Guido Mieth

WideOpenWest (NYSE:WOW) noted in a recent quarterly report that the company continues to experience strong demand for its HSD services. In my view, if new clients also purchase WOW’s video and telephony services, revenue growth will likely trend north. I also see risks from the total amount of debt and competition from large operators, however, in my view, the stock appears undervalued.

Business Model

WideOpenWest is a provider of broadband services. It offers high-speed data transfer services, cable television, and telephone services to households and retail consumers as well as different types of broadband solutions for companies and shops.

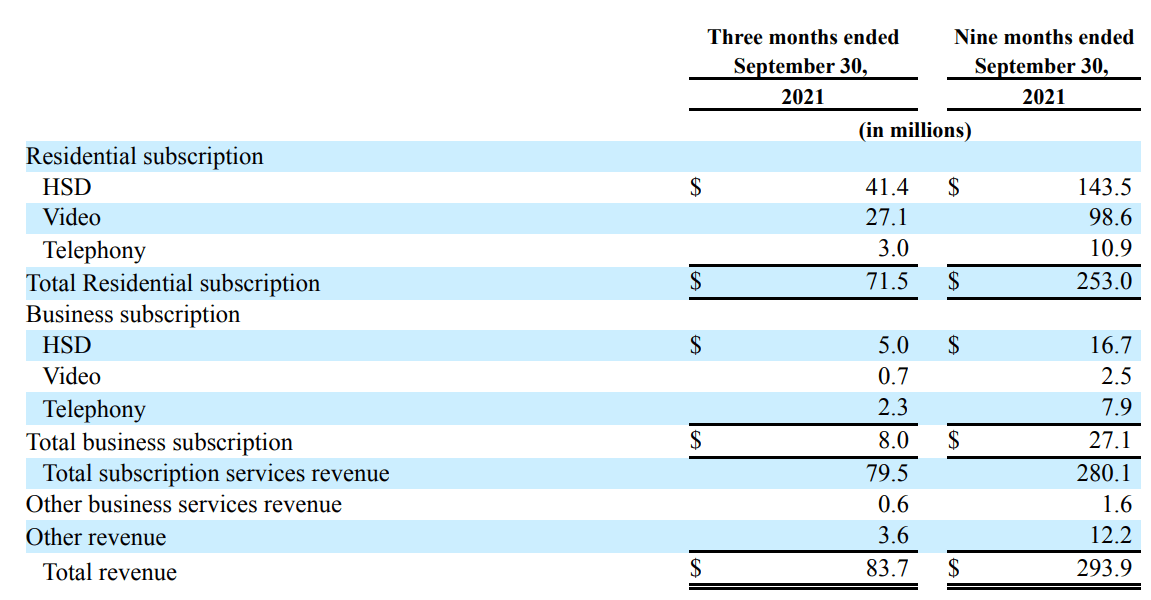

Source: 10-Q

Its services currently extend to 14 regional markets in the United States, mainly in Alabama, Florida, and Minnesota, with the city of Detroit being the largest hub of operations to date. By the year 2022, WideOpenWest registered 1.9 million homes and businesses connected to its service lines, as well as 532,900 contracting companies and customers.

The core of its business and operations, according to the company, is to be able to provide high-quality, low-cost services, making this type of facility accessible to all types of consumers. 96% of its networks are operating at 750 MHz to date, as a result of its permanent research and investment strategies in improving its networks over other types of searches such as commercial strategies or the sales area.

