David Tran

The early-year market rally is showing no signs of stopping, and it’s a great time for investors to re-tilt their portfolios toward forgotten growth names that are ready to burst out of the gate again. In this regard look no further than Splunk (NASDAQ:SPLK), a big data software company that specializes in mining companies’ internal machine data in order to generate insights.

Splunk spent much of the past two years in transition mode. It was late to the subscription game, and just recently started moving over its customers onto recurring subscription contracts instead of perpetual licenses. As expected, the company took a near-term growth hit during this transition and profitability metrics also started fraying. But now emerging from this subscription transition with tremendous growth rates in both revenue and ARR, and with the market ready to bet on growth again, Splunk is an excellent choice for a rebound play.

I remain bullish on Splunk as a core holding in my portfolio. I have long favored technology companies with broad, open-ended platforms serving countless use cases and horizontal applicability to all industries. Splunk has emerged from its two-year transition as an incredibly margin-rich company as well, which will be a major draw in a relatively more risk-averse market that has started paying more attention to tech companies’ bottom lines.

Here is my full bull thesis for Splunk:

-

The use cases for Splunk are infinite. In its early days, Splunk’s machine data-mining capabilities were often used for security purposes to flag and respond to anomalies within corporate systems. But as Splunk has evolved, the company’s machine data capabilities are applicable across virtually any industry and across many functions.

-

Usage-based pricing. Some of the most successful software stocks are usage-based, meaning that revenue climbs proportionally to a customer’s usage of the product. Splunk’s platform is charged on a data volumes/computing power basis. As data volumes continue to explode and companies push the boundaries of how they integrate data into operations and decision-making, Splunk has a tremendous opportunity to derive growth from within its install base.

-

Splunk isn’t without competitors, but the company’s focus on machine data is unique. It’s also the largest company in the space. The company’s closest large/public peers are the monitoring companies like Datadog (DDOG) and New Relic (NEWR), which primarily focus on monitoring the performance and uptime of applications and infrastructure. Splunk focuses on visualizing and analyzing machine data (information passively generated by computers, phones, and other endpoints within networks). We note as well that Splunk’s ~$3.7 billion annual revenue scale makes it twice as large as its next-closest competitor, Datadog.

-

Industry-wide recognition – More to the point above, it’s fine to have competition when Splunk also is widely considered the best-in-breed vendor for machine data analytics. Gartner, the software industry’s leading analyst and reviewer, has bestowed the “Leader” designation to Splunk in the security information and event management space, and also named it as the vendor with the highest ability to execute. These commendations don’t come lightly to IT buyers when making a purchase decision.

-

Significant international expansion opportunity – Splunk has become a global brand name, and it’s time for Splunk to chase more opportunities overseas. Currently, only about ~35% of its revenue base comes from international markets (and an even smaller ~20% slice of the cloud business is overseas). I see significant opportunity for Splunk to expand its presence outside of the U.S.

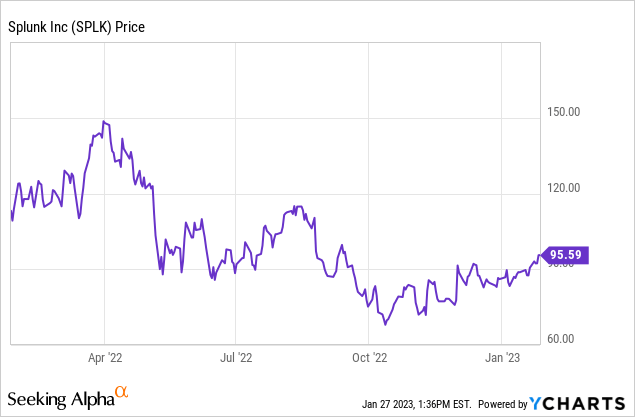

In spite of all these strengths, Splunk’s rather muted price appreciation during its subscription transition has left its valuation metrics quite sparse. At current share prices near $95, Splunk trades at a market cap of $15.60 billion. After we net off the $1.80 billion of cash and $3.87 billion of debt on Splunk’s most recent balance sheet, the company’s resulting enterprise value is $17.67 billion.

For next fiscal year FY24 (the fiscal year for Splunk ending in January 2024), meanwhile, Wall Street analysts have a consensus revenue target of $4.03 billion for the company, representing 16% y/y growth (data from Yahoo Finance). This puts Splunk’s valuation at just 4.4x EV/FY24 revenue, which to me is quite low for a company with 80%+ pro forma gross margins and current revenue growth rates in the ~40% range.

Stay long here, there’s plenty of upside to go.

