Sjo/iStock Unreleased via Getty Images

The Volvo Group (OTCPK:VLVLY) had a very strong year in 2022, with an increase in net sales of over SEK 100 billion (~$9.7billion) to SEK 473 billion (~$45.9 billion), and adjusted operating income of SEK 50.5 billion (~$4.9 billion). The company also generated strong operating cash flow despite challenges such as disruptions in the global supply chain, high input costs, and production stoppages. In the fourth quarter they continued to see strong growth with an increase in net sales of 31%, 17% when adjusted for currency movements, and they also delivered a record number of trucks in Q4, seeing strong sales in all regions. Construction equipment and bus sales also saw growth, while Volvo Penta experienced good demand. Impressively the company saw a 120% increase in sales of fully electric vehicles and machines.

The company continued to gain market shares in most regions, despite being restrictive in slotting orders for production too far into the future. They’ve done this in order to manage book quality and cost inflation, but as a consequence net order intake has decreased.

Except for China, activity in the construction industry has remained good, thanks to ongoing infrastructure investments and favorable commodity prices. Buses saw sales increase thanks to strong demand in North and South America. Profitability in this business segment has improved but is still low, with an adjusted operating margin of only ~3.4%. Volvo Financial Services delivered good results too, with the credit portfolio continuing to grow and showing low credit losses. Given the strong results, the company is planning to pay 14 SEK (~$1.36) per share in dividends, which at current prices represents a dividend yield of ~7%. We believe this is a very attractive dividend yield, but investors should remember that the Volvo Group operates in highly cyclical industries, which means that earnings and the dividend can vary significantly. It is also important to note that earnings per share for the full year 2022 were SEK 16.09 (~$1.56), which means the company is distributing most of its earnings as dividends.

Financials

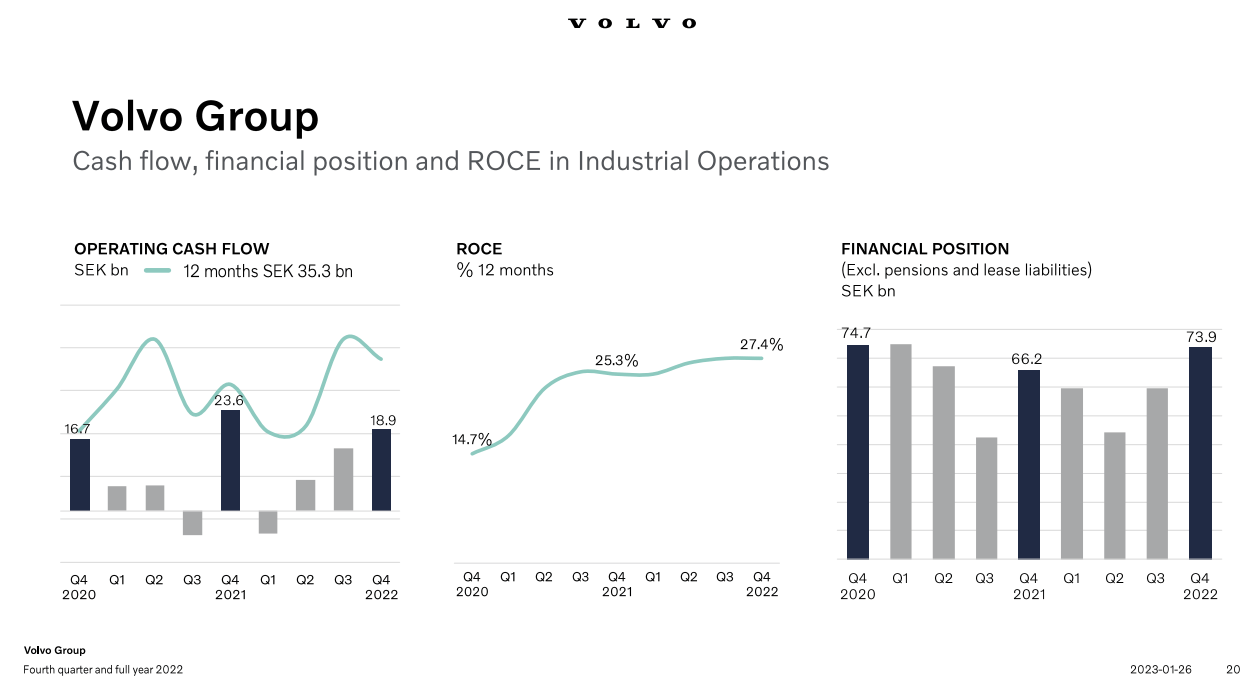

The company’s return on capital employed has been improving, it is generating solid operating cash flows and has a healthy cash position. What this means for investors is that the company is currently in excellent shape, and that is likely why it feels comfortable distributing most of its earnings as dividends.

