Huber & Starke/DigitalVision via Getty Images

NXP Semiconductors (NASDAQ:NXPI) is slated to release its highly-anticipated FQ4’22 earnings on January 30, with investors likely looking forward to better-than-anticipated results from the leading automotive chips semi company.

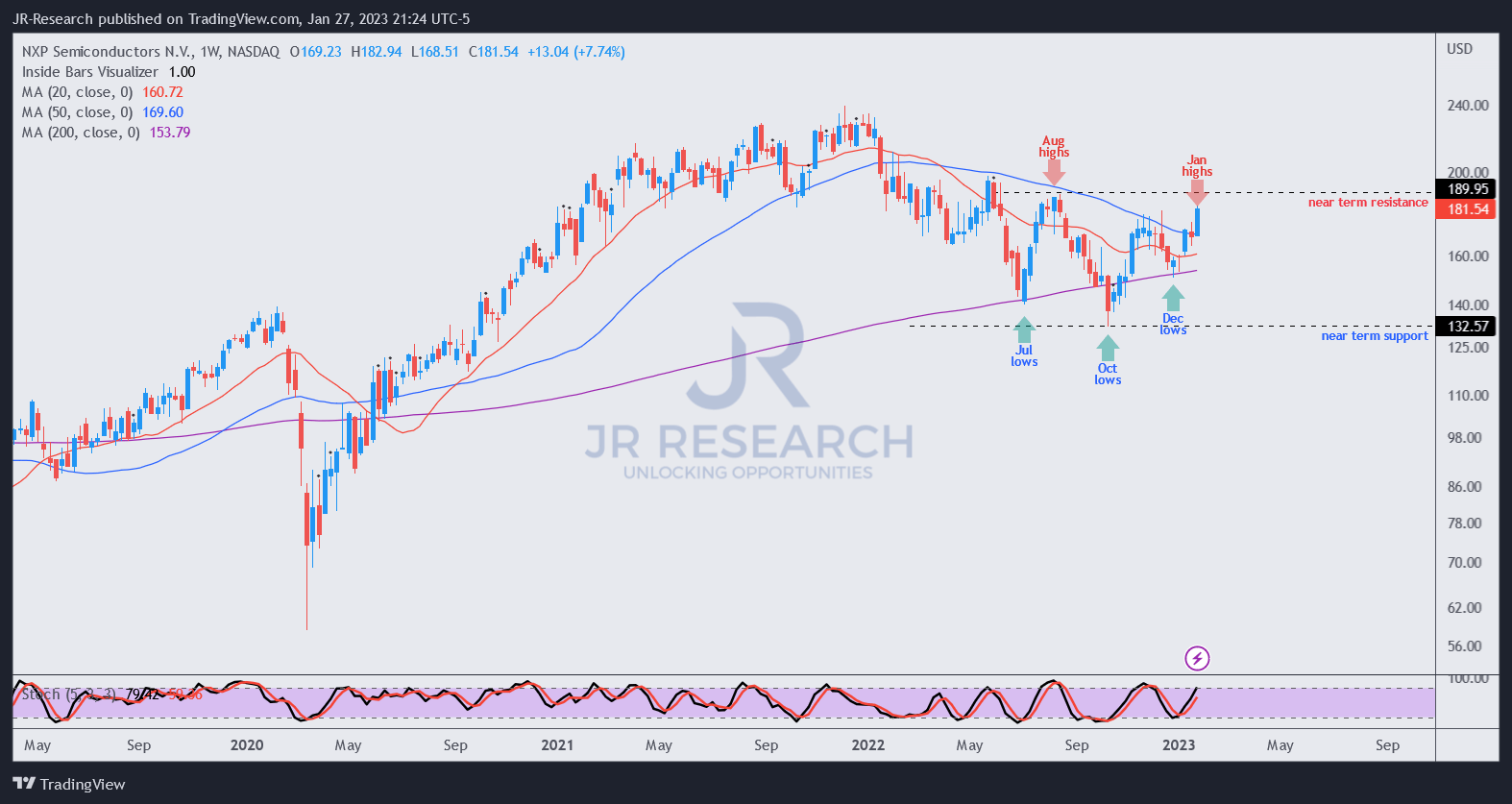

Wall Street analysts’ estimates for FY22 and FY23 have already been revised downward since our previous update in late July 2022, as we urged investors to wait for a steep pullback. NXP fell significantly from its August highs toward its October lows, down more than 30%.

As such, savvy investors have likely capitalized on the terrific reward/risk profile at those pessimistic lows, as NXPI recovered remarkably toward its recent January highs.

