Evgenii Mitroshin

Laredo Petroleum has rebranded itself as Vital Energy, Inc. (NYSE:VTLE), not to be confused with the Western Canadian junior oil and gas company with the same name. In that January 8, 2023 press release, it reported Q4 2022 production that was above its expectations from its revised Q4 guidance as of Q3 2022, although production was also at the lower end of its original Q4 guidance from Q2 2022.

Vital does have some challenges with low natural gas prices, as despite its hedges it may barely realize (including hedges) over $1 per Mcf for its natural gas in 2023 at current strip. Around 28% of Vital’s production was natural gas in Q3 2022. With the current strip for oil in the low-$80s, though, Vital should still be able to reduce its net debt to around $0.95 billion by the end of 2023.

I estimate that Vital is worth approximately $74 per share in a long-term (after 2023) $70 WTI oil and $4.00 NYMEX gas scenario, assuming that it can realize $2 per Mcf for its natural gas in that long-term scenario.

Q4 2022 Results

Vital provided a positive update on its Q4 2022 results. It noted that oil production averaged approximately 35,500 barrels per day, 4% above the high-end of its guidance range and 8% above the midpoint of its guidance range for 32,000 to 34,000 barrels of oil production per day.

As well, Vital’s total production of approximately 77,500 BOEPD was also above the high end (by approximately 3%) of its guidance range of 72,500 to 75,500 BOEPD. Vital’s oil cut ended up at around 46% in Q4 2022, slightly above expectations for a 45% oil cut.

Vital achieved these results without spending above its recent capex guidance for $135 million to $145 million during the quarter.

Vital’s Q4 2022 results were at the low end of its earlier guidance for 35,500 to 37,500 barrels of oil production per day and 77,500 to 80,500 BOEPD in total production for Q4 2022. Vital revised its Q4 2022 guidance in early November to reflect its expectations for significant negative production impacts from offset operator completions. It thus appears that the impact of offset frac-hits wasn’t as bad as Vital expected. The oil production trajectory of Vital’s Leech wells has also improved, and it is now at around 50% of Vital’s Central Howard average (from Q2 2021 onward) compared to 30% in August.

Notes On Natural Gas Prices

Low realized prices for natural gas may present a challenge for Vital in 2023. Natural gas still accounted for 28% of Vital’s production in Q3 2022 despite its focus on drilling oilier inventory. This is still down a fair bit from the 35% of Vital’s total production that natural gas represented in Q3 2019 though.

Vital expected to realize approximately $1 less than Waha for its natural gas in 2022. With the Waha basis averaging around negative $2 to NYMEX though for 2023, and NYMEX strip averaging around $3.50 for 2023, this means that Vital could only realize around $0.50 for its natural gas in 2023 before the impact of hedges.

Vital does have Waha basis hedges and natural gas collars covering around 54% of its projected natural gas production in 2023, but even with the hedging, Vital may only realize slightly above $1 per Mcf for its natural gas in 2023.

2023 Outlook

I have modeled a scenario where Vital averages 79,500 BOEPD in total production and 36,000 barrels per day of oil production in 2023. At the current low-$80s WTI strip and $3.50 NYMEX gas, Vital is projected to generate $1.289 billion in revenues, inclusive of $25 million in positive hedge value.

| Barrels/Mcf | $ Per Barrel/Mcf (Realized) | $ Million | |

| Oil | 13,140,000 | $82.00 | $1,077 |

| NGLs | 7,938,750 | $20.50 | $163 |

| Natural Gas | 47,632,500 | $0.50 | $24 |

| Hedge Value | $25 | ||

| Total Revenue | $1,289 |

With a $650 million capital expenditure budget, this would result in Vital generating $144 million in positive cash flow in 2023 at current strip. This does not include any further interest savings from potential note repurchases.

| $ Million | |

| Lease Operating Expense | $181 |

| Production and Ad Valorem Taxes | $92 |

| Marketing and Transportation | $52 |

| Cash G&A | $70 |

| Interest | $100 |

| Capital Expenditures | $650 |

| Total Expenses | $1,145 |

Notes On Debt And Valuation

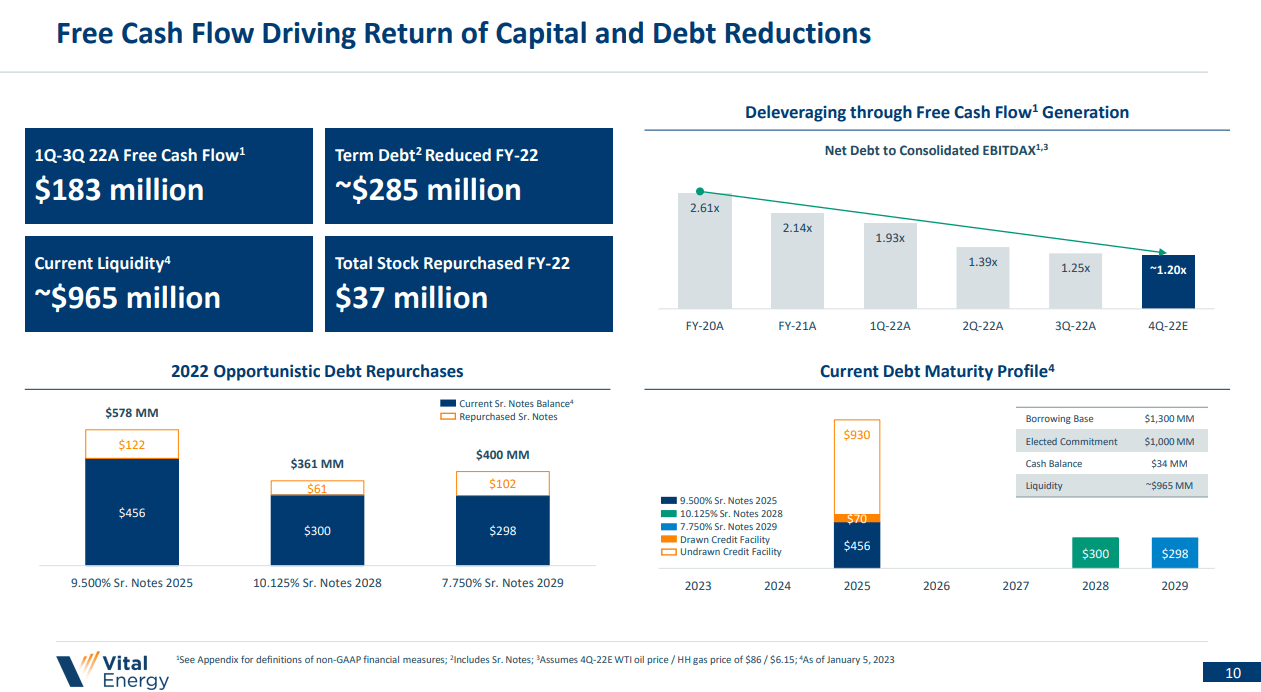

Vital reduced its net debt to $1.09 billion as of January 5, 2023 and it repurchased $285 million of its high-interest notes during 2022, resulting in significant interest savings. Vital has also managed to reduce its leverage to around 1.2x

Vital’s Debt Maturities (vitalenergy.com)

At current strip, Vital is projected to end 2023 with approximately $0.946 billion in net debt if it doesn’t repurchase more shares or notes. Vital’s leverage at the end of 2023 would be 1.1x in this scenario.

I now estimate that Vital is worth approximately $74 per share in a long-term (after 2023) $70 WTI oil and $4.00 NYMEX gas scenario. This is based on a 2.8x EV to EBITDAX multiple and 2023 production levels along with its projected year-end 2023 net debt. It also assumes that in the long-term Vital can realize approximately $2 for its natural gas at $4 NYMEX.

Conclusion

Vital Energy, Inc. is projected to reduce its net debt to under $950 million by the end of 2023 at current strip. It may realize a very minimal amount for its natural gas in 2023 due to Waha trading at a large discount to NYMEX. However, the impact of this is currently mitigated by low-$80s WTI oil, which is a price that works okay for Vital.

Vital Energy, Inc. does have some risks in that $60s WTI oil plus continued large natural gas differentials could lead it to generate essentially zero free cash flow in 2023. Vital Energy, Inc. does also have a fair bit of upside if it can continue paying down its debt, though, which it can do at current strip.

Be the first to comment