Dragoljub Bankovic

Continuous Glucose Monitoring (CGM) system maker DexCom (NASDAQ:DXCM) is trading at a lofty P/E of 141. Some may view this as fair with the company poised to reap considerable revenue and profit gains over the coming years, others however may see it as pricey.

Brief overview

DexCom was the first mover in the CGM space and its products are considered to be the gold standard. DexCom competes with Abbott’s Freestyle Libre (ABT), and Medtronic Guardian Connect (MDT) among other smaller players in the CGM space. For the year ended December 2021, DexCom generated USD 2.45 billion in revenues in 2021, up 27% YoY. Gross profits were USD 1.68 billion while net profits were USD 154 million.

Plenty of room for further penetration in DexCom’s home market – the U.S.

Of the more than 30 million diabetes patients in the U.S., and the vast majority (about 90% – 95%) live with Type 2 diabetes. Yet just about a third of Type 2 diabetes patients use CGM devices to monitor blood glucose levels (diabetes patients have traditionally monitored glucose levels using the ‘finger prick’ method, a relatively more painful, and cumbersome process) leaving a potential market of around 20 million patients in the U.S. alone, an enormous growth opportunity for DexCom who has about a million customers worldwide (market leader Abbott has about 3.5 million). With current revenue per patient in the U.S. of a few thousand dollars annually, (DexCom device and consumables prices vary but rough estimates suggest a gross total of approximately USD 6,000 per year and after deducting distributor margins DexCom likely receives a few thousands of dollars per patient per year), the revenue potential in the U.S. alone equates to several billion dollars (assuming DexCom’s current U.S. market share of around 20%), a significant growth opportunity for DexCom, which generated revenue of USD 2.5 billion in 2021.

Growth opportunity from international expansion

The vast majority of DexCom’s revenues are generated in the U.S. (international revenues accounted for about 24% of revenues in 2021). DexCom is exploring expansion opportunities in high-and-middle income markets in Asia (including Japan and Korea), and Europe. Offices have been opened in Canada, Europe (Austria, Germany, Switzerland, Lithuania, and the United Kingdom. Except for Japan (which has a diabetes population of around 11 million), these markets individually are not as sizable as the U.S., but collectively they are significant amounting to 15 million. These countries have high incomes and mature public health insurance systems making them suitable geographies for DexCom to target and possibly generate average revenue per patient that is roughly comparable to the U.S. Together with Japan, these countries alone represent a market of around 26 million diabetics, slightly bigger than the untapped market for CGM in the U.S.

|

Country |

|

|

Japan |

11 million |

|

Korea |

2.2 million |

|

United Kingdom |

4.2 million |

|

Germany |

5.7 million |

|

Canada |

2.9 million |

Low-priced option – DexCom ONE – positions DexCom to capture lower-priced segment