Moreover, NXP Semiconductors’ leading position in the connected software-defined era of auto chips should help sustain its valuation in the medium-term, despite the threat of a recession impacting consumer discretionary spending in the auto market.

The company also highlighted that the value of its auto chips would continue to climb as they become more complex, relative to simpler microcontrollers in the past. Management highlighted in a recent December conference:

So with the acceleration of content and with the fact also that electrification drives digitalization, and we have seen that trend very powerfully in the last 2 or 3 years. We actually see that those 2 trends are positive and additive. So yes, more processes per car. A smart actuator, simple microcontroller would probably be in the kind of $5 to $10 kind of range, a zonal controller then moves you to the $10 to $20 range. Domain controller, start to be firmly into the $20, $25 range. And then when we go to software-defined vehicles, then you easily talk about double, and in the kind of $50 range. So the opportunity that we see is increasing both in terms of ASP as well as in terms of units. (dbAccess AutoTech Conference)

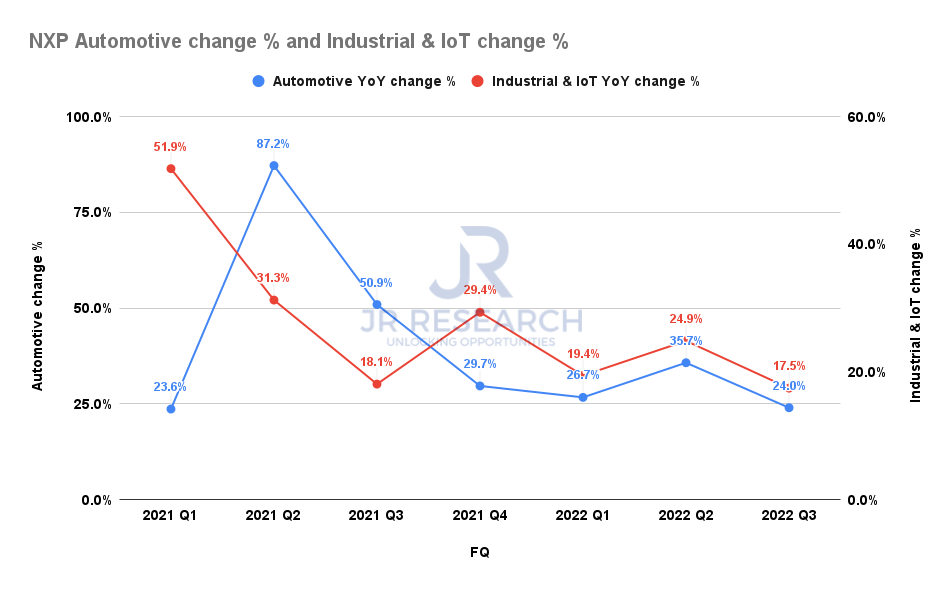

NXPI Auto revenue change % and Industrial revenue change % (Company filings)

Therefore, the company’s competitive advantage in its automotive processes has helped to maintain its growth momentum through Q3, but it could slow further.

Keen investors should recall that its Auto and Industrial segments revenue accounted for more than 73% of its Q3 revenue. Therefore, a broad macro slowdown impacting the automotive market could affect NXPI to maintain its growth momentum.

A recent DIGITIMES report updated that auto chip supply dynamics could stay tight in the near-term, despite the macro headwinds. As such, it should help mitigate a potential correction in the auto chips market moving forward.

The robust pipeline visibility from Qualcomm (QCOM) and Nvidia (NVDA) also corroborated the long-term growth underpinnings of the auto chips market. Notably, the auto chips market is still expected to post robust growth in the semi industry, given its immense potential.

The transition from traditional ICE vehicles to EVs is also still in its early stages, as it accounted for just 10% of global auto sales, suggesting significant potential for NXPI to leverage.

But, the critical question that NXPI investors might have is whether the correction in NXPI from its December 2021 highs is finally over?

NXPI price chart (weekly) (TradingView)

NXPI last traded at an NTM EBITDA of 10.2x, as it recovered from its October lows remarkably, up nearly 40%, outperforming the S&P 500 (SPX) (SPY). NXPI is also not expensive at its current valuation, trading below its 10Y average of 11.6x.

Therefore, astute investors who picked its October lows have been well-rewarded. Investors who missed those lows were given another solid opportunity in late December to add more exposure.

With NXPI closing in against its August highs, we believe that the bear market in NXPI is likely over.

Investors still sitting on the sidelines can consider getting ready to pounce at its next pullback as the market shakes off some late breakout traders/investors who chased the recent surge.

Rating: Hold (Reiterated, but on the watch for a rating change).

Be the first to comment