The Volvo Group Investor Presentation

Electrification

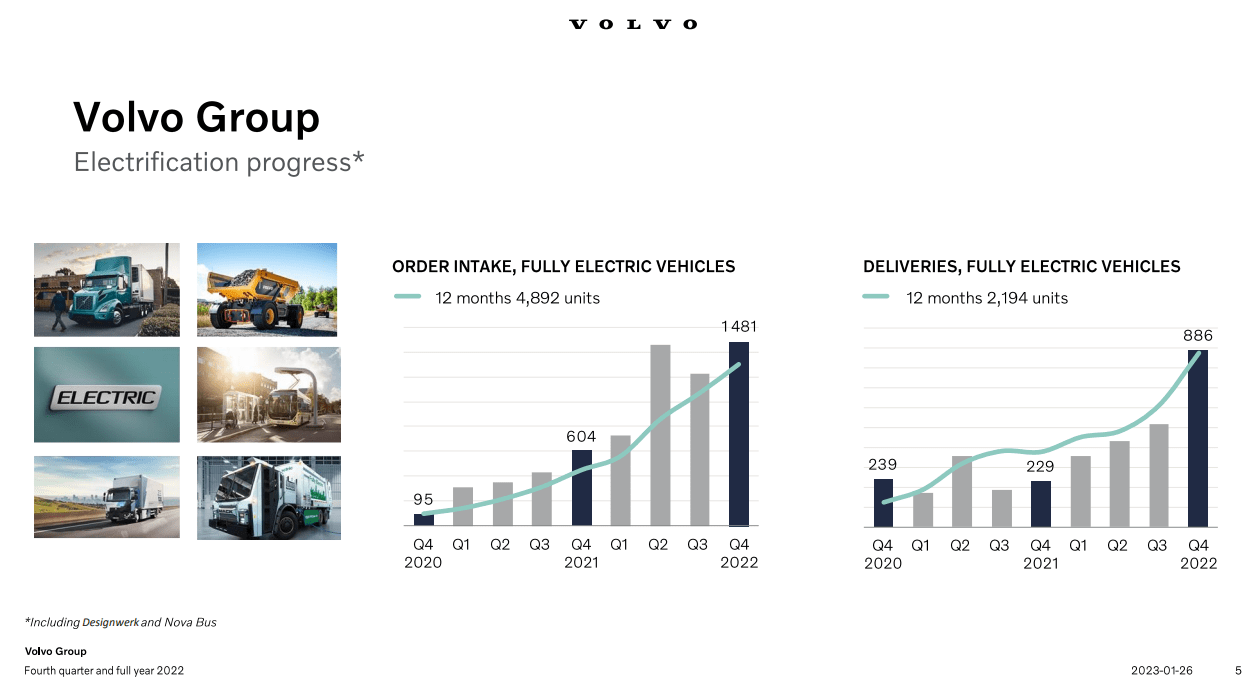

It is great to see that the company is making excellent progress in its electrification strategy. It was announced that the Volvo Group and Pilot Company will create a partnership for a charging network in North America. The company also got XPO Logistic to purchase 100 fully-electric Renault trucks. As can be seen in the slide below, both orders and deliveries of the company’s electric vehicles are increasing very rapidly.

