Introduction

Windstream (OTCPK:WINMQ) is a key tenant for Uniti Group, Inc. (NASDAQ:UNIT) and makes up about half of Uniti’s revenue base. Its abrupt bankruptcy has sent shivers down the spines of every Uniti bull. While we have played the Uniti game from every angle in the past (long, short, ratio call spreads, ratio put spreads, long unsecured bonds), we think the time for those games is done. Today you either go short or go home. The latest development reinforced our thought process on this.

Windstream files new paperwork

Windstream filed some additional documents related to its ongoing bankruptcy proceedings and negotiations with Uniti. While there are several interesting angles from the point of view of the different tiers of Windstream bondholders, we were most interested in the financial projections of the new Windstream. Now some of the projections will of course change depending on what is the final outcome of the bankruptcy, but there is a lot to be gleaned even keeping that in mind.

The customer on constant life support

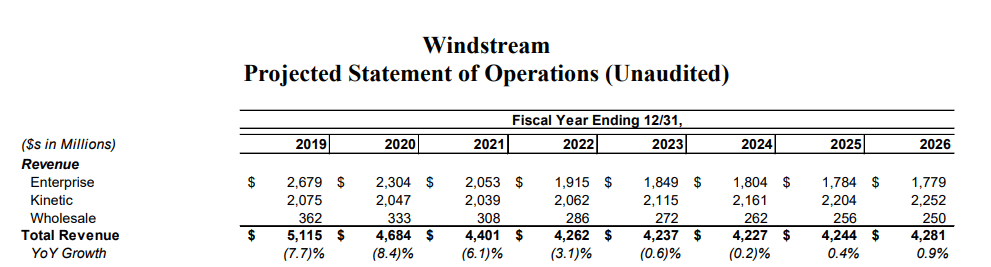

Windstream’s problems stemmed from a constant revenue decline. That led to a perpetually falling OIBDAR (Operating Income Before Depreciation Amortization & Rent). What is interesting though is Windstream’s projections over the next seven years.

{kind=link}

Source: Windstream

Revenue declines don’t stop till 2025, and even there, the growth is made out to be a rounding error. Fascinatingly OIBDAR starts picking up steam in 2023 and grows rather strongly year after year from there.

