One of the reasons why I haven’t lost a second of sleep worrying about the market this year is because I buy quality stocks. While I own volatile stocks that kick me in the (you know where) every now and then, it’s about knowing what you buy and why you buy something. In this article, I want to cover one of my favorite long-term dividend growth stocks: General Dynamics (NYSE:GD). This defense giant offers everything I’m looking for in a dividend stock: a decent yield, reliable and consistent dividend growth, low volatility outperformance, and a business model that supports all of these things. Moreover, the company is back on track after a challenging pandemic, which hurt the (commercial) aerospace industry. The company’s order books are filled and higher defense spending is boosting the company’s non-commercial business, including its Navy-related sales.

In this article, I will work you through my thoughts and explain why General Dynamics offers sleep-well-at-night dividends.

The Case For Quality & Dividend Growth

But first, I need to explain why I don’t own General Dynamics. I can keep this short because the reason is simple. I’m overweight on aerospace and defense stocks. Roughly a quarter of my entire net worth is invested in companies with a focus on defense. Hence, I haven’t added new stocks.

With that said, let’s focus on the word “quality” for a second and why it’s important to buy quality.

In a recent article, I highlighted the importance of buying quality stocks. That may be vague because I doubt that any of my followers have ever bought a stock they didn’t expect to be a quality stock.

Using research conducted by WisdomTree, the key takeaway for buying quality was:

Out of all the equity factors, Quality is one of the most consistent. It has a proven track record of outperformance and it typically delivers steady returns across most market regimes. It is ideal for prolonged periods of uncertainty when a bear market rally or a deep drawdown are as likely and it is, therefore, an ideal candidate to consider for a strategic, core investment in equities

At this point, you’re probably wondering how WisdomTree defines quality. Well, this is the answer:

Quality Investing is defined as investing in companies that have some or all of the following characteristics: good management, strong balance sheet, economic moat, sound dividend policy, stable earnings, and profitable and efficient operations.

Some of these things are harder to figure out than others. For example, what’s good management? I think if a company has high margins, a sound dividend policy, and efficient operations, the odds are that management is good.

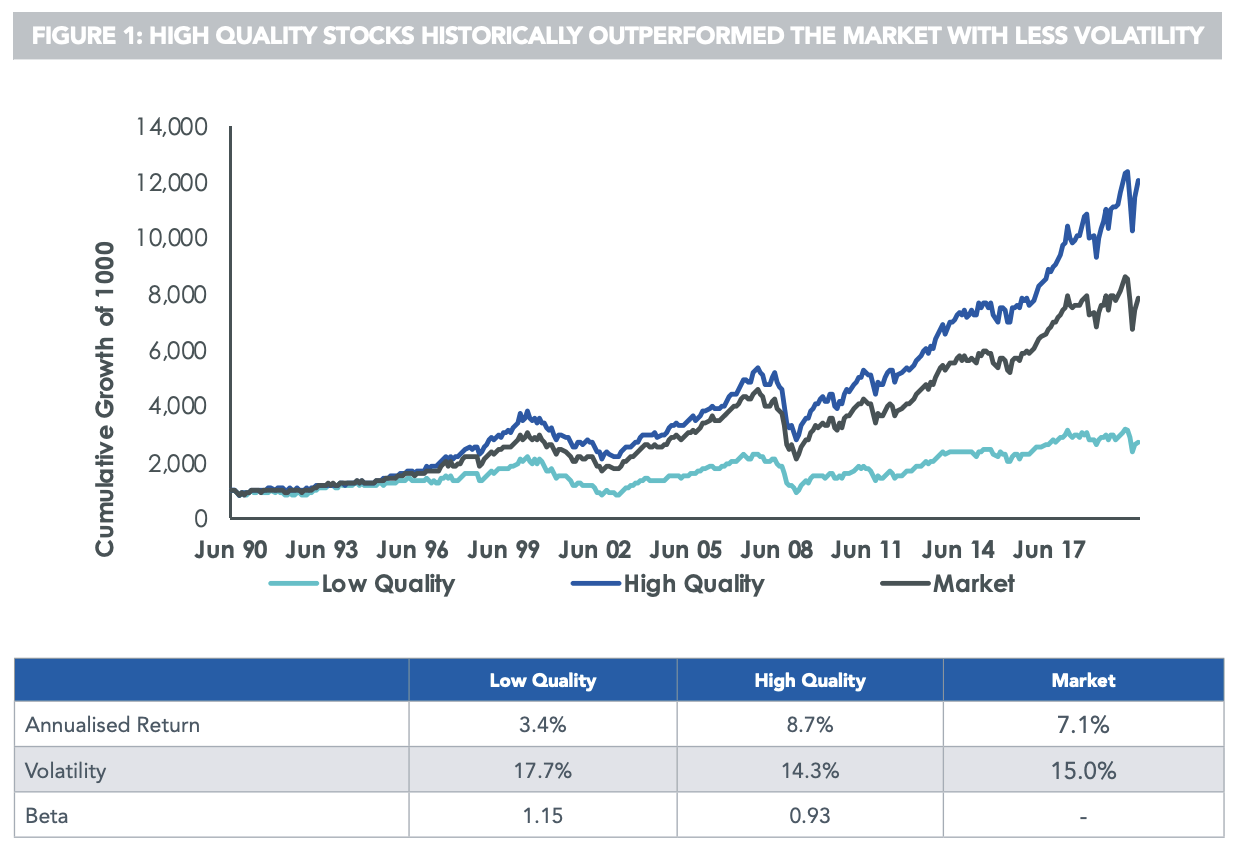

As the WisdomTree chart below shows, high-quality stocks have outperformed the market on a long-term basis because these stocks kept up well during bull markets while doing better during bear markets (because of the quality/value they bring to the table).

WisdomTree

Not only that, but high-quality stocks have outperformed with lower volatility.

