clu/E+ via Getty Images

Introduction

It’s time to talk about Sealed Air (NYSE:SEE). This company is flying under the radar as Sealed Air is a supplier of packaging materials and technologies in the packaging and container industry, which isn’t a very hot industry for most investors. With a market cap of $8.3 billion, the company has become a leading supplier of advanced materials used to lower costs, improve environmental standards, and automate various packaging supply chains. It’s a company that not only benefits from cyclical e-commerce and food consumption growth but also from secular growth like the need for automation and waste reduction. The just-released quarterly earnings confirm the company’s strength and I agree with new sell-side recommendations: Sealed Air is too cheap and poised to outperform.

In this article, I will tell you why that is.

Packaging As A Secular Tailwind

What is secular?

To quote Investopedia:

In finance, secular is a descriptive word used to refer to market activities that occur over the long term. Secular can also point to specific stocks or stock sectors unaffected by short-term trends. Secular trends are not seasonal or cyclical. Instead, they remain consistent over time.

Sealed Air is dependent on economic cycles as well as secular growth.

First of all, the company has two business segments.

In its Protective segment, the company generated 43% of total sales in 2Q22. This segment provides packaging products for e-commerce, consumer goods, pharmaceuticals, medical devices, and industrial manufacturing.

This segment includes brands like Sealed Air, Bubble Wrap, and AutoBag.

Needless to say, while e-commerce and high-quality, environmentally-friendly packaging products are in a secular uptrend, there is a large cyclical factor here as consumer and industrial packaging depends on spending and investments.

The other segment is Food. This segment benefits from at least two major secular trends. The quote below is from the abstract of a scientific paper written last year titled “Meat Production and Supply Chain Under COVID-19 Scenario: Current Trends and Future Prospects”.

This paper covered COVID-19-related issues in meat processing.

In early April 2020, meat packing facilities started to shut down due to the rapid spread of the COVID-19 virus among workers. Furthermore, meat producers and processors faced difficulty in harvesting and shipment of the products due to lockdown situations, decrease in labor force, restrictions in movement of animals within and across the country and change in legislation of local and international export market. These conditions adversely impacted the meat industry due to decrease in meat production, processing and distribution facilities. It is suggested that the integration among all the meat industry stakeholders is quite essential for the sustainability of the industry’s supply chain to cope with such devastating conditions the future may hold.

Labor is a huge issue in the meat processing industry. This industry is easily prone to shortages as it’s hard work that often doesn’t come with the best benefits, to put it mildly. The pandemic made it even worse as sickness and regulations disrupted the meat processing supply chain.

On top of that labor shortages cause wage inflation at a time when food needs to remain affordable.

Long story short, many stakeholders want meat processing to be highly automated.

Last month, FoodDrive published an article outlining the automation plans of one of America’s largest meat processing companies, Tyson Foods (TSN). To deal with inflation and labor-related issues, the company is training employees and, even more important given the focus of this article, spending $1.3 billion on automation over the next three years. That’s a huge deal.

Sealed Air is the right place to be as its food segment includes a wide variety of products that allow companies to package products.

It delivers packaging machines that reduce the need for labor, and enhance efficiencies while reducing food waste. Food waste reduction is mainly achieved through its packaging products, which allow for a longer shelf life.

Sealed Air

According to the company:

We offer a wide range of fiber, plant-based and plastic material solutions that minimize waste, reduce resource use and overcome labor challenges. By enabling circularity we lessen reliance on virgin materials for both packaging and equipment, expanding advanced recycling capabilities like we have proven through partnerships with Exxon, Sabik and Plastic Energy allows essential packaging to be recovered and reused for demanding applications such as food packaging, while enhancing safety and performance.

