Laser1987

Wells Fargo (NYSE:WFC) reported its Q4 earnings on Friday. The numbers were fairly underwhelming, at least at first glance, and shares sold off by as much as 4% in early trading Friday morning.

This wasn’t completely unexpected. After all, the company was hit with a $3.7 billion fine in December as part of the legal remediation process for the company’s fraudulent accounts scandal. Wells Fargo quarterly earnings reports continue to be a complicated affair as the company deals with both its past legal headaches and a complex economic environment going forward.

That said, Wells Fargo shares rallied sharply through the course of the day Friday, turning a meaningful premarket loss into a solidly positive performance. Let’s dig into the earnings report to see the factors at play here.

Breaking Down Wells Fargo’s Q4 Earnings

From the top-line numbers, Wells Fargo appeared to have a mixed quarter. Q4 earnings per share of 67 cents topped expectations by six cents. However, revenues of $19.7 billion missed by $380 million and amounted to a 5.7% year-over-year decline in revenues. That’s not a great look.

And while earnings did beat estimates, the Q4 EPS figure fell sharply year-over-year. The company earned $1.38 per share in Q4 of 2021. For Q4 this year, that plunged to just $0.67. At first glance, that might sound really bad.

However, with bank quarterly results, it’s important to focus on a bank’s core earnings power. Particularly for the large national banks, earnings are exceptionally complex with a ton of moving parts. An analyst should assess a company’s ongoing earnings potential rather than focus on the one-time items which cause volatility in earnings in any given quarter.

For this most recent quarter, for example, Wells Fargo took a 70 cent per share hit from items related to litigation, regulatory matters, and customer remediation. If you back that out, the company’s Q4 earnings per share would have been $1.37, which is essentially flat vs. last year’s $1.38 result.

That’s not all. Wells Fargo also took a 15 cent per share hit from recognizing losses in its affiliated venture capital business. That’s not a surprising result, given the drastic declines we’ve seen in valuations for many growth companies over the past year. We can say Wells Fargo made mistakes in capital allocation there, perhaps. However, I’d argue this sort of loss is a cost of doing business in investment banking, and Wells Fargo’s gains during bull markets more than offset modest write-downs during periods such as now.

If you put aside legal costs and venture capital losses, Wells Fargo’s earnings would have been up year-over-year. Is that an accurate way of thinking about things? The losses suffered there were real, and hurt shareholders, no doubt. However, I’d argue that the actual banking business – the process of gathering deposits, making loans, and earning the profit spread therein – is looking more attractive than ever.

To that point, Wells Fargo’s net interest margin is continuing to soar. The net interest margin hit 3.14% this quarter, up from 2.83% in Q3 of ’22. In Q4 of last year, Wells Fargo’s net interest margin was a meager 2.11%. In just one year, Wells Fargo has improved its lending profitability by more than 100 basis points. This is simply incredible stuff. I fear investors are lost in the noise around legal expenses or whatnot and miss the fact that the bank’s core lending business has become essentially 50% more profitable over the past year thanks to the surge in interest rates.

What About Economic Risk?

The other drag on earnings, which largely offset the rise in net interest income, was a significant increase in provisions for future credit losses. This is where banks set aside reserves today to cover loans which may go bad in the future. As the economy weakens, banks build more reserves for anticipated future losses. If and when the economy recovers, banks can reduce their provisions and see an increase to earnings.

At the moment, however, banks are hunkering down for worsening credit conditions. That’s a perfectly reasonable behavior given the current economic outlook. In fact, Wells Fargo was far from alone in adding to its provisions (and thus weakening its quarterly earnings) among the major banks in Q4.

Is this rise in credit provisions a harbinger of a rough 2023 ahead? Not necessarily. Here’s CEO Charlie Scharf on what the bank is seeing with its customer base:

“Our customers have remained resilient with deposit balances, consumer spending, and credit quality still stronger than pre-pandemic levels. As we look forward, we are carefully watching the impact of higher rates on our customers and expect to see deposit balances and credit quality continue to return toward pre-pandemic levels.”

Returning to how things were prior to the pandemic would hardly be a bad thing for banks. The banks had excellent credit quality in the late 2010s. The issue, as far as earnings went, was that interest rates and spreads were simply too low to earn that much money even though loan quality was high. However, now, loans are offering much more attractive starting yields. Wells Fargo’s net interest margin is up more than one full percentage point, after all.