The Volvo Group Investor Presentation

Services

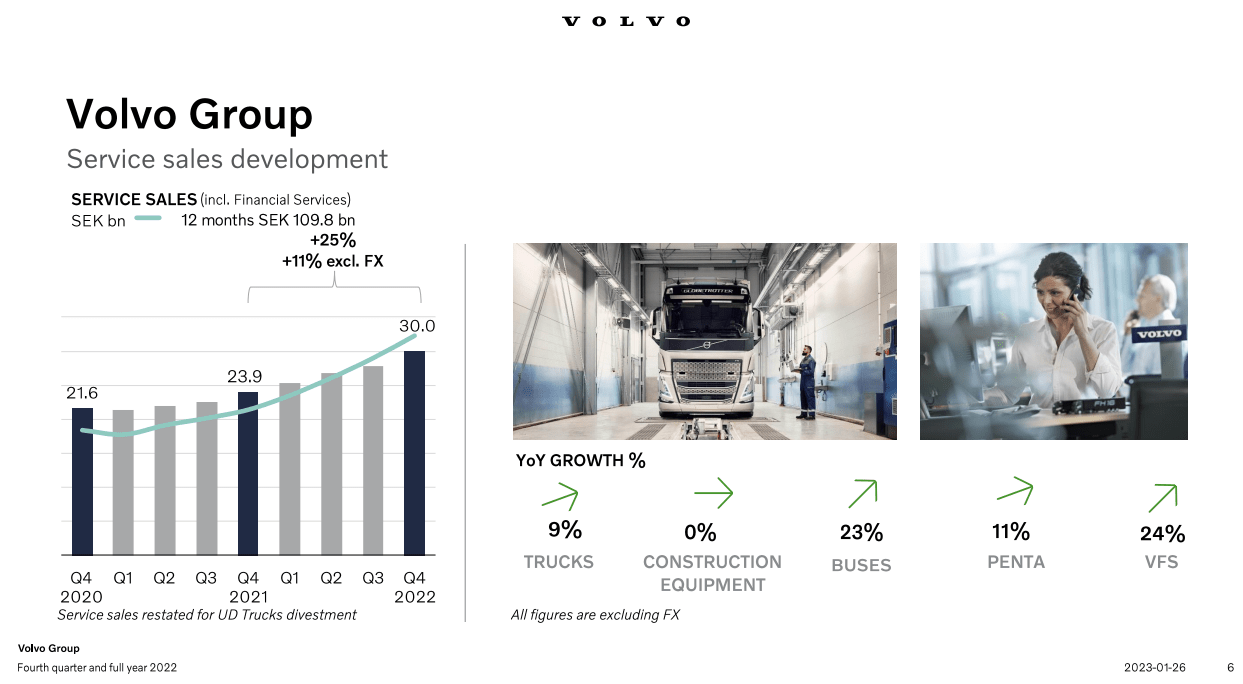

One business area that we would like to highlight is Services, which has been growing nicely, and adds stability to the group’s results, as it is less cyclical. We believe this segment will continue to become more relevant for the Group. Most business experiences significant increases in Service sales year over year, the only exception was construction equipment. In the last twelve months Service sales have been ~ SEK 109 billion (~$10.5 billion), which represents more than 20% of the group’s revenue.

The Volvo Group Investor Presentation

Dividend

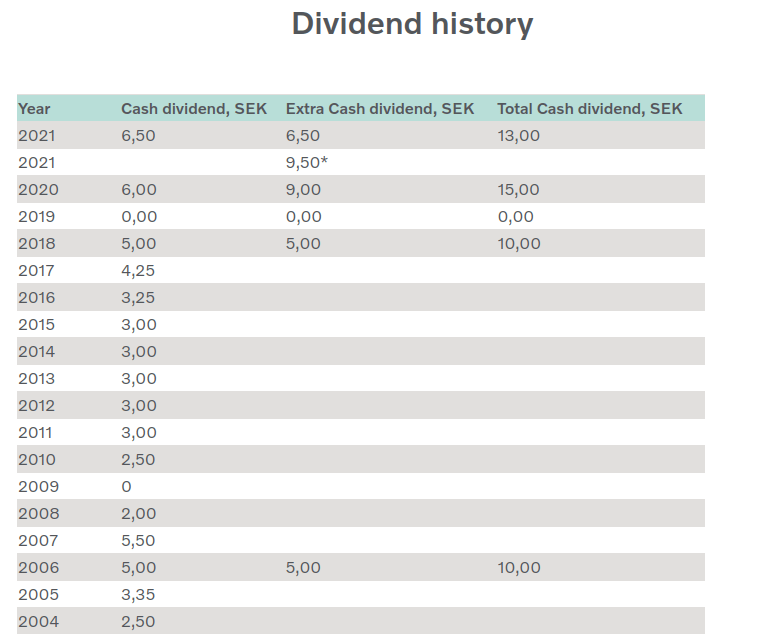

The coming dividend is expected to be 14 SEK per share, an increase from the previous 13 SEK. The table below summarizes the recent dividend history of the company. As can be seen, there have been years in the recent past when no dividends were paid. We believe the dividend at ~7% is attractive, investors should just be aware that as a company operating in highly cyclical industries, it tends to be less stable. Furthermore, the company is paying most of its earnings as dividends, so there is less margin of safety to maintain it should economic conditions deteriorate.