The Results Speak For Themselves

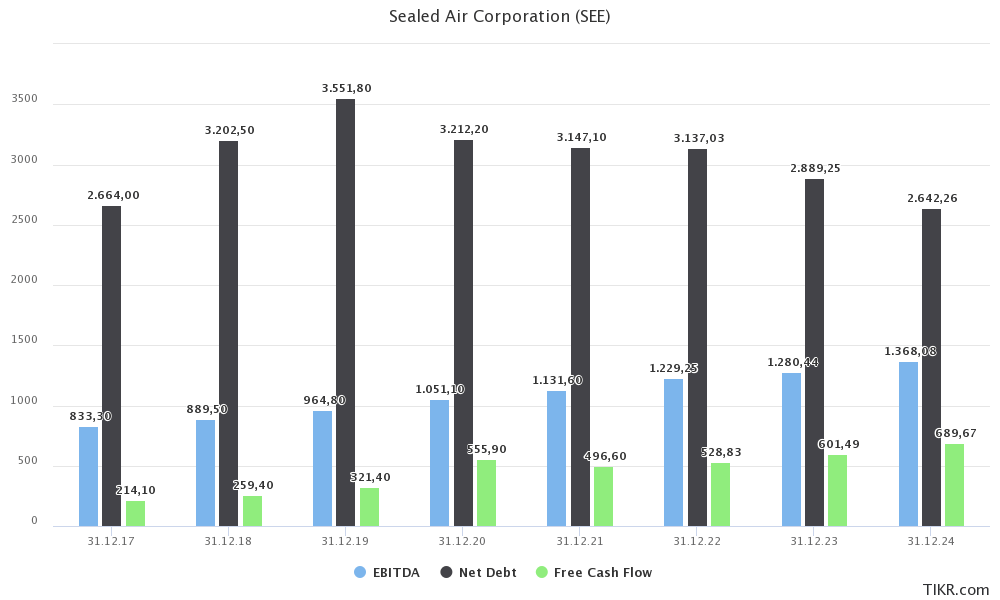

What we are dealing with here is a company that is now consistently improving its financials. For example, between 2017 and 2024E, EBITDA is expected to grow by 6.5% per year. Free cash flow is also accelerating to more than $600 million in 2023. This implies a 7.2% free cash flow yield using the company’s $8.3 billion market cap. It’s one of the reasons why net debt is expected to come down significantly in the years ahead. In 2023, net debt is expected to fall below $2.9 billion, which implies a leverage ratio of 2.3x EBITDA. That’s highly sustainable.

TIKR.com

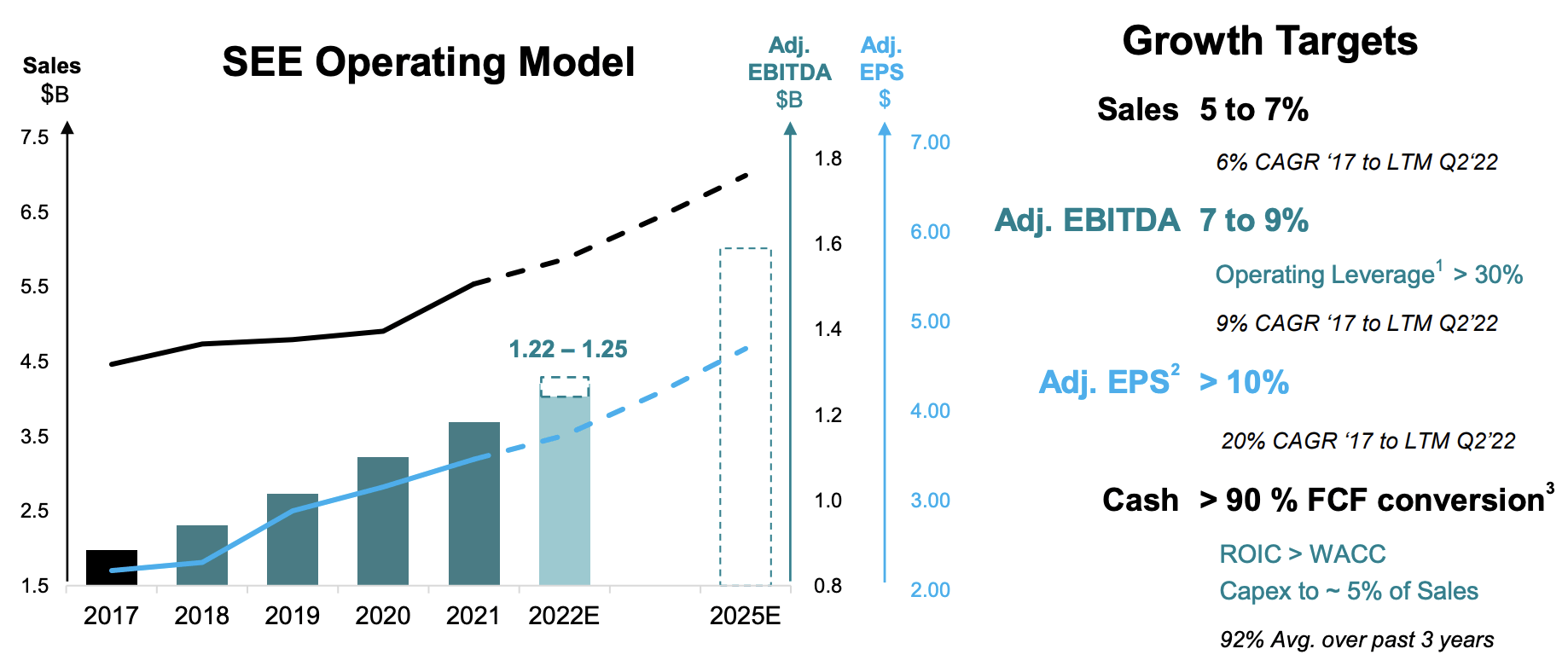

The best thing is that the 6.5% EBITDA growth rate between 2017-2024E is expected to be higher using the 2017-2025E timeline. The company is accelerating its margins after aggressive M&A in the past 10 years.