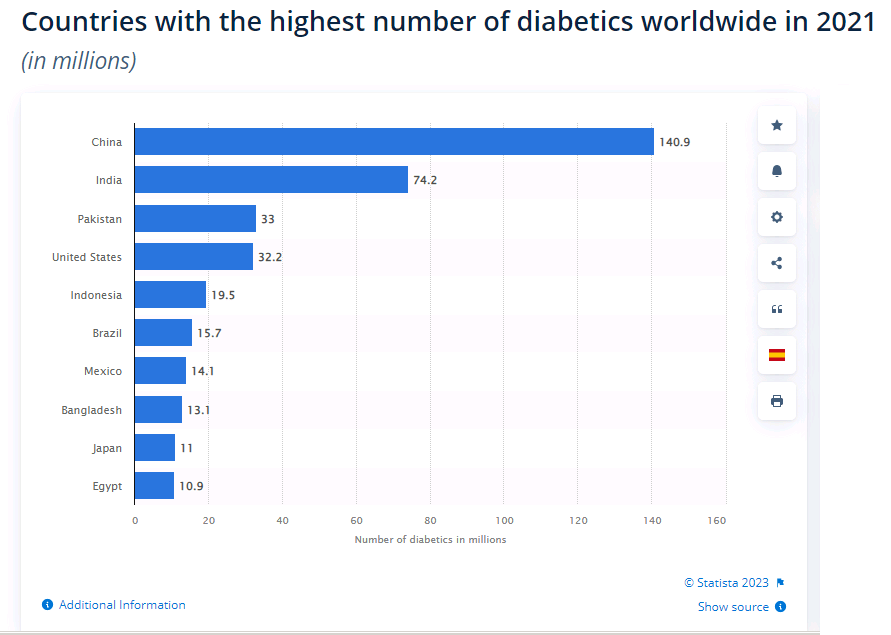

Rival Abbott has largely focused on the low-cost CGM market with its Freestyle Libre devices while DexCom has traditionally focused on the higher-cost but more accurate segment. Their high-cost products however limited DexCom to developed markets, notably the U.S., and Europe that could afford DexCom’s products. The biggest growth opportunities however lie elsewhere, notably in China, India Pakistan and Indonesia (who along with the U.S. make up the top five countries with the world’s largest diabetes populations), but whose incomes are a fraction of the U.S.

Statista

China, India, Pakistan, and Indonesia are also expected to see a nearly 50% increase in their diabetes populations over the next two decades, adding about 123 million people to their diabetes populations by 2045.

International Diabetes Federation

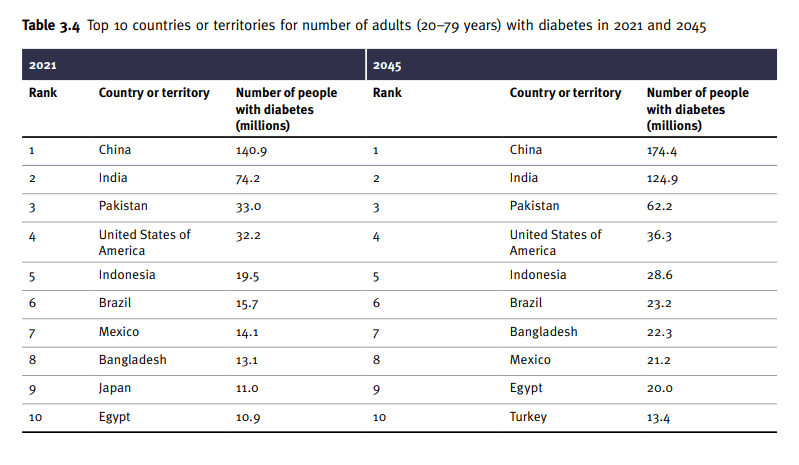

To address this gap in its product offering, DexCom rolled out a cheaper but pared down version of its G6 device – DexCom ONE. The product was launched only last year and allows the company to capture a greater share of the diabetes population outside the U.S. The revenue potential is significant; although these regions are likely to generate a far lower average revenue per patient compared to the U.S. (DexCom ONE retails for about half of DexCom’s G6), this is outweighed by the sheer size of the market (China, India, Pakistan, and Indonesia alone have a diabetes population of around 266 million). Assuming a market share of a conservative 5% with an average revenue per patient of around USD 800, the potential revenue amounts to around USD 10 billion. This is not even including the other markets within the top 10 and below who collectively make up a sizeable market; there are approximately 537 million diabetes patients worldwide and this number is projected to rise to 643 million by 2030 according to the International Diabetes Federation.

G7, Malaysia manufacturing facility, scale economies to help reduce manufacturing costs

DexCom’s latest CGM model – the G7 – which launched in Europe in October last year, is expected to launch in the U.S. and “worldwide” this year. DexCom’s G7 is considerably cheaper to manufacture than its predecessor – the G6 – a positive for gross margins as G7 sales increase while G6 is gradually phased out.

DexCom is currently building their third manufacturing plant in Malaysia (the first facility outside the U.S.). The facility should help reduce manufacturing costs and support DexCom’s international expansion ambitions; labor costs in Malaysia are extremely competitive and the facility, located in Penang (known as the Silicon Valley of the east) offers a mature supply chain of electronic component manufacturers (such as sensors and semiconductors). Construction is on track and production is expected to begin in mid-2023.

Moreover, as DexCom scales their international operations, the company should benefit from scale economies as well, overall helping to expand margins which are currently around 68% and 6% for gross margins and net margins, respectively.

Risks

Possible near term margin pressure due to rising competition

DexCom’s main competitors in the CGM market are Abbott, Medtronic, and Senseonics. New players include British newcomer GlucoRX With competition increasing in the CGM market, notably against archrival Abbott, DexCom has been ramping up promotional activity in an effort to gain market share. DexCom’s advertising expenses jumped 65% YoY to USD 126.4 million in 2021 (a far higher increase than revenues which rose 27% YoY.