Recent trends showcase boosts in revenue and profitability

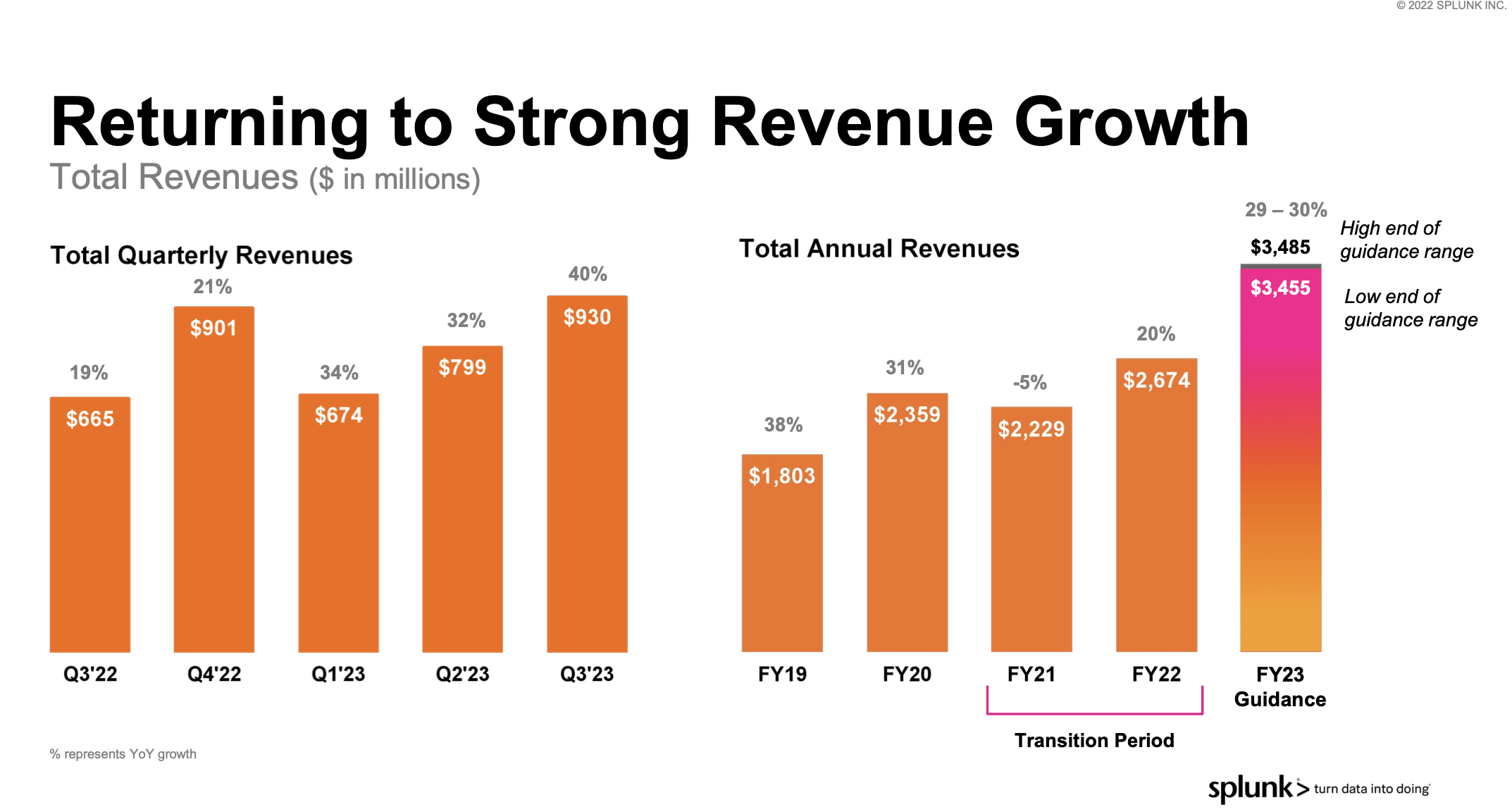

It took a lot of patience as Splunk fine-tuned its business model transition, but now we’re here to reap the rewards. The company posted excellent fiscal Q3 results:

Splunk Q3 results (Splunk Q3 earnings deck)

Revenue grew 40% y/y to $929.8 million, which handsomely beat Wall Street’s expectations of $836.3 million (+26% y/y) by a huge fourteen-point margin. And as shown in the chart below, revenue growth accelerated sharply from 32% y/y growth in Q2. The right-hand side of the snapshot below also shows how growth has materially skyrocketed since the days of Splunk’s subscription transition.