Estimates From Financial Analysts Appear Quite Beneficial

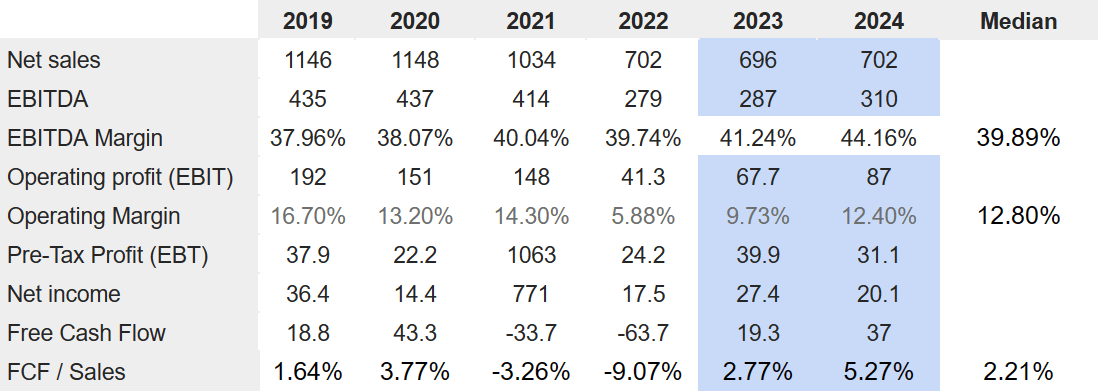

I believe that financial analysts delivered beneficial expectations about WOW. 2024 net sales are expected to be close to $702 million, a bit more than the figure expected for 2023. In addition to 2024 EBITDA of $310 million and 2024 EBITDA margin of 44.16%, 2024 operating profit is expected to be $87 million. It is worth noting that the EBITDA margin is expected to increase. 2024 pre tax profit would stand at $31.1 million, with a net income of $20.1 million. Finally, 2024 FCF would be close to $37 million with FCF/sales of 5.27%.

Source: S&P

Balance Sheet

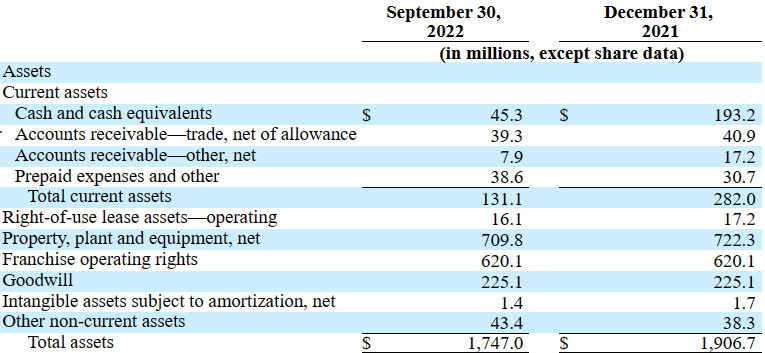

As of September 30, 2022, the company reported cash of $45.3 million, accounts receivable of $39.3 million, and prepaid expenses close to $38.6 million. Total current assets stand at $131.1 million, below the current amount of liabilities. In my view, a few very conservative investors may not appreciate the total amount of liquidity reported by WOW.

Property stands at $709.8 million together with franchise operating rights of $620.1 million, goodwill of $225.1 million, and other non-current assets of $43.4 million. Total assets stand at $1.747 billion, and the asset/liability ratio is equal to 1x-2x. Even considering the total amount of current assets, in my view, the balance sheet appears in good shape.

Source: 10-Q

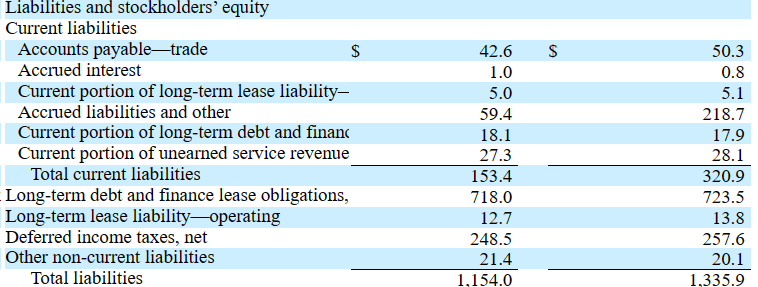

WOW’s liabilities include accounts payable worth $42.6 million along with accrued liabilities of $59.4 million. The current portion of long term debt stood at $18.1 million, in addition to the current portion of unearned service of $27.3 million. Finally, total current liabilities were $153.4 million.

The long term debt does not seem small. It is equal to $718 million with a long term lease liability of around $12.7 million. Deferred income taxes stand at $248.5 million, accompanied by other non-current liabilities of $21.4 million. Finally, total liabilities are equal to $1.154 billion.

Source: 10-Q

More Assessment Of Consumer Behaviour And Better Pricing Strategies Could Bring Significantly More Demand.