With this in mind, I like to focus on the dividend (growth) aspect of a company’s qualities. Being able to pay a dividend (ignoring growth) is a stamp of approval because making a profit is hard. Distributing cash to shareholders consistently is even harder. If a company is able to do this sustainably (without having to borrow money), it’s likely the company is a quality company.

A company that can consistently grow its dividend offers even more quality, as it means the company can also withstand the test of time (competition, changing technologies, you name it) while more often than not protecting investors against inflation as well.

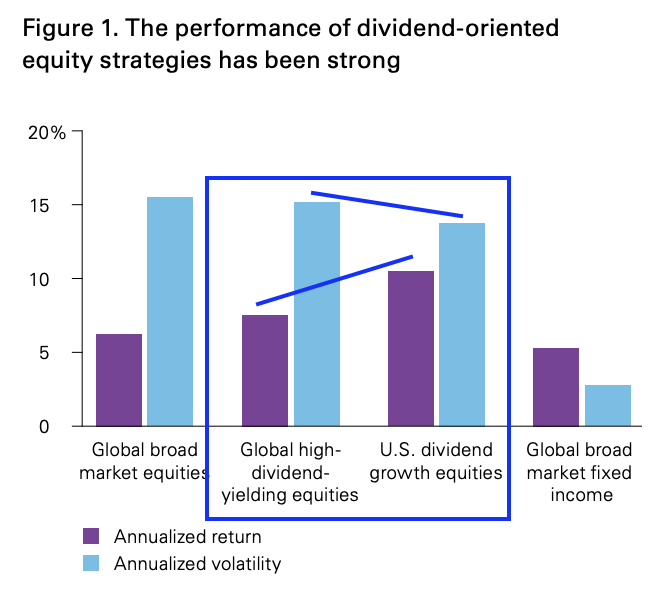

Hence, dividend growth stocks – like the quality stocks above – have a history of outperforming the market with lower volatility as the Vanguard chart shows below.

Vanguard

The point I’m trying to make here is that even if dividend yields are low sometimes, investors need to look beyond the yield as total returns are often much better than one might think. Especially if it comes with subdued volatility.

This is where General Dynamics comes in.

General Dynamics’ Moat

General Dynamics is the 5th-largest defense contractor in the US with a market cap of $64.3 billion. Located in Reston, Virginia, the company has a very interesting business portfolio consisting of both commercial and defense/government products and services.

As the table below shows, the company’s sales are well-diversified as no segment generates more than a third of total sales.

MarketScreener

One of the most fascinating segments is its aerospace segment where the company is a leading producer of business jets. This mainly covers the company’s Gulfstream models.

General Dynamics

The company supports more than 3,000 Gulfstream aircraft in service (the installed base is much larger) and it operates the largest factory-owned service network in the industry, which means the company benefits from new sales, maintenance operations, and aftermarket sales.

Its marine systems segment competes with one of my core holdings: Huntington Ingalls Industries (HII). While other players have marine operations, Huntington and General Dynamics are the two largest suppliers of Navy ships and the sole producers of nuclear submarines for the Navy.

Our Marine Systems segment is the leading designer and builder of nuclear-powered submarines and a leader in surface combatant and auxiliary ship design and construction for the U.S. Navy. We also provide maintenance, modernization and lifecycle support services for Navy ships and maintain the most sophisticated marine engineering expertise in the world to support future capabilities.

As of December 2021, the company had more than $21 billion in Virginia-class submarine backlog alone.

General Dynamics

In its combat systems segment, the company produces the famous M1A2 Abrams main battle tank and Stryker wheeled combat vehicle. While investors like to buy companies that focus on next-gen war capabilities, all of these vehicles are part of multi-domain warfare and a cornerstone of NATO defense capabilities. In other words, demand for these products isn’t going anywhere.

General Dynamics

The technologies segment is much more asset-light as it:

[…] provides a full spectrum of services, technologies and products to an expanding market that increasingly seeks solutions combining leading-edge electronic hardware with specialized software. The segment is organized into two business units – Information Technology (“GDIT”) and Mission Systems. Together they serve a wide range of military, intelligence and federal civilian customers with a diverse portfolio that includes:

•information technology (“IT”) solutions and mission-support services;

•mobile communication, computers, command-and-control and cyber (“C5”) mission systems; and

•intelligence, surveillance and reconnaissance (“ISR”) solutions.

With all of this said, 70% of total sales came from the US government in 2021. 12% from US commercial customers. 10% came from non-US governments. The remaining 8% came from non-US commercial customers. In other words, roughly 80% are government sales, which makes sense given that the (mainly commercial) aerospace segment is roughly 20% of total sales.

Before we look at any other numbers, the company’s business model screams quality. Competition is subdued as GD builds highly-specialized products for governments, which also means that revenues are (somewhat) recession-proof. A large recession would obviously hurt commercial activities, but the main long-term risks are supply risks as we’ve witnessed since the start of the pandemic.