Now, the company is more positive than “ever” as it expects to benefit from its operating model, which is based on automation, digital, and sustainability. In other words, automation and sustainability, which I discussed, and digital.

In 2025, the company aims to do $1.6 billion in EBITDA, which implies a 9% compounding growth rate per year starting in 2017. Adjusted EPS is expected to grow by 10% after 20% annual growth between 2017 and 2Q22 (on a last-twelve months basis).

Sealed Air

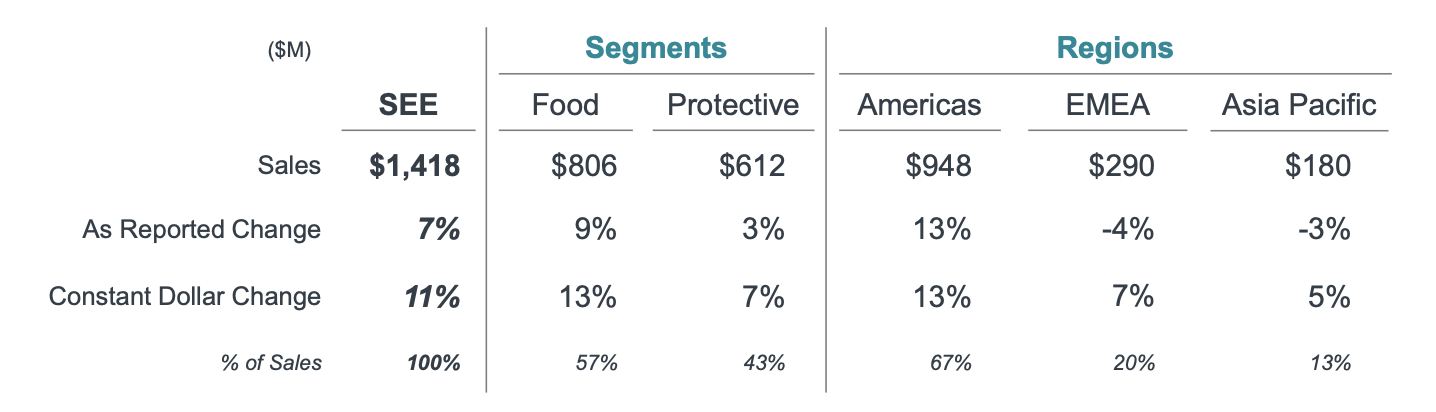

Its just-released 2Q22 results were another sign of strength, at least when it comes to pricing. The company did $1.42 billion in revenue. This was up 6.8% versus 2Q21. It is also $10 million below estimates, which I believe can be neglected.

Total non-GAAP EPS came in at $1.01, which is $0.05 higher than expected.