Splunk top-line momentum (Splunk Q3 earnings deck)

The company noted that cloud migration remained strong, though major headwinds have made some customers exert some caution. Per CEO Gary Steele’s remarks on the Q3 earnings call:

Our top line outperformance was driven by strong term license demand from existing customers, underscoring the value our customers continue to gain from Splunk’s mission-critical security and observability solutions powered by our one-of-a-kind data platform. That said, as noted last quarter, we continue to see caution from customers on the timing of their cloud migrations and expansions setting ongoing macro concerns.”

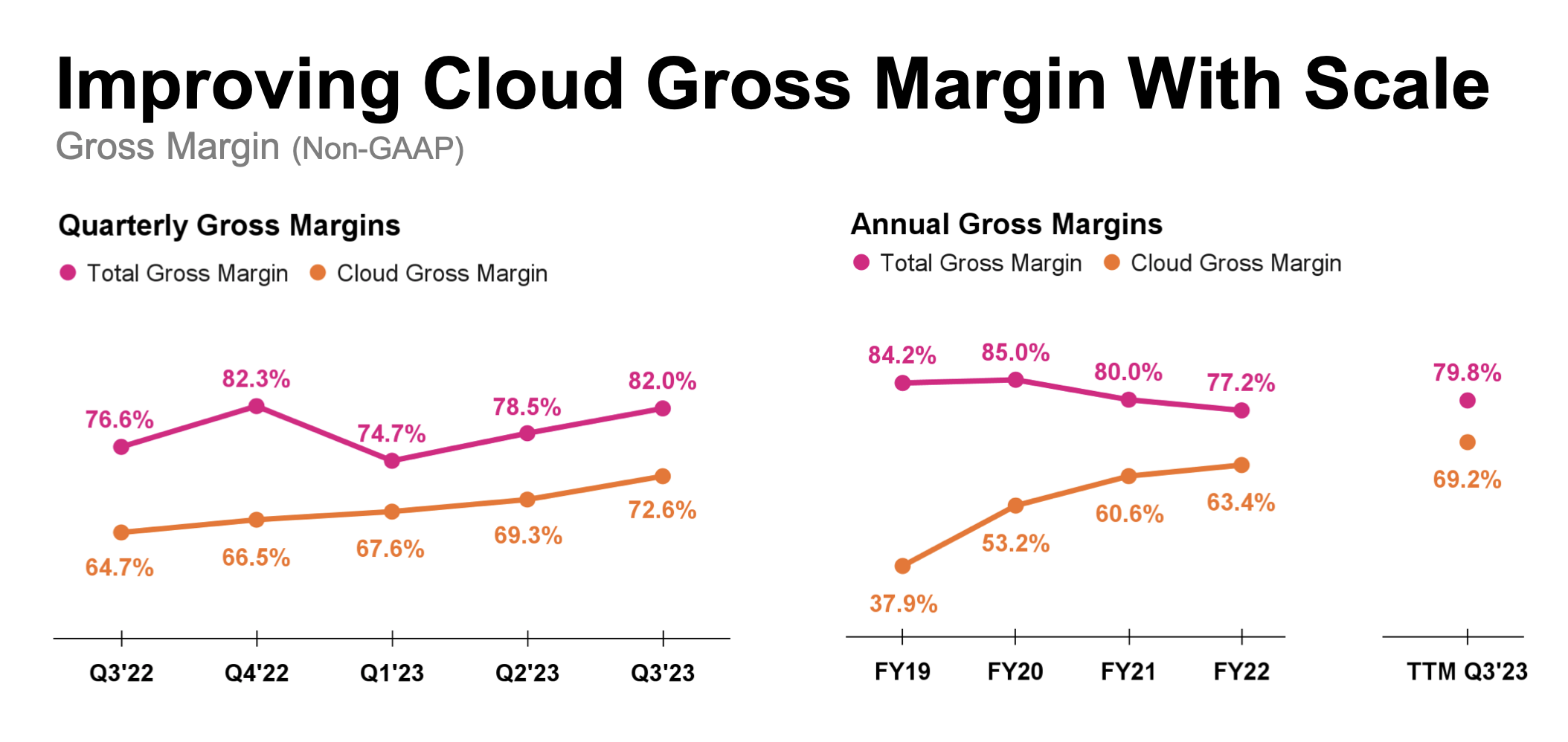

Splunk also displayed excellent profitability results. Pro forma grow margins rose to a sky-high 72.6%, up 330bps sequentially and an increase of nearly eight points year over year:

Splunk margins (Splunk Q3 earnings deck)