The GD Dividend & Outperformance

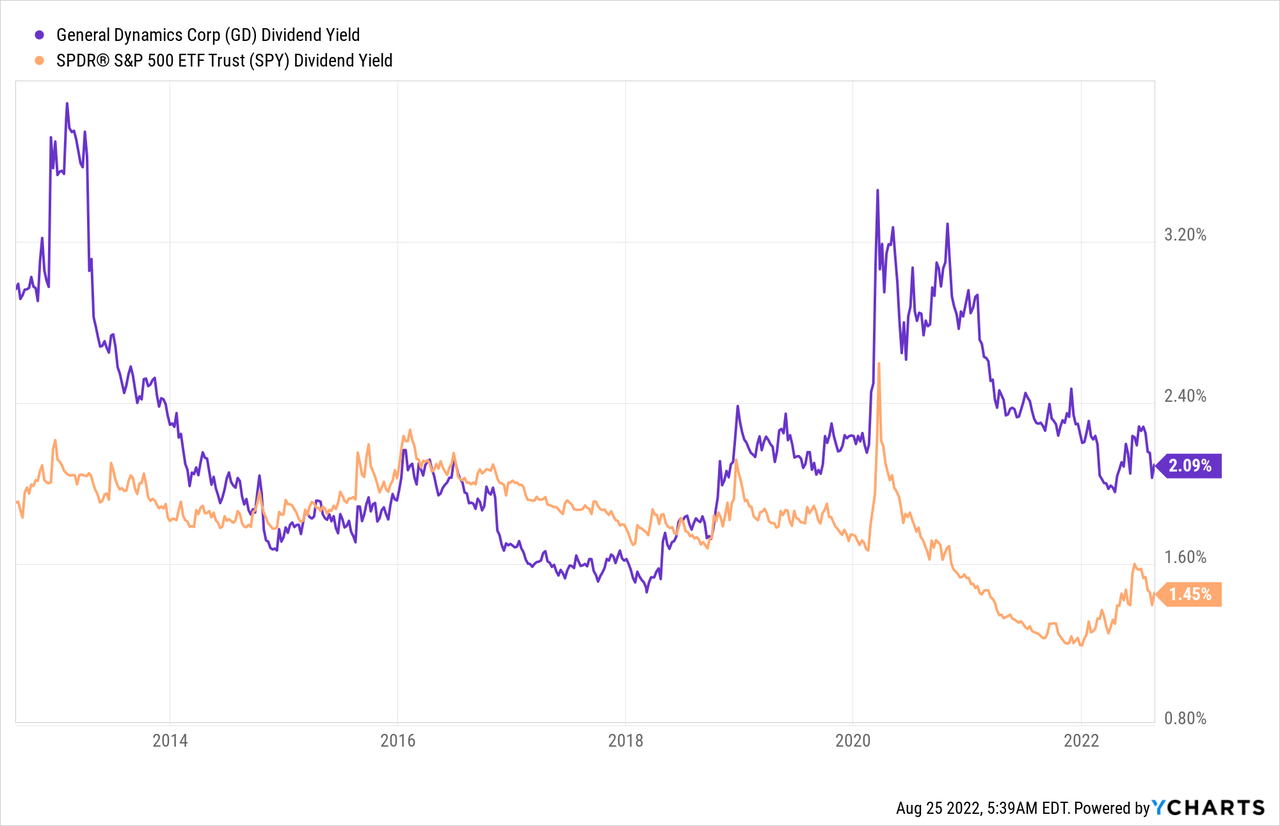

General Dynamics currently pays a 2.1% dividend based on a $1.26 quarterly dividend per share. That’s $5.04 per year per share. It’s roughly 60 basis points above the S&P 500 yield and close to its own longer-term median.

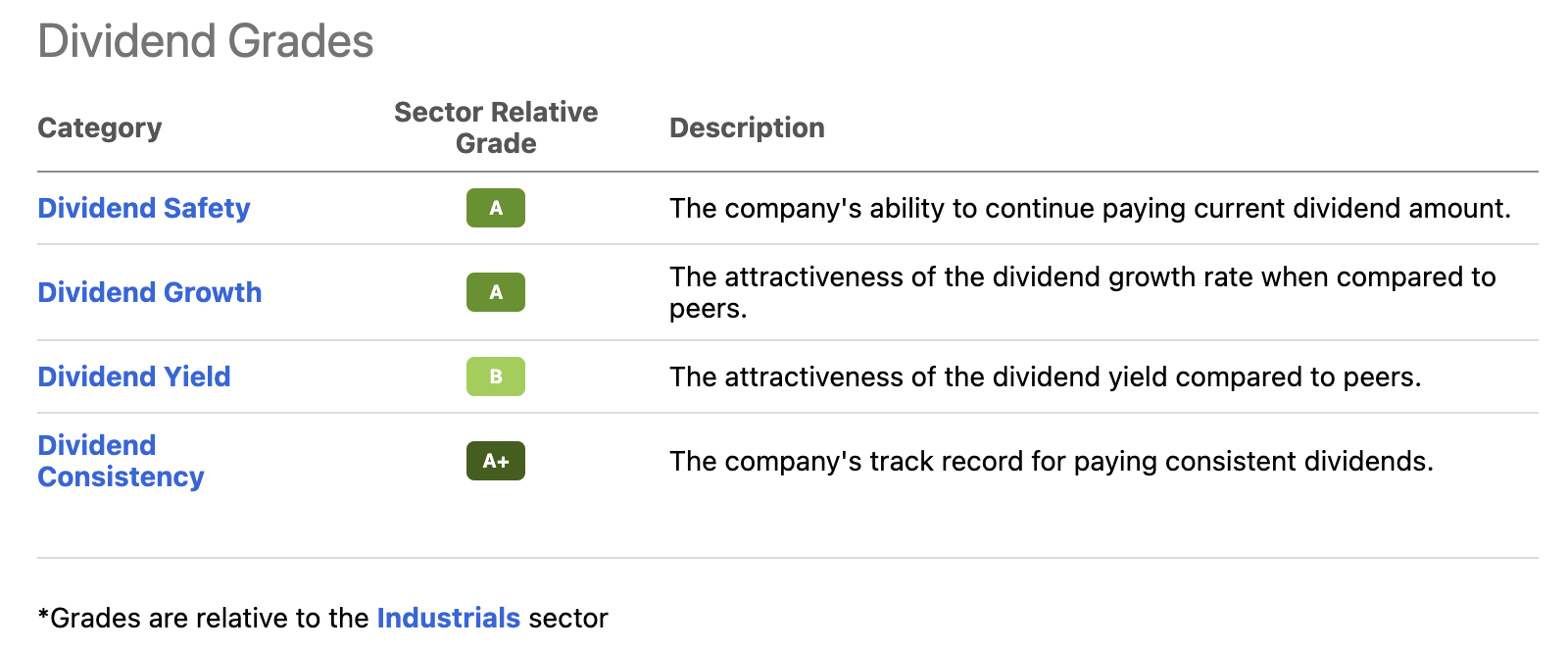

As the dividend scorecard provided by Seeking Alpha shows, the dividend yield scores a B as 2.1% isn’t low, but it also isn’t *that* high. Yet, dividend safety, dividend growth, and consistency all score very high compared to industrial sector peers.