Considering the total number of clients reported in the last annual report, who contracted HSD services, I believe that the opportunity is large. If these clients decide to subscribe to higher speed tiers, and receive more programming content, revenue growth will likely increase. I believe that readers need to have a look at the company’s optimism noted in the last annual report and the last quarterly report.

Approximately 64% of our customer base subscribed only to our HSD service. We expect the portion of our customer base that subscribes only to our HSD service to continue to rise as broadband utilization increases across every facet of our customer’s lives.

In addition, we fully anticipate new and existing customers to continue to purchase higher speed tiers to support the evolution of how customers consume entertainment content. Source: Annual Report

We continue to experience strong demand for our HSD service. Source: 10-Q

I also believe that WOW will likely learn more and more about the clients, so pricing strategies and HSD offerings will likely evolve and help design new services. Under this scenario, I assumed that new products and pricing will likely bring demand.

We employ value based pricing strategies for our subscription HSD, Video and Telephony services. We focus our pricing strategy around our HSD offering and provide the option for HSD customers to purchase Video and Telephony services as part of a bundled service with tiered features and pricing. We believe that our services are priced and featured to meet the demands of a variety of consumers. Source: Annual Report

Experts in market assessment believe that the cable television broadcasting services market will likely grow at a CAGR of close to 5.4%. Hence, under normal conditions, I believe that WOW’s net revenue will likely grow at the same pace.

Cable Television Broadcasting Services is expected to grow at a CAGR of over 5.4% during 2022 – 2032. Source: Television Broadcasting Services Market

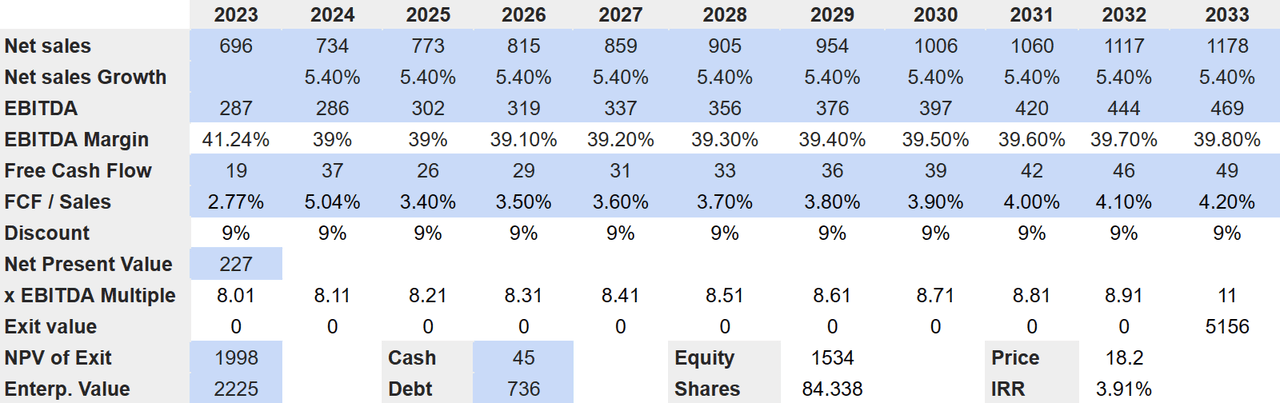

With sales growth of 5.4%, an EBITDA margin of 39%, and FCF/Sales close to 4%, I obtained 2033 net sales of $1.1 billion and 2033 FCF of $49 million. If we use a discount of 9% and an EV/EBITDA close to 11x, the net present multiple of the exit value would be $1.9 billion, and the NPV of future FCF would stand at $227 million. Now, the sum of the terminal value and the discounted FCF results in an enterprise value of $2.2 billion. I also obtained an equity valuation of $1.53 billion, an implied price of $18.2 per share, and an internal rate of return of 3.91%.

Source: Malak’s Financial Model

Competitors, More Regulations, And Debt Risks Could Imply A Valuation Of $8.95 Per Share

WideOpenWest operates in a highly competitive market that is subject to change and technological innovation. The inability to respond to these dynamics can mean a risk for the company.

