformed the SPDR S&P 500 Trust ETF (SPY) in the past year. Also, its leverage ratio is higher than its peers. Nonetheless, given the robust liquidity and low relative valuation, I think the stock has a positive bias at the current price.

Be the first to comment