Seeking Alpha

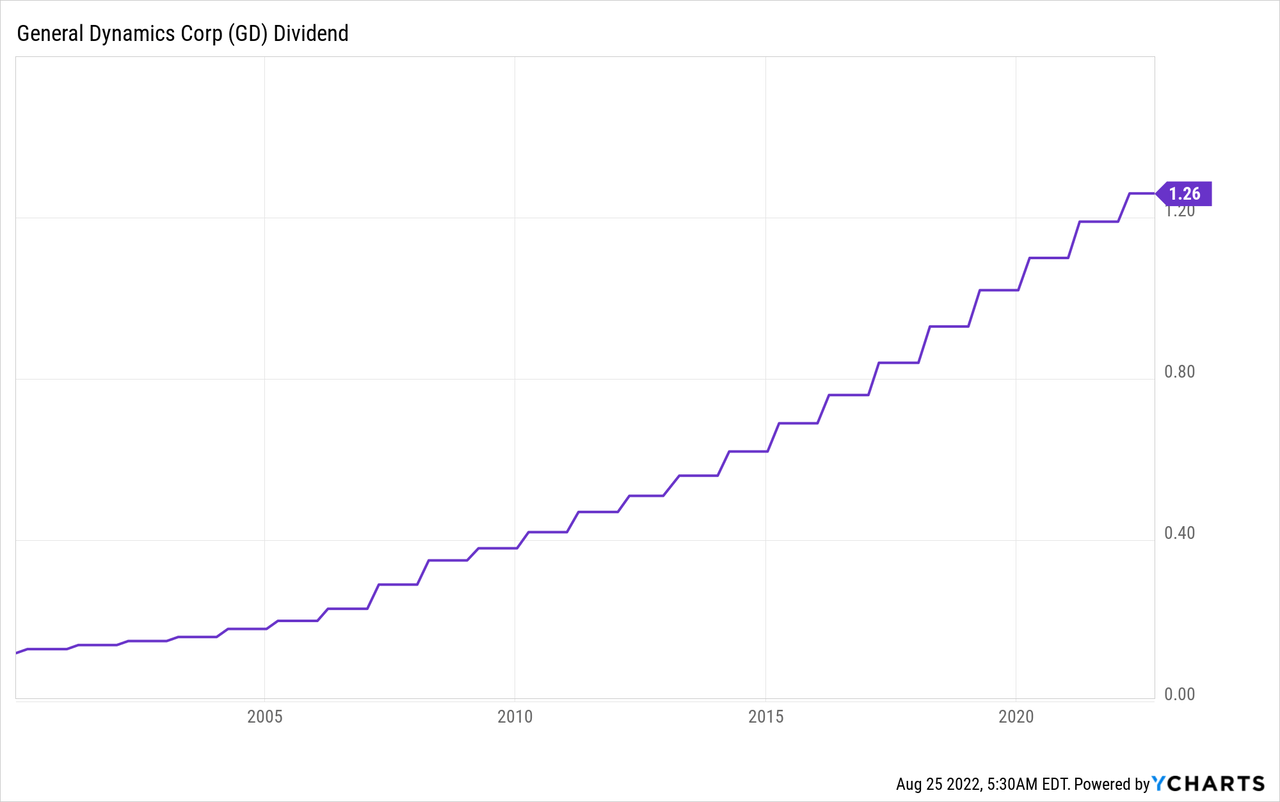

Over the past 10 years, the average annual dividend growth has been 9.6% with consistent hikes throughout recessions.

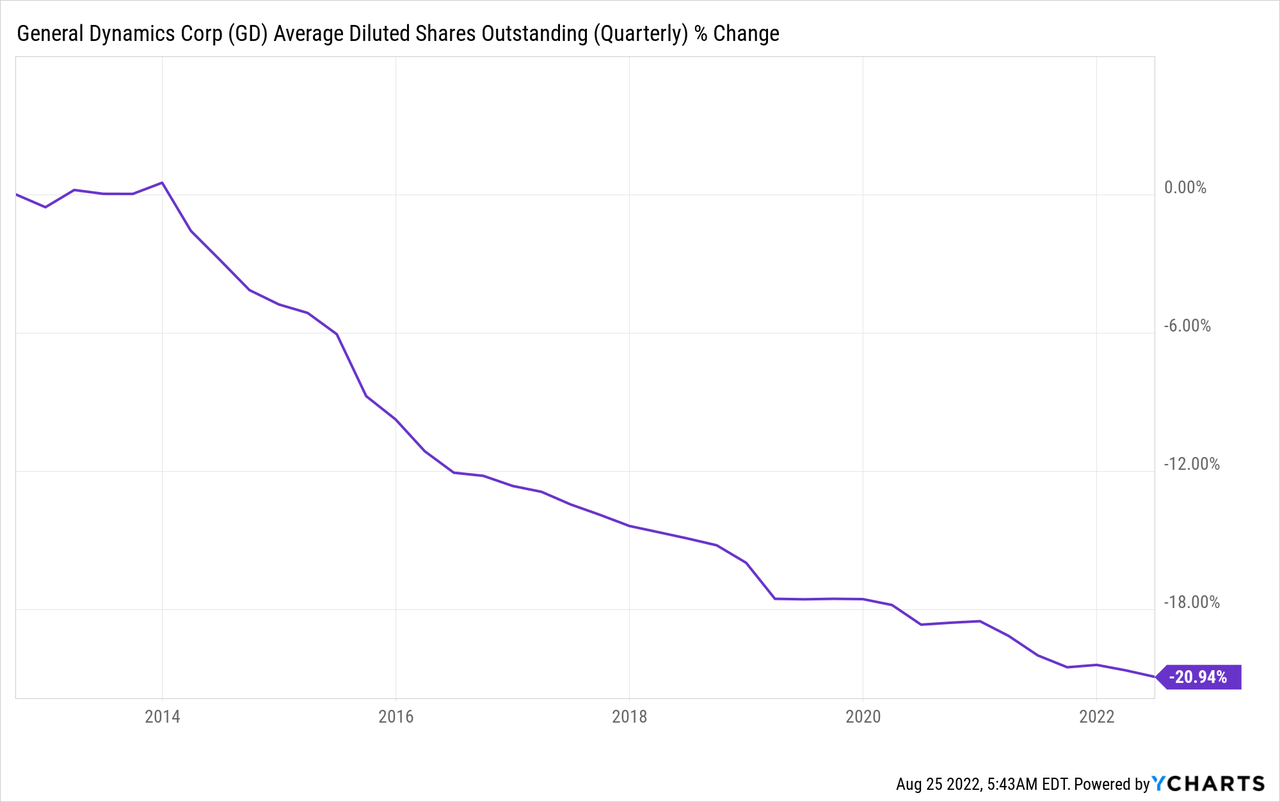

On top of that, GD also engages in buybacks. Over the past 10 years, management has reduced the number of diluted shares outstanding by 21%, adding to (artificial) earnings per share growth.

Now, with all of this in mind, it’s important to mention that the company is indeed doing what we expect from quality stocks, given the theoretical background covered in this article.

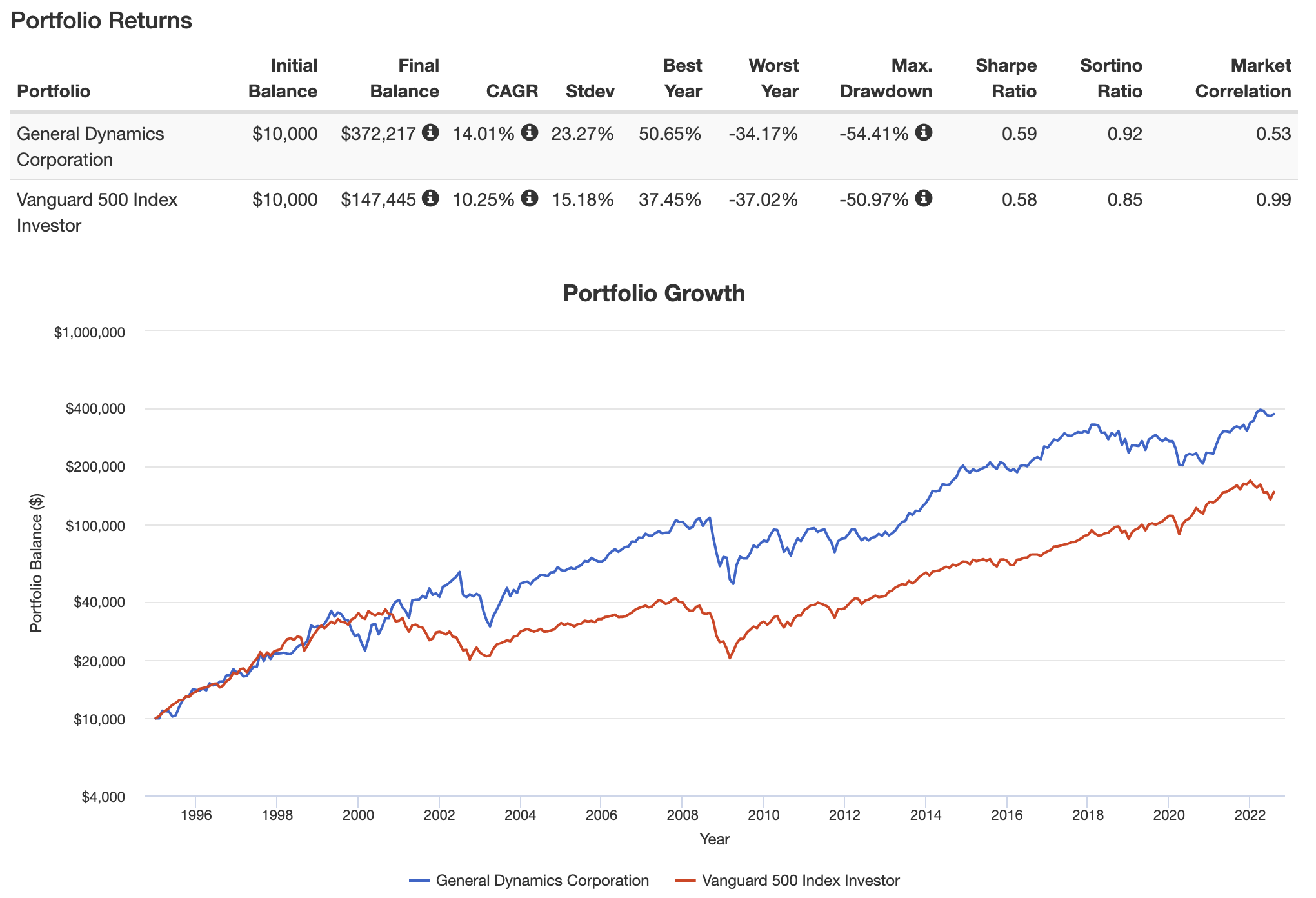

Going back to 1995, General Dynamics has returned 14.1% per year, beating the S&P 500 by roughly 375 basis points. The standard deviation was subdued at 23.3%, which means the company also beat the market on a volatility-adjusted basis (Sharpe/Sortino ratios).