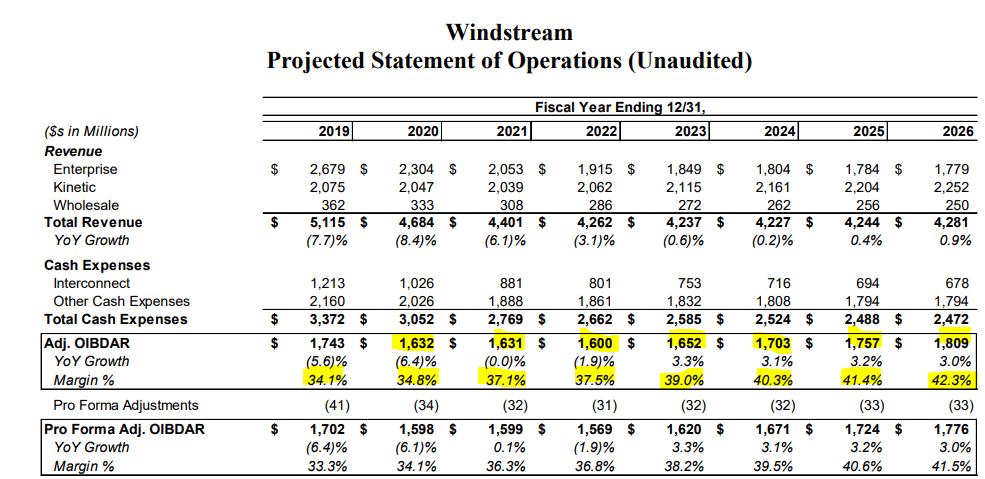

Source: Windstream

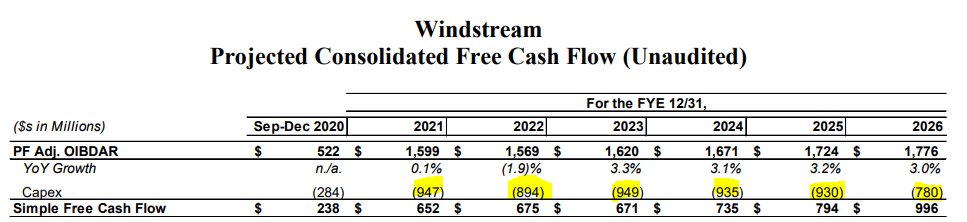

Windstream has made this possible through rather generous OIBDAR margins which expand from 34.1% to 42.3%. Considering the markets it is in alongside the competition, we don’t think this will be remotely feasible. Even with those extra rosy projections, Windstream’s free cash flow situation is extremely tenuous. To start off, even in 2021, Windstream’s OIBDAR minus Capex is less than what it paid to Uniti in 2020 for rent (approximately $650 million).

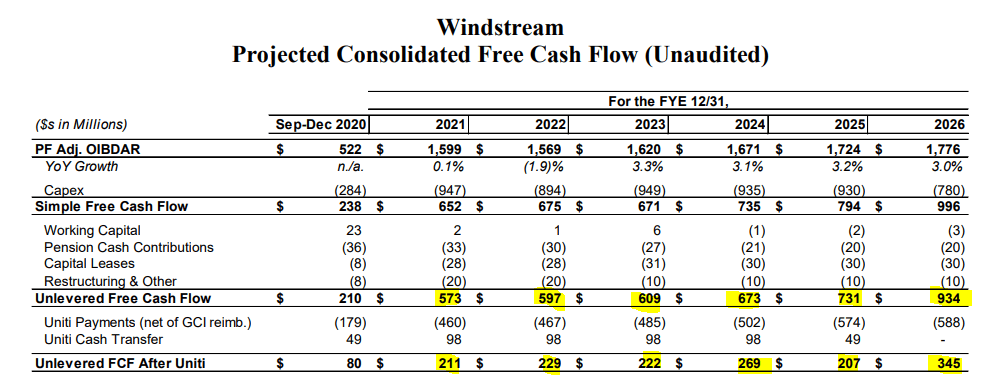

Source: Windstream

This should empirically settle whether or not Uniti had to come to the table (it did, in case it was not clear). Thanks to falling OIBDAR and high capex, Uniti’s original run rate of rent would only be covered (as defined as unlevered cash flow above) after 2025. Fortunately Windstream will get some generous life support from Uniti, but that will only take it so far.

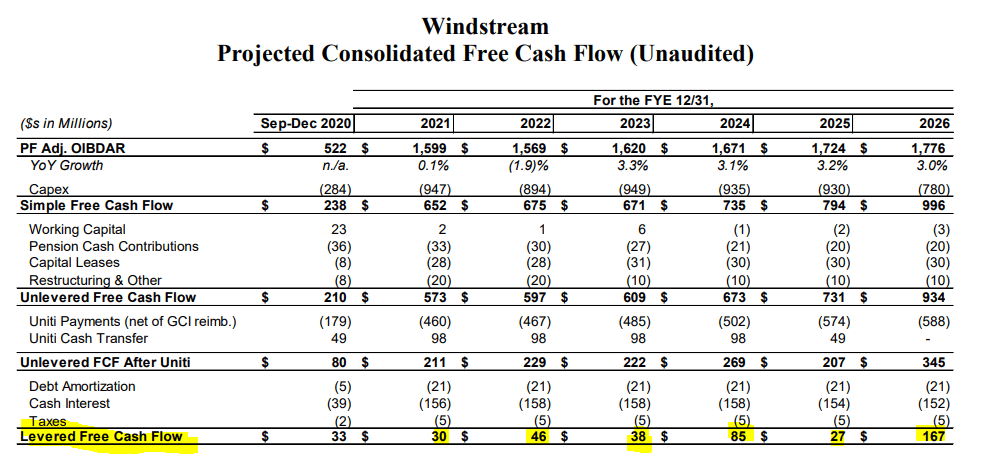

Levered Cash flow

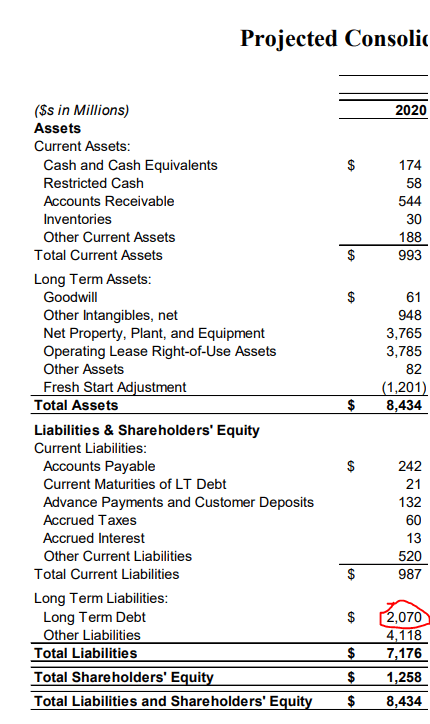

Windstream’s proposed post bankruptcy balance sheet is the hardest set of figures to rely on at this point. But even giving it a wide margin of error, we can derive some useful facts.

Source: Windstream

New Windstream will be carrying substantial liabilities. The $4.118 million refers to the operating lease liabilities, which do not matter in a real sense. But Windstream will still have $2.07 billion of long-term debt. Windstream’s real free cash flow will again be a ridiculously tiny $30 million in 2021.

Source: Windstream

This is after expected Uniti concessions of dropping the rent down by close to $200 million. This is after expected Uniti cash transfer of $98 million a year. The real culprit is the capex which will be close to $900 million annually.

Source: Windstream

Windstream’s rationale for the capex is explained in the document:

Total capital expenditures are forecast to increase from ~$879 million in 2019 to ~$947 million in 2021, though declines to ~$780 million by the end of the projection period. The primary reason for the increase in capital expenditures during the projection period is to significantly expand network speed (e.g., 1GB expansion program) through increased investments in fiber to the premises (“FTTP”) and fixed wireless infrastructure. – Source: Windstream

When that level of capex struggles to keep your revenues flat, you cannot with a straight face call it “growth capex”. That is maintenance capex, plain and clear and anyone who believes otherwise is flat out wrong.

Sensitivity analysis

Windstream’s free cash flow disappears in any case where:

1) Revenues are 2%-3% lower

2) Expenses are 3%-4% higher

Even at the end of the period shown, Windstream will have substantial debt in relation to free cash flow ($1.98 billion at the end of 2026). Our point here is that Windstream will still come out looking like it is about to file for bankruptcy rather than it came out of one. Any slippage will create dire straits again for the company and hence for Uniti.

Conclusion

Windstream’s OIBDAR has declined by 6% a year like clockwork year after year. We would note that that happened during the longest running expansion in US history. With unemployment increasing by 20% and GDP declining by over 25% in Q2-2020, Windstream is projecting flat OIBDAR for the next seven quarters. Two quotes come to mind.

We think Uniti is very badly hobbled and stuck between a rock and another rock with sharp edges. Already 2021 numbers with these rent reductions will make Uniti’s debt look rather unsustainable. If (actually “when” is better) further rent cuts are required, Uniti’s cash flow will become even more strained. We reiterate our call that Uniti will not pay a cent more in dividends than REIT rules require and it may even pay that in shares versus cash.

If you enjoyed this article, please scroll up and click on the “Follow” button next to my name to not miss my future articles. If you did not like this article, please read it again, change your mind and then click on the “Follow” button next to my name to not miss my future articles.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

TipRanks: SELL

High Dividend Opportunities, #1 On Seeking Alpha

HDO is the largest and most exciting community of income investors and retirees with 4,400 members. We are looking for more members to join our lively group and get 20% off their first year! Our Immediate Income Method generates strong returns, regardless of market volatility, making retirement investing less stressful, simple and straightforward.

Invest with the Best! Join us to get instant-access to our model portfolio targeting 9-10% yield, our preferred stock and Bond portfolio, and income tracking tools. Don’t miss out on the Power of Dividends! Start your free two-week trial today!

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a short position in UNIT over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment