Solskin

Investment Summary

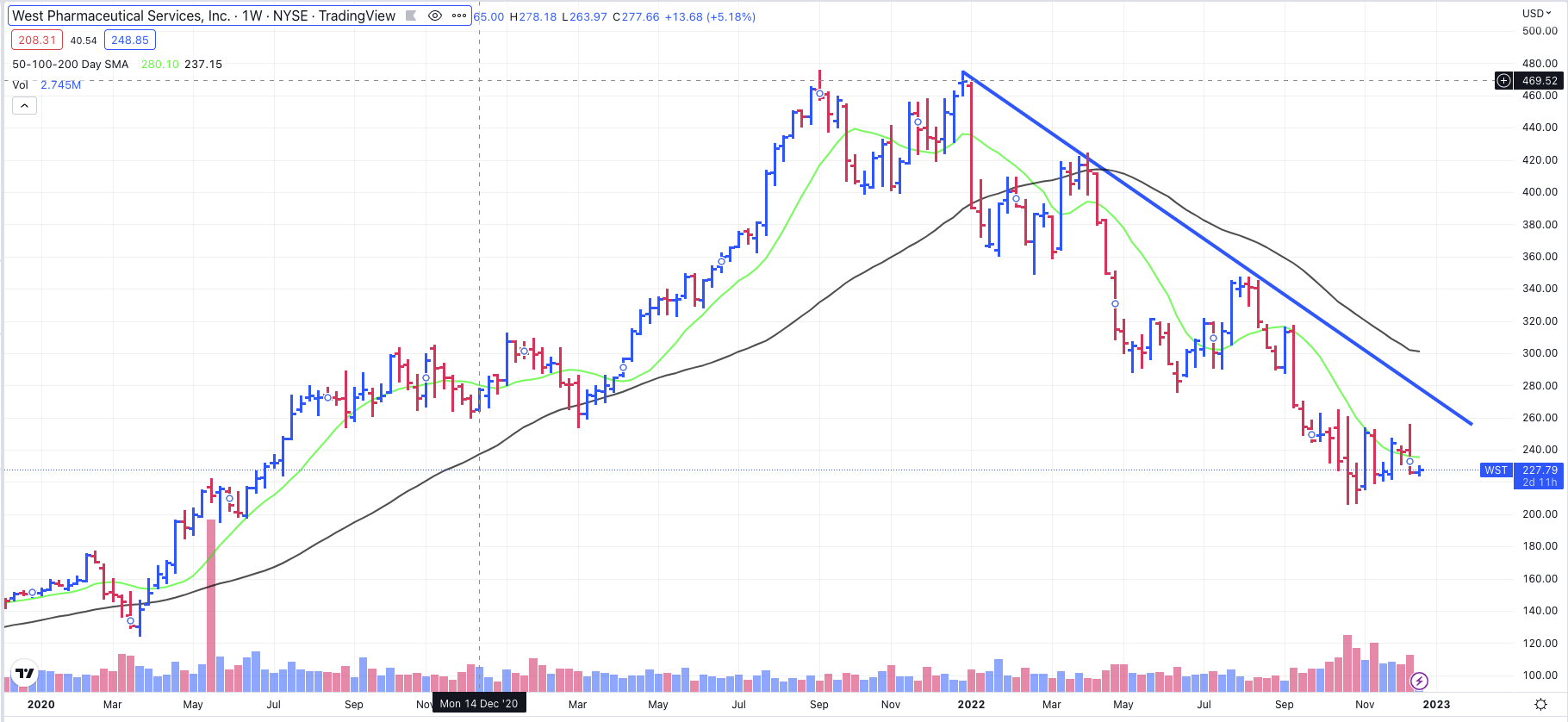

The pandemic era of FY20-21′ was kind to many healthcare/pharmaceutical companies with exposure to the underlying segment. To this point specifically, we had been constructive on West Pharmaceutical Services, Inc. (NYSE:WST) throughout the said period, however, the tide has turned for the long-standing pharma player in FY22′. You can see below that market punishment has been rife for the stock this year. Here I’ll discuss our latest findings on the WST investment debate.

Exhibit 1. WST selloff from December 2021 double-top (weekly bars)

Data: Tradingview

Net-net, given the culmination of potential downside risks that are presented in this report, balanced by reasonable profitability metrics, we rate WST a hold at a $218 valuation. Note, WST’s dividend, which is rated as healthy, is not discussed in this report.

Q3 financials exemplify the previous Covid-19 tailwinds

Starting with WST’s latest set of numbers, we noted the obvious pitfalls of its diminishing Covid-19 revenue. Specifically, we saw that WST experienced a decline in contract manufacturing sales and a decrease in COVID-19-related sales of approximately $20mm ($0.27/share) compared to the previous year.

As a reminder, previously, a large portion of WST’s vaccine stoppers was going to a smaller consortium of customers with fewer product variations. This allowed for higher productivity and efficiency in the company’s high-value products (“HVP”) production system.

However, we’d also note that the transition toward NovaPure syringe plungers has resulted in increased demand from a larger number of customers, and a wider range of drugs and product variations, leading to reduced efficiency in WST’s existing HVP manufacturing sites. Additionally, capacity has been reduced in the company’s HVP operations segment due to a combination of “equipment downtime and delays in the installation of new HVP processing equipment” per management on the Q3 earnings call.

WST estimates that this had a negative impact of $30mm ($0.40/share) on the Q3 run rate. The company expects these issues to be resolved by 2023, although estimates say they will continue to impact WST in Q4 FY22′. Hence, when exactly, we aren’t sure. WST also now expects COVID-19 sales to decrease to approximately $90mm ($1.21/share) for the full year of 2023, a 75% YoY decrease.

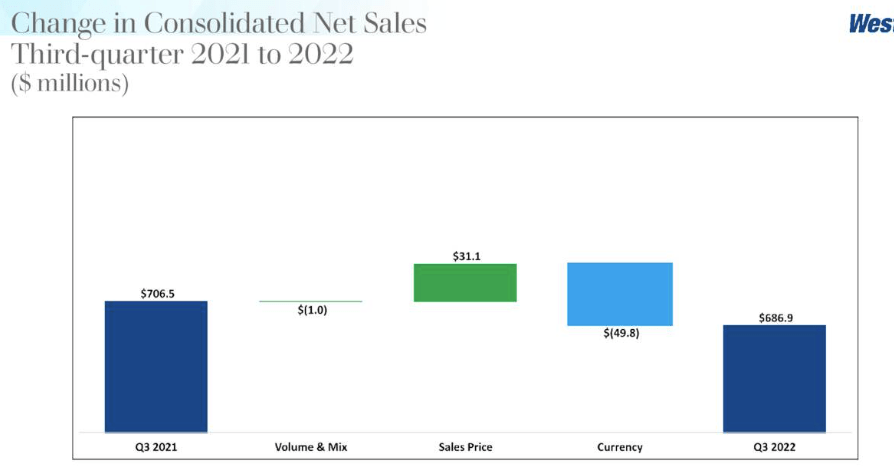

Switching to the earnings result, we noted WST experienced net sales of $686.9mm, a result of organic growth at 430bps. You’ll note however in Exhibit 2 that this is actually a down-step in reported revenues from last year. A foreign exchange (“FX”) headwind of ~$49.8mm is baked into this result. Underlying growth was influenced by an increase in sales prices, contributing $31.1mm or 4.4 percentage points, offset by a decrease in volume and mix of roughly $1mm and a decline in COVID-19-related sales of $20mm as mentioned previously.

Exhibit 2. Reduction in turnover on a reported basis, underlined by product margin mix and FX headwinds

Image: WST Q3 FY22 Investor presentation, Seeking Alpha.

Moving down the P&L, the company also recorded $268mm in gross profit, a 700bps YoY decrease from the prior year. On this, gross profit margin of 39% compressed ~180bps from the same period. Despite this, we saw a 200bps increase in WST’s adjusted operating profit, with a recorded total of $186.4mm in the third quarter compared to $182.8mm last year. It pulled this down to EPS of $2.03, itself down from $2.47 a year ago.