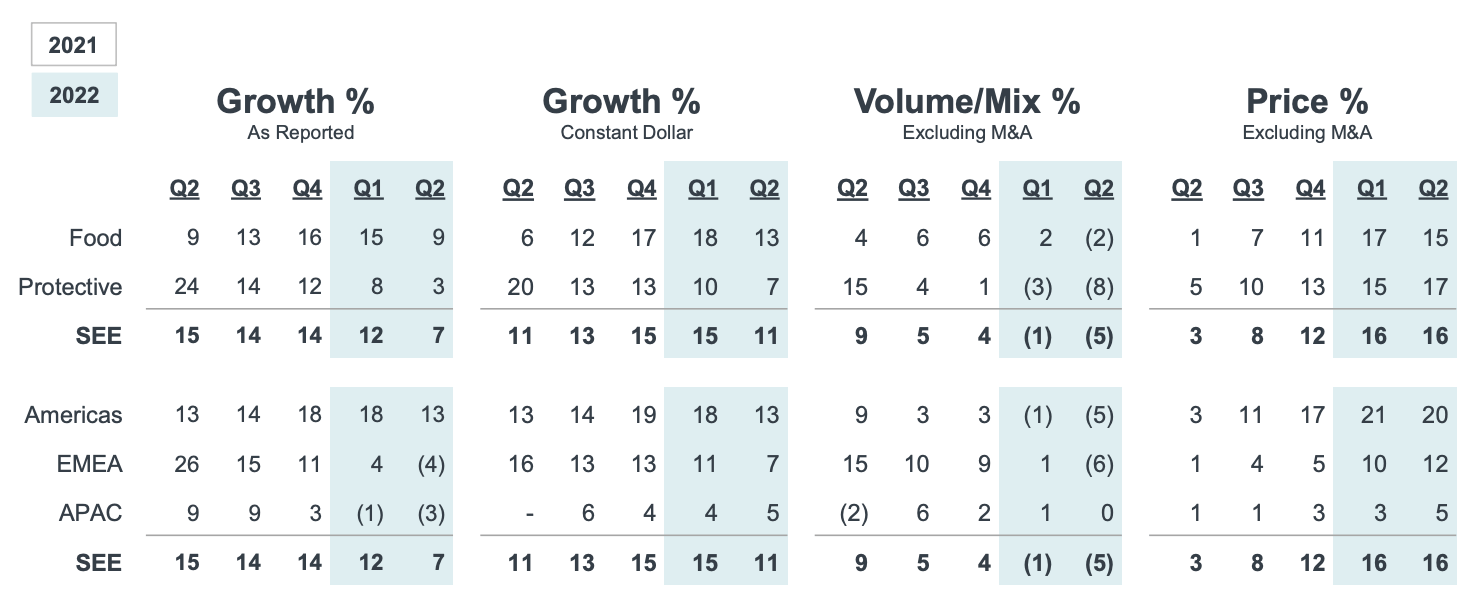

Outperforming sales growth was generated in the food segment where sales rose by 9%. Excluding dollar strength, it would have been 13%. Moreover, on a constant dollar basis, sales were up in all regions.

Sealed Air

The problem is that volumes in both segments were down. The reason why sales on a constant dollar basis are up is all because of pricing. That’s not sustainable. Volumes were down due to supply chain problems as the company mentioned in its earnings call.

Sealed Air

In the first half, the company improved sales from $2.6 billion to $2.8 billion. $418 million was contributed by pricing. Volume partially offset this number by $69 million.

The company suffered from customers who lowered their inventories as well as the aforementioned supply chain problems that prevented orders from being turned into sales.

What I find interesting is that despite lockdowns in China, volume growth in APAC was flat, hence outperforming other markets. I believe that China will turn out to be a bigger driver of growth than previously assumed in the years ahead as waste reduction, especially in plastics, will be huge for China.

The good news is that Sealed Air stuck to its outlook. As reported by Seeking Alpha:

The Company continues to forecast full-year Adjusted EPS to be in the range of $4.05 to $4.20 vs consensus of $4.11, which is based on approximately 148 million shares outstanding and an Adjusted Tax Rate of approximately 26%.

The Company continues to expect full-year Free Cash Flow in 2022 to be in the range of $510 to $550 million.

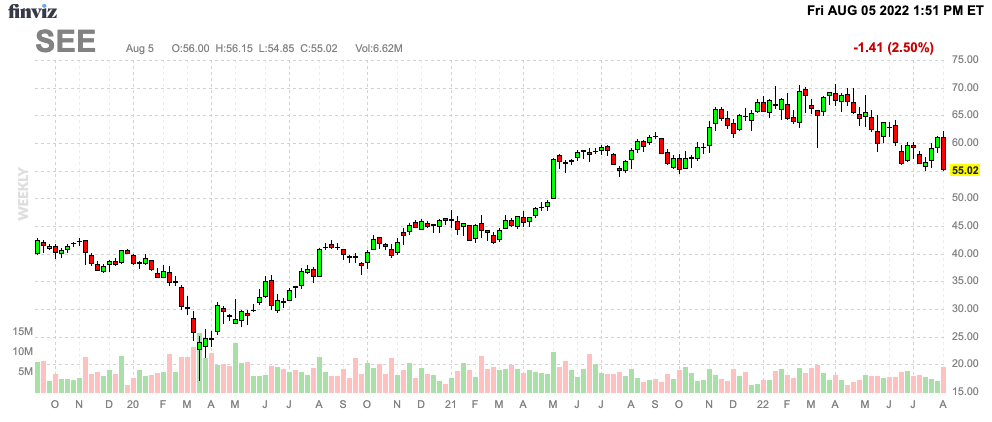

Yet, despite this outlook, investors didn’t like the fact that volumes were down. Inventory reduction at customers and risks in Asia are toxic and a sign that the company is indeed suffering from ongoing cyclical headwinds. Hence, the stock declined by 9% on the day after earnings. This decline continued to currently $55 per share.