Portfolio Visualizer

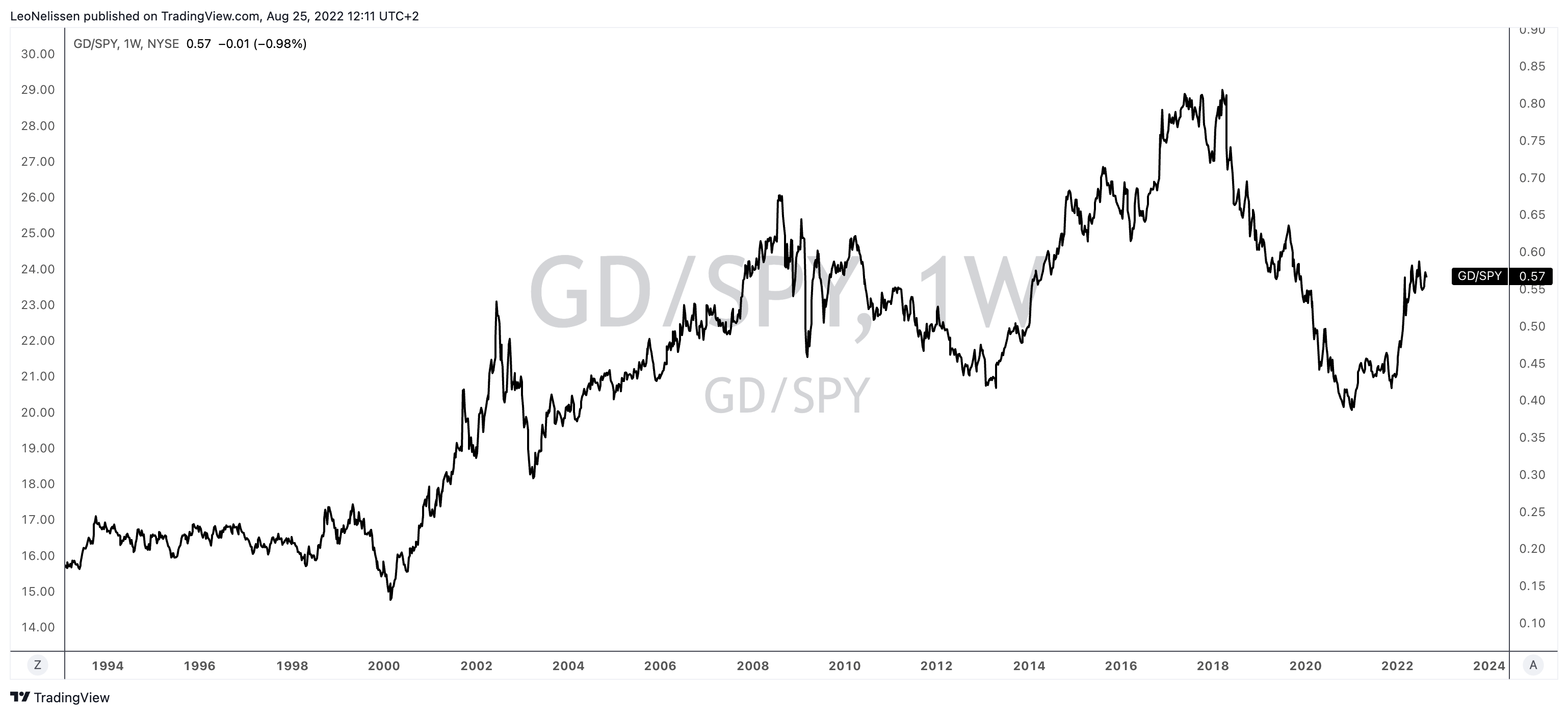

More recently, the stock has underperformed the market as the GD/S&P 500 ratio below shows (including dividends). Underperformance started when global growth peaked in 2018. This was then accelerated by the pandemic. After the 2020 bottom, GD was able to outperform again.

TradingView (GD/SPY Ratio – Including Dividends)

I expect outperformance to last as GD fundamentals are improving.

Better Fundamentals Across The Board

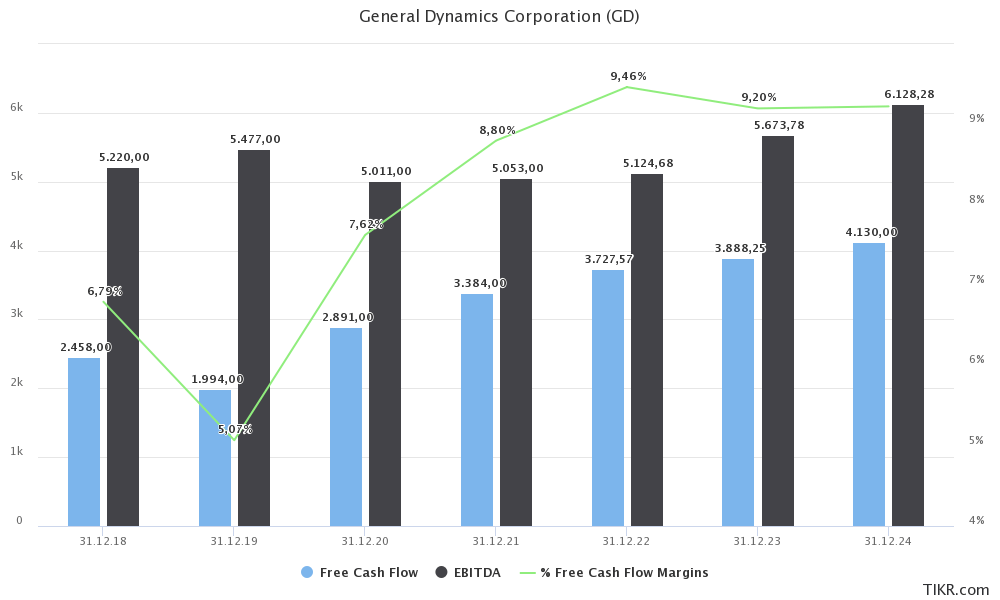

There are two important developments here. EBITDA is set to accelerate after 2022 for the first time since the start of the pandemic. Moreover, free cash flow improved during the pandemic as the FCF margin rose above 9.0%. Next year, GD is in a good spot to do $3.9 billion in FCF or 6.1% of its market cap. As free cash flow is operating cash flow minus CapEx, the company can spend its FCF on shareholder distributions. After all, net debt is expected to fall to 1.4x (EBITDA) in 2023, paving the way for accelerating shareholder distributions.

TIKR.com

In this case, the company is benefiting from strength across the board. For example, in aerospace, the company has a book-to-bill ratio of 2.2x as of 2Q22, meaning orders are coming in more than twice as fast as the company can turn backlog into finished jets. The company has the highest backlog in over a decade with a total contract value close to $20 billion.

Combat systems backlog improved to $13.4 billion in 2Q22, up from $13.1 billion in 1Q22 as the company will produce new Abrams tanks for Australia and close to $1 billion in Stryker vehicles and Mobile Protected Firepower vehicles with a potential future value of $5 billion.

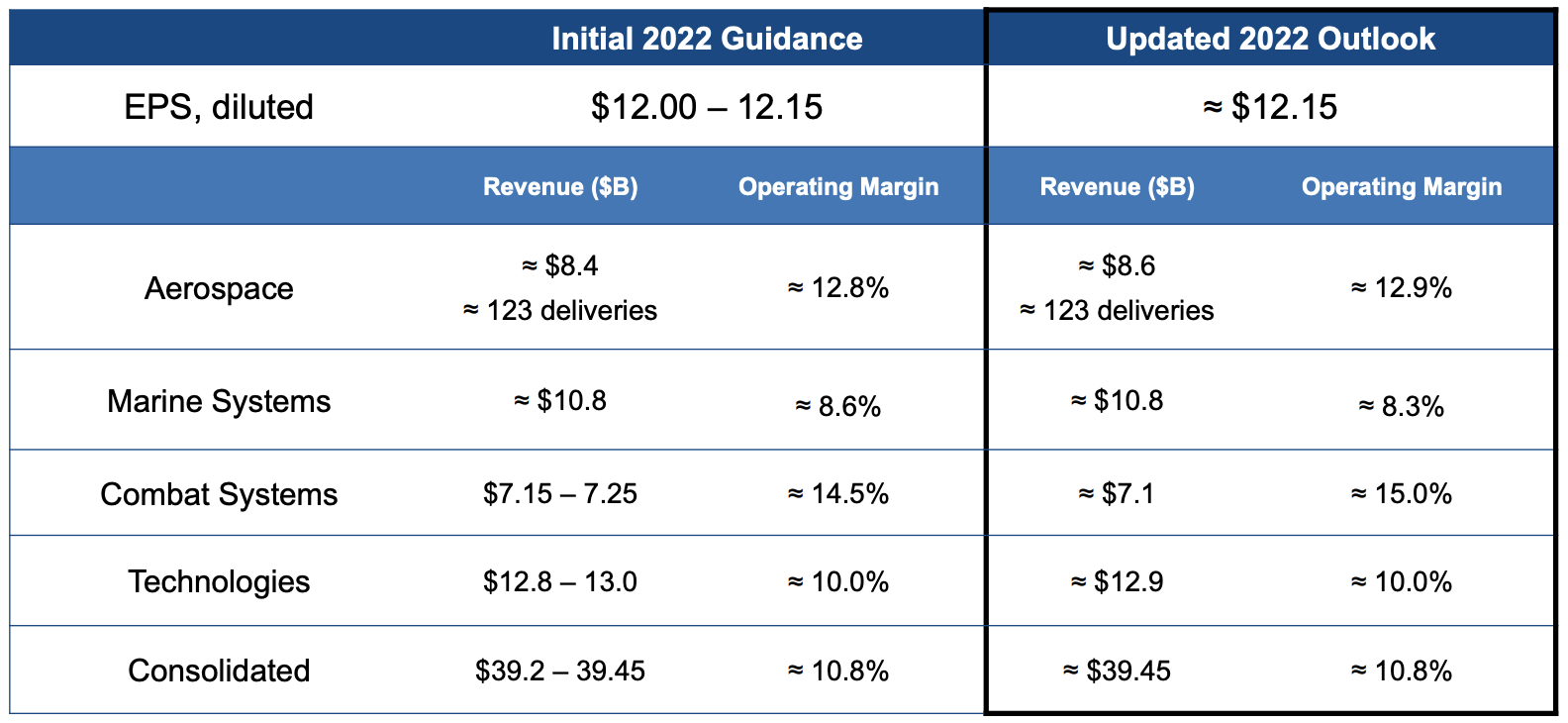

Thanks to aerospace, the company was able to update its guidance as it now sees $12.15 in diluted EPS, that’s the upper bound of its prior guidance range.

General Dynamics

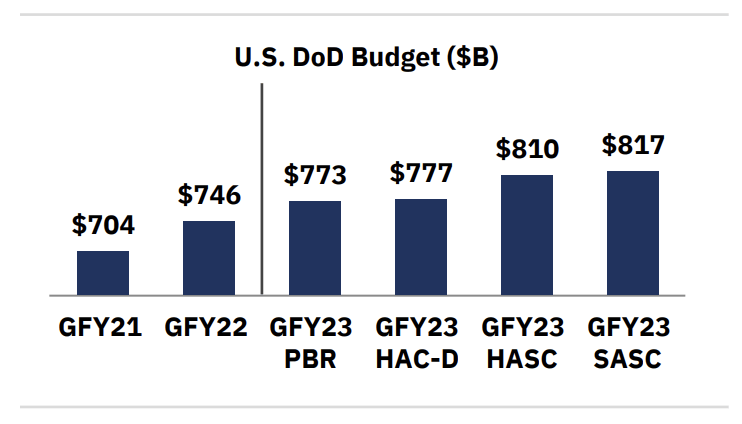

Additionally, and this matters on a long-term basis, the defense budget is improving. As I wrote in a recent Northrop Grumman (NOC) article:

In general, the geopolitical tensions have caused bipartisan support for higher defense spending in the US as well. Note that China has threatened Taiwan as well – especially after Pelosi decided to visit the Island.

In June, Defense One reported that the defense budget for 2023 was on pace to come in close to $860 billion.

“The Senate’s bill includes $817.33 billion for the Defense Department, according to a summary of the legislation released by the committee. Combined with national-security funding at the Energy Department and other defense programs outside the jurisdiction of the bill, the total national defense topline would be $857.64 billion.”

A chart I used in my L3Harris (LHX) article shows that the Senate Armed Services Committee (“SASC”) budget request would exceed the 2022 budget by 9.5%.

L3Harris Technologies

General Dynamics expects to see tremendous tailwinds in shipbuilding and strength in its other segments, although it needs to be seen how spending is applied exactly.

I think the greater area of maybe anxiety or speculation is around Combat Systems and the Army budgets. We’ll see where that goes. This is obviously something that ebbs and flows and has a lot higher beta in terms of an Army budget on an annual basis than on the Navy strategic side.

But the fact is we can’t ignore the fact that there is a significant amount of support among the Congress for increasing defense budgets. So Abrams, Stryker those continue to be very critical assets in the Army infrastructure and we think there’s continued support for those.

Valuation

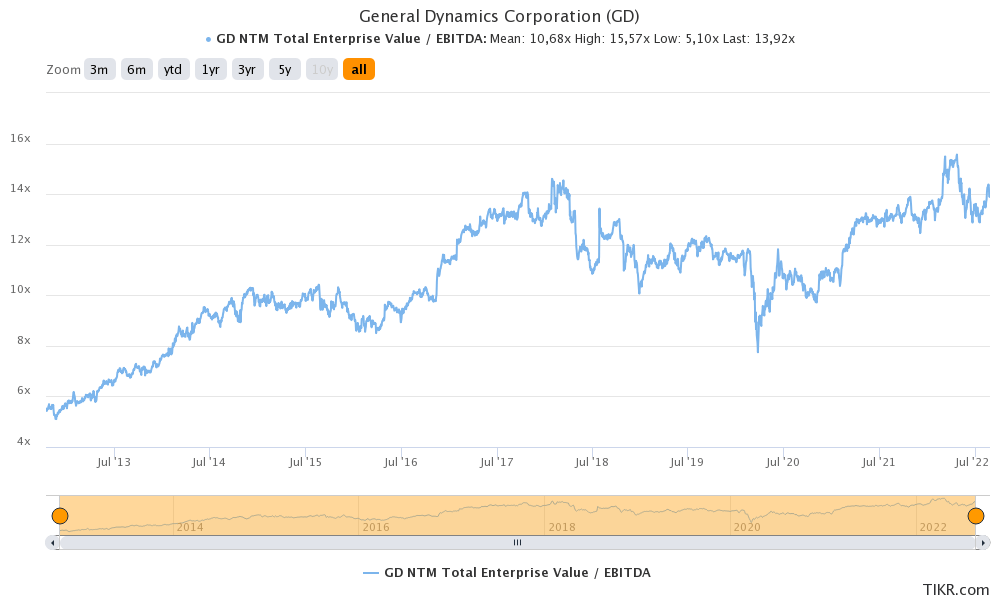

General Dynamics is trading at 13.2x 2023E EBITDA of $5.7 billion. This is based on its enterprise value of $75.0 billion consisting of its $64.3 billion market cap, $8,100 in 2023E net debt, and $2,600 in pension-related liabilities.

This valuation is below the 2022 peak bust still somewhat elevated compared to pre-pandemic levels. What we’re seeing now is that investors are pricing in higher growth as a result of filled order books and rebounding demand in both commercial and defense markets.

TIKR.com

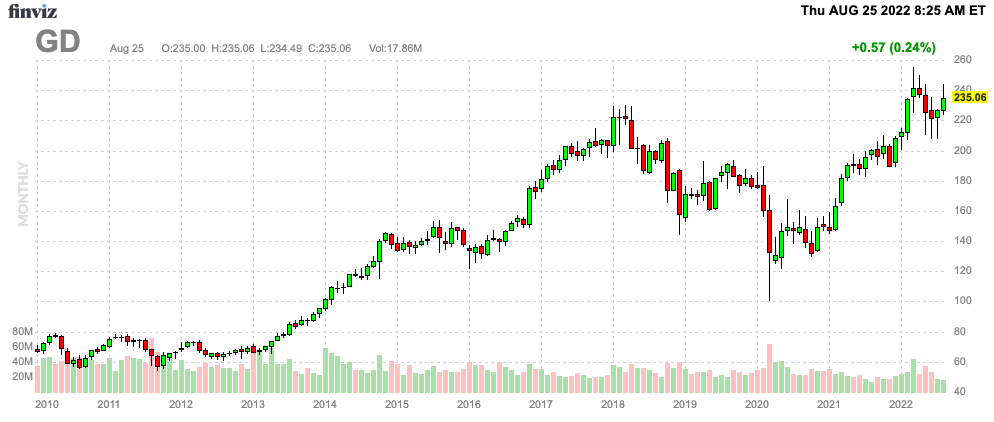

Given that we’re dealing with an implied free cash flow yield of 6.1%, I think GD is fairly valued with more upside.

FINVIZ

Takeaway

General Dynamic remains one of my favorite long-term dividend stocks. The company is a high-quality company by any definition thanks to its well-diversified and high-moat business model, consistent and satisfying dividend growth, decent dividend yield, healthy balance sheet, and a business environment with increasingly healthy fundamentals.

In light of rebounding commercial demand and high global defense spending, I believe that GD is in a terrific position to accelerate both EBITDA and free cash flow growth in the years ahead.

Adding to that, because of its qualities, the company gives investors a high likelihood of outperforming the market with subdued volatility on a long-term basis.

Given the bigger picture, I think GD is a fantastic sleep-well-at-night dividend growth stock for a wide range of dividend-focused investors.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment