Patrickistock/iStock Editorial via Getty Images

Compagnie Financière Richemont (OTCPK:CFRHF) (OTCPK:CFRUY) just released its nine-month results. Here at the Lab, we were not very optimistic about the company’s future development and our main concerns were due to 1) the governance controversy with the British activist fund called Bluebell Capital Partners, 2) Richemont’s e-commerce strategy that leads to the impairment of a total consideration of €2.7 billion and 3) lower Swiss watch exports combined with negative growth in Asia Pacific (APAC) sales developments.

Starting with the negative news, and following the company’s release in August, YNAP’s accounts will be reported as ‘discontinued operations’. So, our internal team has made some adjustments in Richemont’s sales split to report on a comparable basis to the company’s sales division.

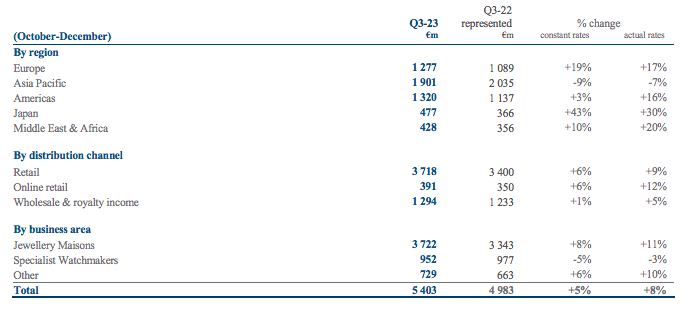

Having recently looked at Burberry numbers, Richemont also reported a negative trend in China. In addition, the luxury giant failed to meet Wall Street analyst consensus expectations on the revenue line. In Q3, looking at the details, the company reported top-line sales up by 8% to €5.4 billion, but below the €5.7 billion forecasted by equity research analyst consensus average. This was due not only to the Chinese sales trend that on a yearly basis delivered a -24% but also to the US slowdown. Despite the good performance due to the out-of-town tourism flow, the US revenues were up by +3% compared to an average forecast of +8%.

Compagnie Financière Richemont sales by Region, Channel and Business Area

Source: Compagnie Financière Richemont Q3 results

Regarding the company’s division, slightly below expectations was the jewelry segment (+8% versus implied numbers at +10%). More important to note and in line with Mare Evidence Lab’s previous indication was the watch division which reported negative results that fell by 5% on a yearly basis versus a forecast of +8%. In the division, retail sales outpaced the wholesale segment due to the double-digit decline in Asia-Pacific which significantly impacted the double-digit growth in Europe and Japan.

What is key to emphasize is the fact that Richemont expressed a strong rebound in sales ahead of the Chinese New Year. After the COVID-19 wave peaks in the country’s major cities, stores are reopening and customer numbers are increasing with retail sales that are reporting a sharp rebound. The group appeared confident and left its yearly target unchanged.

Conclusion and Valuation

With the latest development and updating our internal numbers, here at the Lab, we forecasted a total top-line sales of €19.6 billion for the full year, with a plus +12% at constant exchange rates, and an operating profit at €4.80 billion (signaling again a plus 28%). The company is clearly demonstrating important operating leverage. Ignoring the mixed above results on consensus, investors seemed to focus on the optimistic outlook that China’s reopening suggests. In particular, China’s acceleration will likely be supported by savings made during COVID-19 confinements. Important to note is also Richemont group’s net cash position that stood at €5.5 billion and is up by €0.6 billion thanks to a solid FCF generation. Despite that, in 2022, Richemont has underperformed the sector by almost 12%, and based on the latest accounts, there is a 20% P/E discount compared to the luxury peers on the 2023-2024 expected numbers. The company is currently trading at an estimated 2023 P/E of 20x versus a historical average of 27x. Therefore, we decide to increase our target price to CHF 150, confirming our neutral rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment