piranka

In Oct. 2022, Dycom Industries (NYSE:DY) traded in the $100 range before rallying to over $120. But as Warran Buffett famously said in 1987, the stock market is a voting machine in the short run. In the long run, it is a weighing machine. Dycom posted third-quarter results that sent the engineering services firm’s stock sharply lower.

What did investors not like about the results?

Third Quarter Revenue Growth

Dycom posted revenue growing by 21.8% Y/Y to $1.04 billion. It earned $1.80 a share. The company posted a 22.2% rise in contract revenue. Its strong liquidity strength of nearly $45 million enabled it to buy back 304,030 shares at an average price of $93.85.

Revenue grew as Dycom deployed gigabit wireline networks, wireless/wireline converged networks, and wireless networks. Chief Executive Officer Steven Nielsen said that demand from four out of its five top customers increased. This contributed to a gross margin lift of 18.4%, 103 basis points above last year.

Opportunity

Rural America requires increased access to high-capacity telecommunications. Through the JOBS Act, infrastructure investment is part of the $40 billion in funding. Dycom is at the center of providing increased levels of support. The stock should appreciate in value as it generates revenue from infrastructure-related activities.

Dycom is supplying services that include program management, planning, engineering, and design. Those services are across the countries serving multiple customers.

Dycom is deploying fiber networks in rural America. Although customer procurements will grow, the company faces macroeconomic headwinds. For example, tight labor conditions may restrain the work. The increasing cost of capital might result in delays. Although these uncertainties may widen Dycom’s outlook range, it should meet the market’s expectations for 2023.

Dycom’s Customers

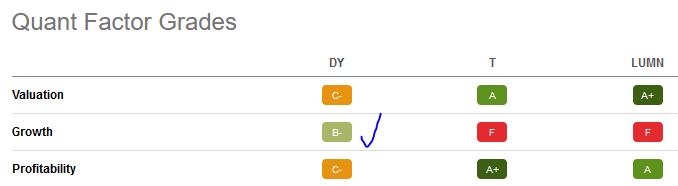

AT&T (T) is Dycom’s largest customer. It accounted for nearly one-quarter of its revenue. Lumen (LUMN) is Dycom’s second-largest customer. It made up 13.7% of revenue. Business with Lumen grew organically by 64.5%.

Income investors may consider complementing their AT&T stock holding with Dycom. DY stock has a better growth grade than either stock.

DY Quant score (Seeking Alpha premium)

AT&T stock rebounded last quarter but still pays a dividend that yields 6%. Conversely, Lumen is a risky holding. The short interest is 13.61%. In addition, the stock lost more than half its value last year:

Dycom Chart (Seeking Alpha)

Outlook

For the fourth quarter, Dycom expects contract revenue to grow by mid- to high-single digits. However, markets sold DY stock when it said that adjusted EBITDA as a percentage of contract revenues would grow modestly.

Q4 is somewhat weaker due to Dycom’s strong business in the first three quarters. Furthermore, the holiday creates seasonal weakness. Unfavorable weather conditions and fewer daylight hours will also slow business during the period.

The higher cost of capital is the risk that investors should consider. In addition, the chances of a recession in 2023 are very high. Dycom is not immune to an economic slowdown. Ahead of the warning, DY stock fell from $105 to $90 on Nov. 22, 2022.

Investors are overly cautious of Dycom’s prospects. It has big customers working through long-term contracts. Infrastructure spending on fiber and networks will continue during that time. The stock’s 23 times forward price-to-earnings multiple is not excessive. Its share price will trend higher once Dycom affirms its baseline growth.

Risks

Dycom could face continued upward pressures in general and administrative costs. Still, the pressures are minimal. The company streamlined the organization during the pandemic. Its back-office costs are minimal. Those structural changes will lead to operating profit expansion in the year ahead.

Related Investments

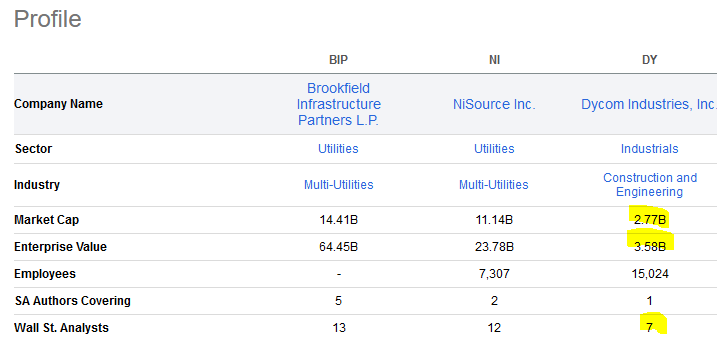

In addition to investing in AT&T, readers may consider infrastructure companies. NiSource (NI) has a quant rating of “hold.” Brookfield Infrastructure Partners (BIP) is rated “sell.” Conversely, Dycom has a “Buy” rating:

DY Quant score (Seeking Alpha premium)

Dycom also has around half as many analysts covering the stock. Its market capitalization is a fraction of companies in the infrastructure utility sector:

Seeking Alpha premium

Your Takeaway

The market braced for a disappointing final quarter after Dycom’s last earnings report. However, it put working capital to good use. This should lift Q4 results higher than management expected.

After shares fell by 23.3% from their 52-week high, the stock does not trade with as big a premium. Most importantly, the increase in government infrastructure projects reaffirms my bullish theme that will benefit Dycom’s business prospects.

Be the first to comment