FINVIZ

Yet, I believe that a lot has been priced in – too much weakness actually.

Valuation

After the earnings release, RBC Capital’s Viswanathan came out saying that he sees 25% upside potential given the company’s modest FY2023 assumptions.

Sealed Air “seems to be managing supply chain challenges and should continue to see strong equipment and systems sales and benefit from public venues reopening and continued growth in automation,” the analyst wrote, seeing the potential for upward estimate revisions if the company continues to execute.

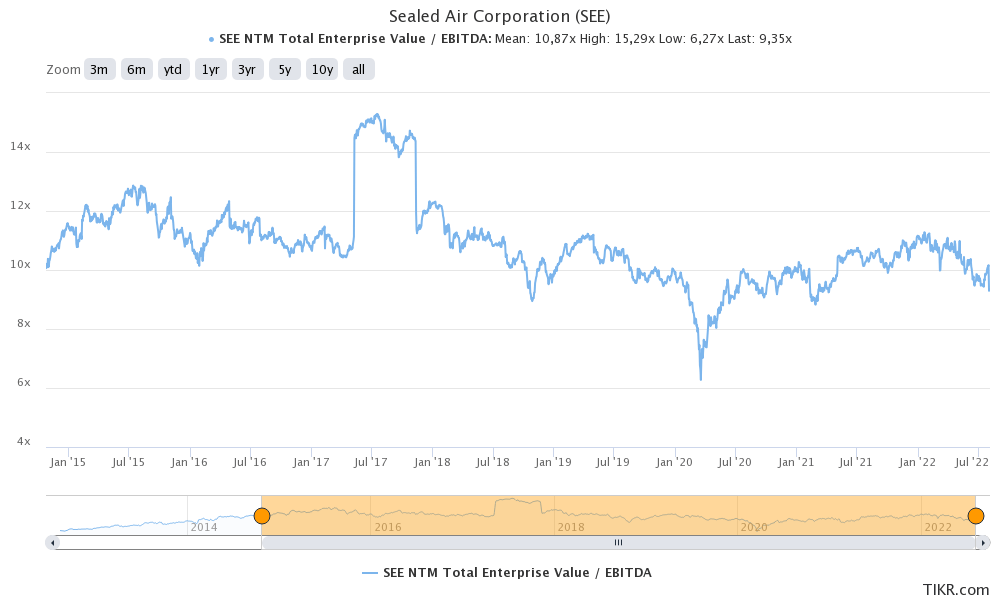

Using 2023 assumptions, we’re dealing with $1.28 billion in expected EBITDA. The company’s $11.38 billion enterprise value is trading at 8.9x that number. In this case, the enterprise value consists of the $8.3 billion market cap, $2.9 billion in expected net debt, and just $175 million in pension-related liabilities.

If we ignore the pandemic sell-off, the company has always bottomed above 9.0x NTM EBITDA. In this case, NTM stands for “next twelve months”.

TIKR.com

With that said, I believe that the company should have a market cap of at least $11.0 billion. That’s 30-35% upside potential over the next 12 months.

However, the problem is getting there. Right now, the market is nervous. Supply chain problems are persistent and companies are lowering orders due to economic headwinds.

Sealed Air is suffering from that despite its long-term secular tailwinds.

Hence, investors looking for Sealed Air exposure should only buy if they are willing to make this a long-term investment. I think SEE will easily beat the market in the future and on a long-term basis. However, the stock is volatile and we’re not out of the woods yet.

Takeaway

Sealed Air is a fantastic company. Unfortunately, its stock price is down 17% year-to-date and unable to recover after its recent earnings. The company does benefit from secular tailwinds including the need for automation in key industries like meat processing, the desire to reduce waste, and automation of packaging and shipping processes.

While the longer-term outlook is fantastic and still on track, 2Q22 was challenging. Customers are reducing inventories and slowing purchasing activities, and on top of that, supply chain issues remain a drag on sales.

The good news is that Sealed Air has pricing power. It will help the company to achieve its 2022 targets, which are hopefully followed by strength in orders in 2023 and beyond.

Moreover, the company is now rapidly reducing its net debt thanks to improving free cash flow and trading at a very attractive multiple.

Hence, I’m still bullish and I believe that there is at least 30-35% upside potential.

(Dis)agree? Let me know in the comments!

Be the first to comment