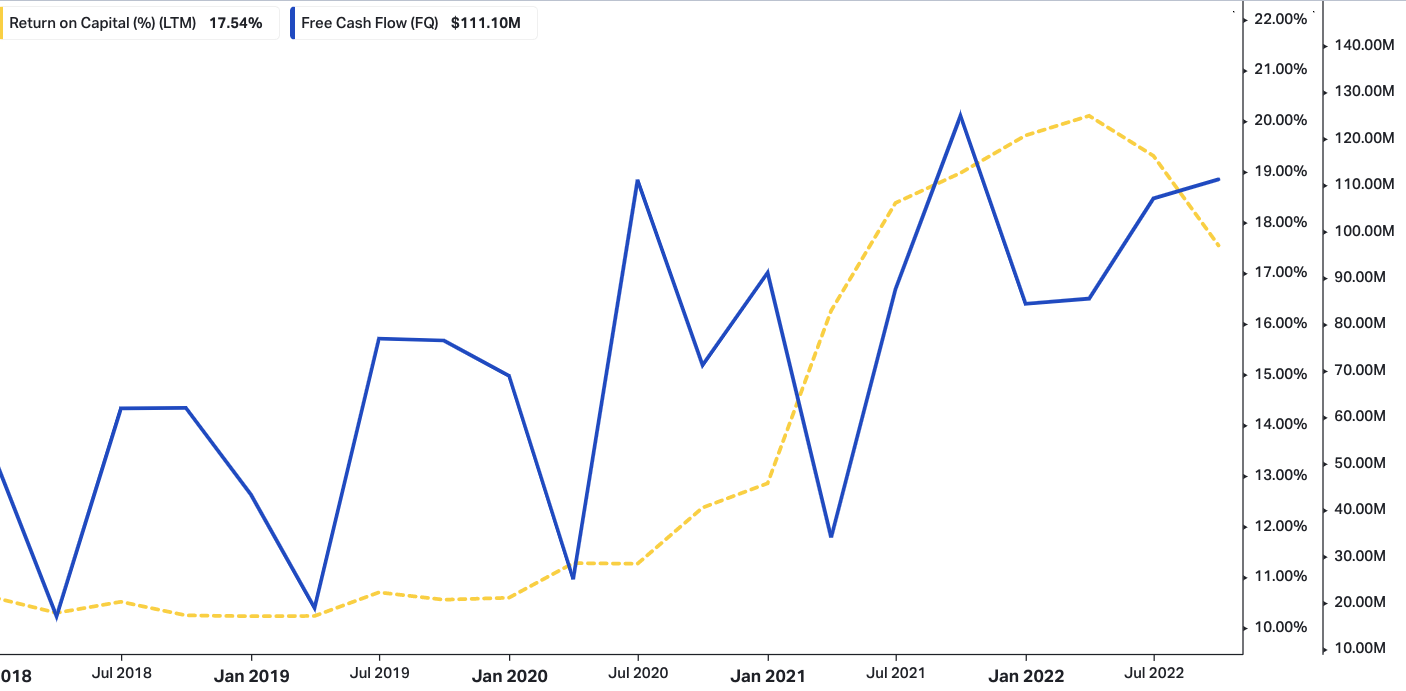

Management also touted working capital advancements by ~$130mm YoY, however, we’d note this was a function of higher inventory and a decrease in free cash flows. You’ll see the latter reflected in the chart below. However, at the same time, WST’s trailing return on capital is a standout in the investment debate at 17.54% and is worth remaining constructive on. The cash production of this company is part of what keeps us neutral versus an outright sell and could potentially be an upside risk to our investment thesis should WST outperform at the bottom line in FY23.

Exhibit 3. Cyclicality in FCF matched by NWC movements and reasonable return on capital

Data: HBI, Refinitiv Eikon, Koyfin

Looking at the segment takeaways, there was reasonable growth across the portfolio. For instance:

- Proprietary product sales saw organic growth of 5.5% in the third quarter. This stemmed from mid-single-digit growth in both the biologics and generics market units.

- It’s also worth advising that its pharma market unit experienced low-single-digit growth, driven by the HVP unit, including NovaPure and Westar components. In fact, HVP comprised 72% of proprietary product sales in the quarter.

- Despite volume declines, contract manufacturing Q3 gross profit margin of 17.3% was 120 basis points aloft last year. The increase in margin was largely attributed to price increases in the period.

With respect to guidance, management now expects a revenue range for FY22 of $2.83-$2.84Bn, a revision down from previous estimates of $2.95-$2.975Bn. In our eyes, this presents as a downside risk factor looking ahead, and, tied into the movement of broad equity markets and the distribution of probable outcomes for the global economy, links to our hold thesis on WST’s stock price. On this, it expects to pull in adjusted EPS of $8.15-$8.20, down from $9-$9.15. This also confirms our hold call.

Valuation and conclusion

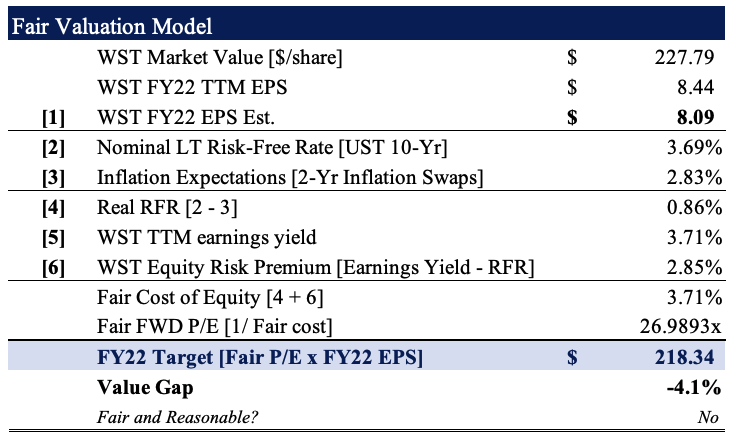

It’s worth pointing out that consensus has WST valued at 27.9-28.2x forward P/E (non-GAAP and GAAP, respectively). We believe this is a slight premium on the stock’s capital appreciation prospects, especially given the guidance downgrades, diminishing Covid-19 revenues ahead, and lack of differentiation on this part.

Our FY22 EPS estimates of $8.09 are based on FY22 EPS sales assumptions of $2.84Bn and adjusted EBITDA of $850.5mm, which is below consensus of $8.17 per share. As seen below, we believe WST should trade at a forward P/E of ~27x, yielding a price target of $218.43 at the $8.09 EPS estimate.

Exhibit 4. Fair forward P/E ~27x $8.09 = $218

Note: Fair forward price-earnings multiple calculated as 1/fair cost of equity. This is known as the ‘steady state’ P/E. For more and literature see: [M. Mauboussin, D. Callahan, (2014): What Does a Price-Earnings Multiple Mean?; An Analytical Bridge between P/Es and Solid Economics, Credit Suisse Global Financial Strategies, January 29 2014]. (Data: HBI Estimates)

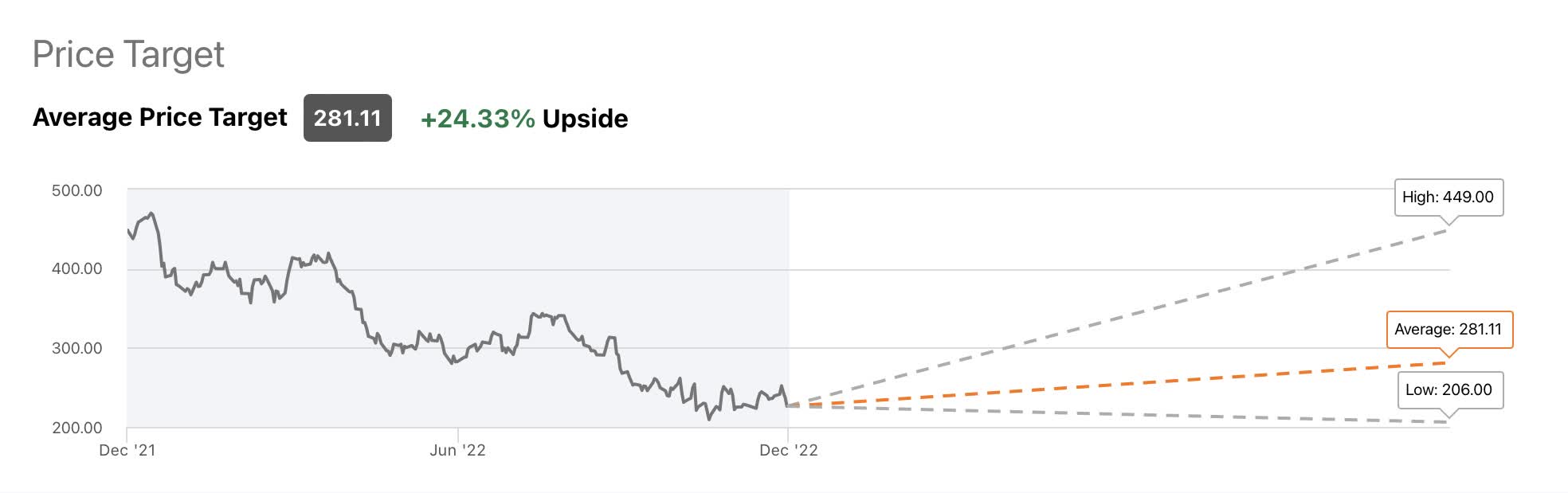

It’s also worth noting the range of analyst price targets for WST and how these stack up with respect to our valuation. In fact, this could be a key upside risk to the investment debate. We’d encourage investors to keep this in mind when moving forward.

Exhibit 5. Range of analyst price estimates for WST in FY23

Data: Seeking Alpha, WST Ratings

As a result of the factors discussed here, we remain neutral on the WST share price looking ahead. Given the culmination of headwinds in the investment debate, we feel comfortable valuing the stock at $218 or ~27x forward P/E.

Be the first to comment