Sugar taxes, growing health awareness can limit increasing diabetes incidence

Although projections forecast diabetes incidence to increase tremendously, rising health awareness as well government efforts to control ballooning healthcare costs (such as by curtailing diabetes incidence through sugar taxes) could potentially limit diabetes incidence increase in the years ahead.

Conclusion

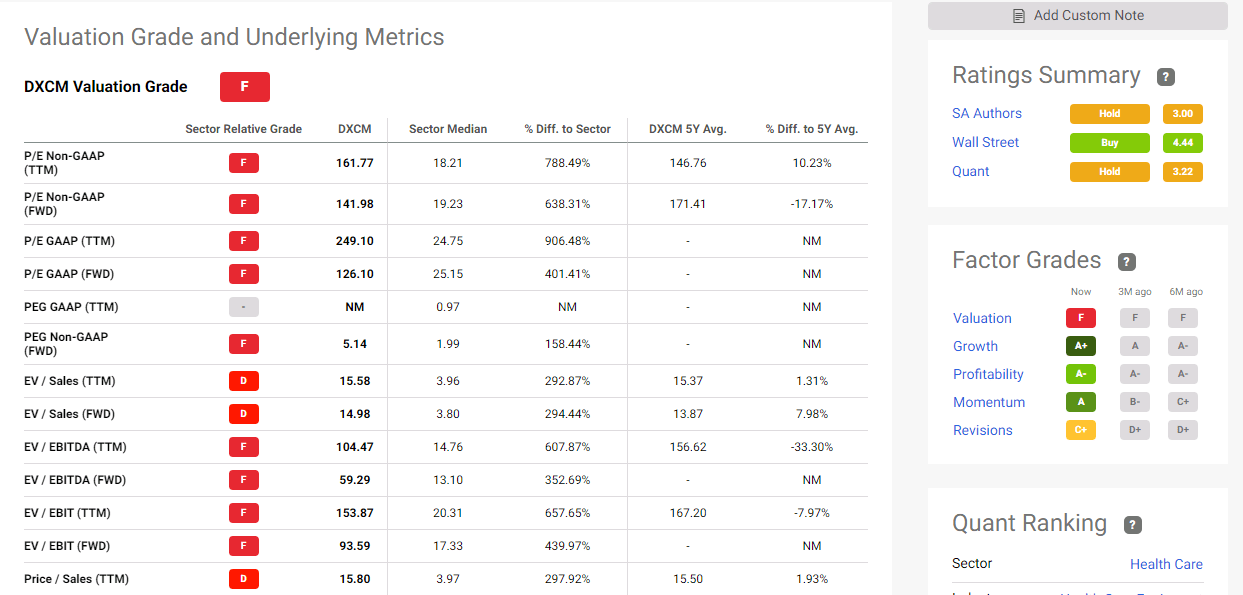

With DexCom positioned to enjoy multi-fold revenue and profit growth prospects in a growth industry with relatively high barriers to entry, their P/E of 141 may be viewed as fair to some although others may view it as rather pricey and may prefer to wait for a better entry point; for perspective medical device market leaders such as surgical robot maker Intuitive Surgical (ISRG) trades at a P/E of 56 (Intuitive Surgical is far away the market leader in its industry unlike DexCom who is battling stiff competition from medical device giant Abbott along with other smaller players). Seeking Alpha gives DexCom’s valuation an ‘F’, and DexCom’s price multiples are considerably higher than sector medians.

Seeking Alpha

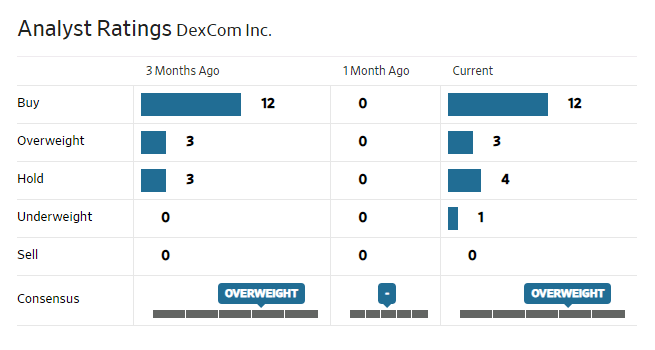

Analysts are generally bullish on the stock.

WSJ

Be the first to comment