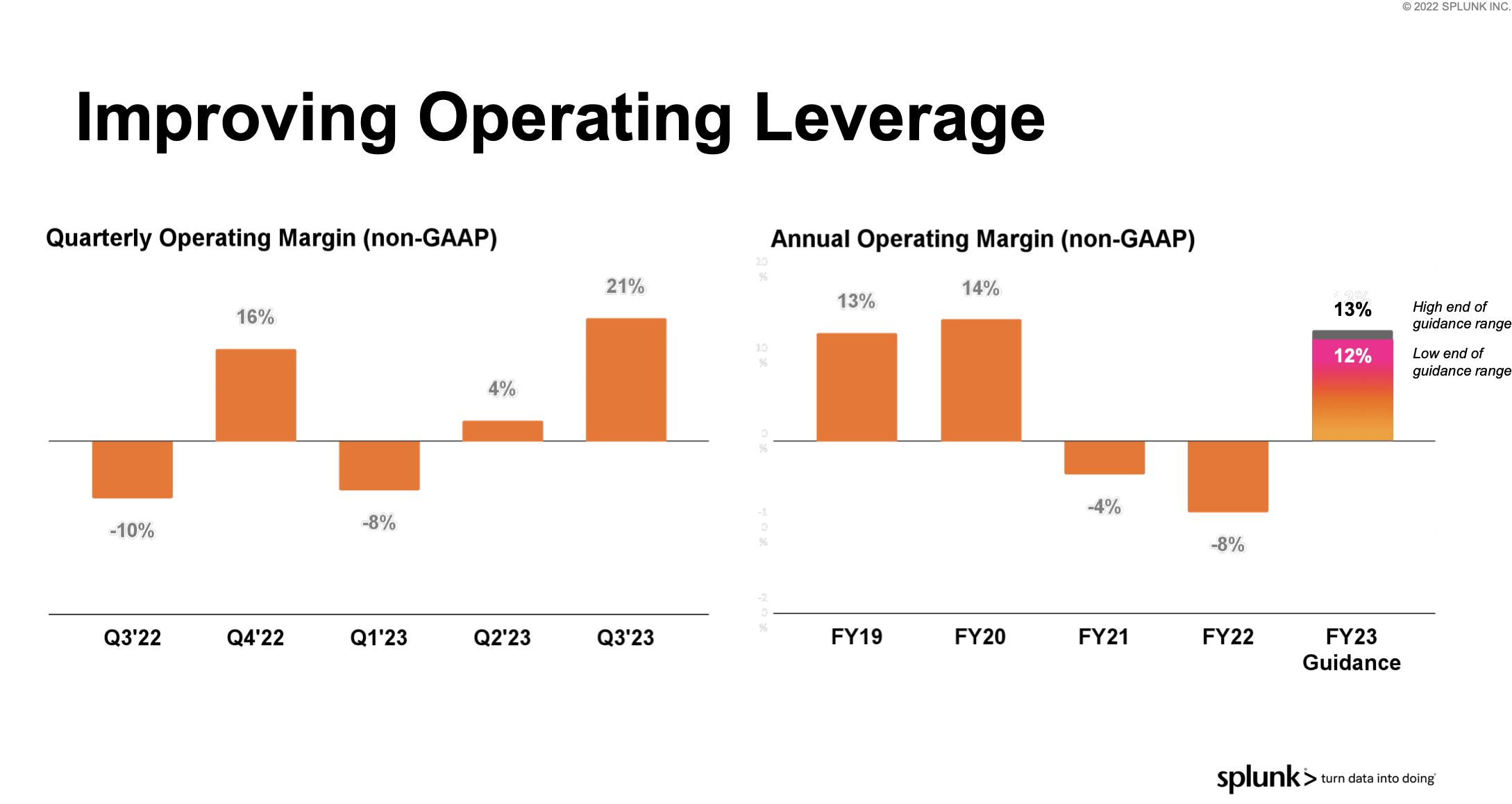

This was driven by ongoing optimization efforts with the company’s infrastructure delivery partners. In addition to gross margin boosts, Splunk also managed to exhibit extreme opex discipline, slowing down hiring, shrinking its real estate footprint, and reducing travel and entertainment to bare essentials. As a result of these actions, the company out $30 million out of its opex relative to Q2, and reduced opex by 2% y/y. With both operating leverage plus gross margin gains, the company managed to boost pro forma operating margins to 21%: more than thirty points of gain since the prior year.

Splunk operating margins (Splunk Q3 earnings deck)

Key takeaways

Rich profitability, a resurgence in growth driven by a now nearly pure recurring-revenue business, net revenue expansion rates in the ~130% range, and a wide-open $100 billion TAM to grow into – these are all of the key reasons to stay long on Splunk. Continue to bank on this stock for upward momentum.

Be the first to comment