imaginima

Vitesse Energy (NYSE:VTS) is a company that through a spin-off from Jefferies (JEF) came into existence in mid-January this year. Often spin-offs can provide great and quick revaluation opportunities and come across as unequivocally undervalued. While the multiple that gets proposed for VTS is great, we don’t suspect the valuation is that compelling. Besides using some precedent transactions, which are admittedly a little dicey, even just on a review of peer multiples and considering the relatively low quality assets and breakeven points, there’s not an especially strong reason to buy. There are equally cheap and safer oil assets out there.

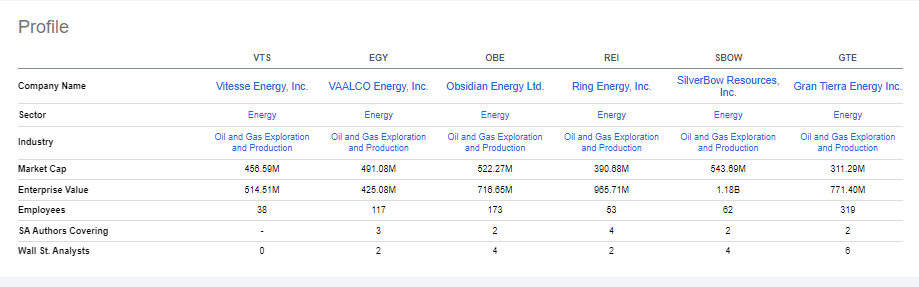

VTS Key Facts

It has interests in acreage on the Williston Basin, and this is probably the worst shale basin in the US. The IRRs are barely high enough to justify investment at current prices, and the breakevens are higher than almost anywhere else, so there’s some risk of non-profitability if the oil cycle phases forward. Run rate breakevens for existing wells are probably around $40 per barrel, and efficient investment is closer to $70 which is barely below the current prices. These are slightly dated figures, but there’s no reason to expect they’re lower now, especially as inflation raises the nominal CAPEX burden. Moreover, VTS has relatively low leverage at a 0.4x net debt to EBITDA multiple, so they’re developing closer to the unlevered IRRs that benchmark returns at the different basins. Higher financing costs aren’t going to help them much in getting away from those pretty low unlevered figures, considering the commodity risk in oil assets.

Since a lot of its acreage is not yet operated, around 70% of it based on how many more net wells management thinks can be developed, the economics of new wells are more important than the run-rate economics, and currently the IRRs are going to be only a little higher compared to project finance benchmarks in oil & gas.

Valuation

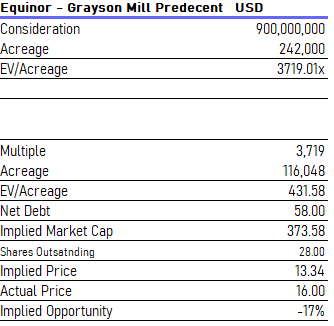

The Williston Basin really is the worst, but if we start comparing it with peers in the segment using SA’s valuation tools, we see that it doesn’t particularly stand up.

VTS Peers (Seeking Alpha)

The peers are usually trading between a 3x and 4x PE, while Vitesse lies at around 5x. So without deserving a premium it looks a little expensive.

We can also use precedents, although at a time when oil supply was structurally higher before Russia invaded Ukraine, to value VTS (oil prices were still similar in February 2021). If we scale the working + un-operated acreage based on the expected total well development figures from VTS, and use a multiple from the precedent of the Equinor (EQNR) transaction to value the company based on an EV/Acreage multiple, we get the following results.

Precedent Transaction Valuation (VTS)

This lines up closely with the peer analysis in terms of the upside.

Bottom Line

There are commodity risks when buying shale assets. A lot of operating leverage and a pretty high breakeven make for a dangerous combination. While the oil price is being supported by structural factors including the reignition of China and better than expected inflation data in the US, oil is still cyclical and the discretionary supply from OPEC could move things around a lot – although game theory does tell us that the Saudis will prefer to keep prices high rather than low, even just to stick it to the US.

The reinvestment economics are not so great at Williston, and when you can get Norwegian Continental Shelf assets at a similar price, it seems obvious to opt for those assets instead.

However, we should mention that management proposes a hefty dividend at $66 million annually as of their investor presentation in November 2022. So yield chasers who want a 15% dividend yield may choose VTS on that basis. It does say something about the low multiple valuations after all, but it may not be as sustainable, and there’s even a potential gutshot that could come from politicians that may limit dividend payouts from oil & gas companies given the politics around green energy and the discipline producers are maintaining around shale.

Ultimately, not super compelling.

Be the first to comment