The competitors of this company vary according to its different services as there are different smaller providers. In this regard, each region in which WideOpenWest operates has local competition for both residential and business services. The risk in this sense involves attracting customers at a low cost. Nationally, the company competes with the largest broadband service providers in the United States, which prevents easy growth outside the states where it is already positioned. Let’s keep in mind that some of the competitors are massive corporations with more resources and significantly more market recognition than WOW.

Source: Annual Report

Besides, WOW obtains customers by charging low costs to its consumers, which could be endangered in the event of increased costs in programming and retransmission of content. There are also risks from WOW’s competitors’ exclusivity programs, such as HBO or Amazon (AMZN). If WOW can’t offer quality programming and content, competitors will likely gain market share from the company.

Moreover, WideOpenWest operates several of its networks through franchisees whose commercial contracts may expire. The inability to maintain or renew these contracts may jeopardize the company’s operations, and reduce future sales growth expectations. In line with these words, networks and facilities, future regulations, and laws that imply compliance with the reduction in carbon emissions and reduction of environmental damage could force WideOpenWest to a forced adaptation that would diminish future FCF margins.

I also believe that the total amount of long term debt could represent a risk for WOW. An eventual strong increase in the interest rates may increase the company’s interest expense payments. As a result, the company’s cost of equity may increase, which would lower the company’s valuation. If equity investors dislike the total amount of leverage, WOW may receive less demand for the stock, which may increase the cost of equity. In sum, WOW’s stock price could diminish.

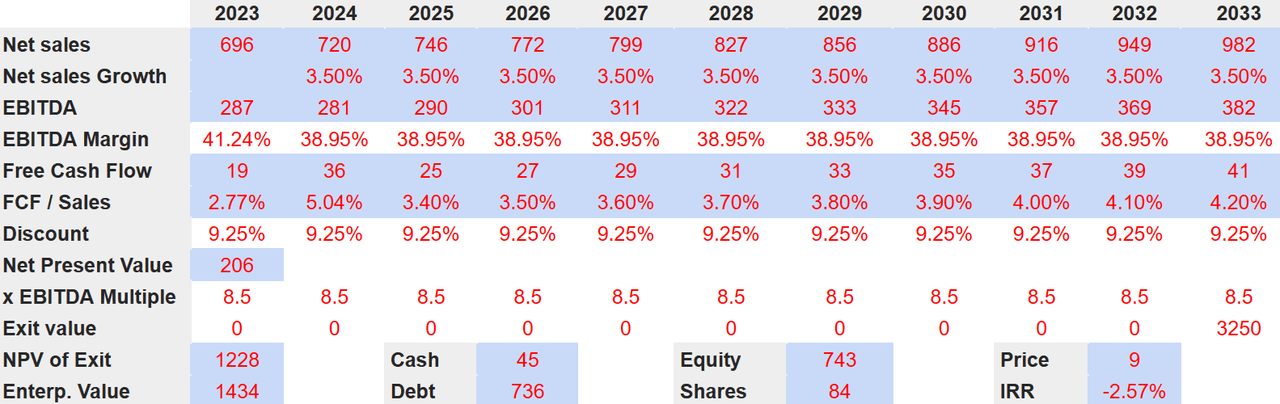

If we use net sales growth of 3.5%, an EBITDA Margin of 38.95%, and FCF/Sales of 9.25%, 2033 FCF would be $41 million, and 2033 net sales would stand at $982 million. Now, with a WACC of 9.25%, the net present value would stand at $205.5 million. Besides, with an EV/EBITDA multiple of 8.5x, the net present value of the exit term would be $1.22 billion. Finally, if we take into account cash of $45 million and debt close to $735.5 million, the implied price would be close to $8.95 per share, and the IRR would stand at -2.5%.

Source: Malak’s Financial Model

Conclusion

WideOpenWest recently noted that it continues to experience strong demand for its HSD services. In my opinion, if customers subscribing to HSD also purchase video and telephony, future sales growth will likely trend north. I also believe that further assessment of data from clients will likely lead to better pricing strategies, which may also bring more FCF margins. I see risks from the total amount of debt and competition, however, I believe that the company’s stock price could be worth much more.

Be the first to comment