The key profitability issue has improved, and having more or less normal levels of credit quality would be sufficient for the American banking sector to generate record profits going forward.

There’s a difference between provisions for credit losses and actual credit losses. Banks set aside capital for potential losses whenever economic conditions appear to be worsening. This is a prudent measure that helps stabilize a bank’s operations.

However, oftentimes, these provisions don’t actually turn into real credit write-offs of the same magnitude. Look at 2020, for example, when banks built up huge provisions to deal with expected outsized losses from the economy being shut down. Instead, the government offered strong measures to counteract the direct hit of the pandemic-related business closures, and loans ended up performing far more strongly than banks had feared might happen.

It remains to be seen if the Federal Reserve will manage something along the lines of a “soft landing” or if we’re headed for a more serious and prolonged recession. I could make a good argument for either potential outcome at this point. What I will say is that I’m not necessarily assuming all the credit provisions we see today are sure to turn into real write-offs over the next 12-24 months. Regardless, banks – including Wells Fargo – take an incremental hit to earnings today to make those provisions in case the next recession ends up being a doozy.

Sector Results: Similar Market Reaction

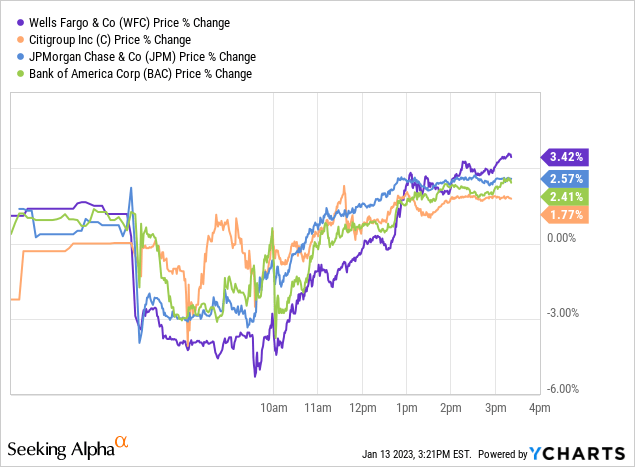

An investor focused on just one of the individual big banks might try to derive a lot of meaning out of the initial sell-off and subsequent rebound in, say, WFC stock.

However, it’s worth considering that four major banks reported Friday morning. In addition to Wells Fargo, JPMorgan Chase (JPM), Bank of America (BAC), and Citigroup (C) all reported at the same time.

And, through early Friday afternoon trading, all had roughly the same pattern, with shares dropping around 3% pre-market before rallying and moving to strongly positive territory.

Oddly enough, Wells Fargo started the day with the biggest drop of the four banks in question, and appears set to end up with the biggest advance for the day when the session ends:

I’d stress that investors not make too much out of any one earnings report. You can pick out individual items, such as JPMorgan Chase warning investors of significantly higher operating expenses in 2023 versus expectations.

However, at the end of the day, the market is clearly trading this group of stocks as a sector and looking at the overall metrics. How strong is loan demand? How much of the Fed’s interest rate hikes are filtering into net interest margins? How are credit metrics looking? These questions, much more than a singular quarterly EPS number, are what will drive these stocks’ performances over the next year.

WFC Stock Bottom Line

I tend to take bank earnings, either good or bad, with a grain of salt. The presence of so many accounting items, such as allowances for potential credit losses, make quarterly earnings per share an imprecise measure of a bank’s ongoing earnings power.

I personally tend to focus more on longer-term metrics such as changes in a bank’s net interest margin, operating efficiency, and credit quality. On these metrics, Wells Fargo (and most other large American banks) are currently pointed in the right direction.

There’s no doubt that this was a messy quarterly earnings report for Wells Fargo. However, as the trading reaction on Friday seemingly showed, the core fundamentals for Wells Fargo – along with its peer national banks – remain strong. Net interest margins are way up, the consumer remains reasonably healthy, and the economic outlook is fair for the banks in particular.

Could things worsen? Yes, of course. If the Fed can’t manage a successful soft landing, Wells Fargo’s outlook could dim significantly. However, I’d argue that this possibility is already baked in price. Wells Fargo’s operating results have improved, and yet shares are down approximately 20% over the past year. The divergence creates an opportunity for the bulls.

Be the first to comment