The Volvo Group Website

Valuation

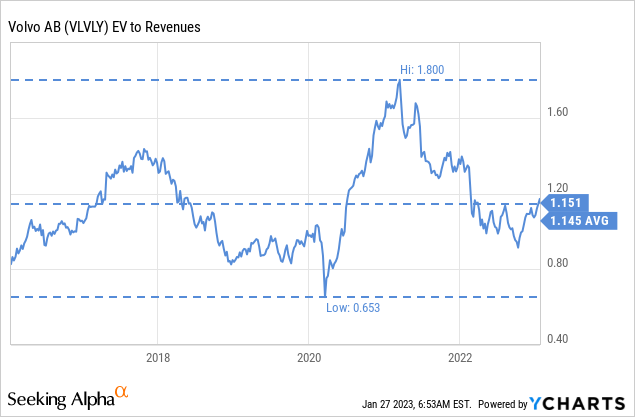

In our previous articles we had been arguing that shares were cheap. Since then shares have gone from ~$15 per ADR to ~$20, and greatly outperformed the S&P 500 index (SPY). We now believe shares to be fairly valued, and are therefore adjusting our rating to ‘Hold’ from ‘Strong Buy’. As can be seen below, the EV/Revenues multiple is now very close to the ten year average of ~1.15x.

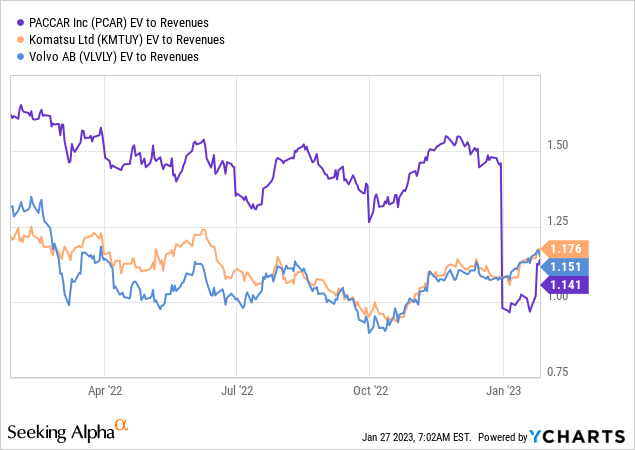

Some of its peers like PACCAR (PCAR) and Komatsu (OTCPK:KMTUY) are also trading with very similar EV/Revenues multiples.

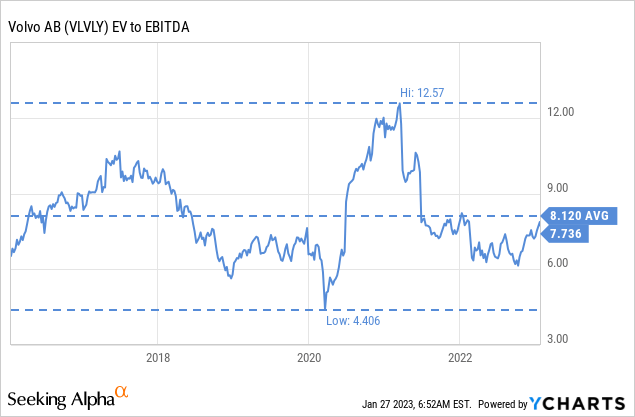

The EV/EBITDA ratio is roughly 7.7x, only slightly cheaper compared to the ten year average of ~8.1x. The price/earnings ratio at ~13x looks reasonable for this type of company. We believe the undervaluation has been corrected, and returns from here will be highly dependent on economic conditions.

Risks

While the Volvo Group has been delivering solid results, investors should not forget that it operates in very cyclical industries. Especially when there is an extremely high probability that a recession is coming soon.

Conclusion

The Volvo Group delivered excellent results for fiscal year 2022. We were particularly impressed by the progress made in its electrification initiatives, and with the growth of the Services business. Income investors will probably find the ~7% dividend yield attractive, it is just important to remember that the dividend is not as reliable as that of some other companies. Looking at the dividend history of the last few years, there were some years in which no dividend was paid. Investors should also take into consideration that the company is paying most of its earnings as dividends, and that this is a company operating in highly cyclical industries. We believe shares are currently close to fair value, trading at close to their ten year average valuation multiples, and as such we are updating our rating from ‘Strong Buy’ to ‘Hold’.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment