Adrian Vidal/iStock via Getty Images

Investment Thesis

The Vanguard International Dividend Appreciation ETF (NASDAQ:VIGI) is an international dividend ETF. The fund offers exposure to a basket of hundreds of high-quality dividend-paying securities around the world.

Dividend ETFs are a common source of revenue for investors looking for a steady flow of cash. They are also typically less volatile than the market because a dividend indicates that a company is financially healthy and is therefore perceived as less risky by market participants. VIGI is not a high-yield investment and it is carefully avoiding dividend traps, which makes it one of the most reliable dividend ETFs.

That said, I believe many VIGI components are now overvalued. While I have no doubt that these are high-quality firms, the current valuation can prove to be a drag on VIGI’s future returns.

Strategy Details

The Vanguard International Dividend Appreciation ETF tracks the investment results of the S&P Global Ex-U.S. Dividend Growers Index. The fund is made up of large-cap equities from developed and emerging economies, excluding the United States, that have both the ability and the commitment to grow their dividends over time.

If you want to learn more about the strategy, please click here.

Portfolio Composition

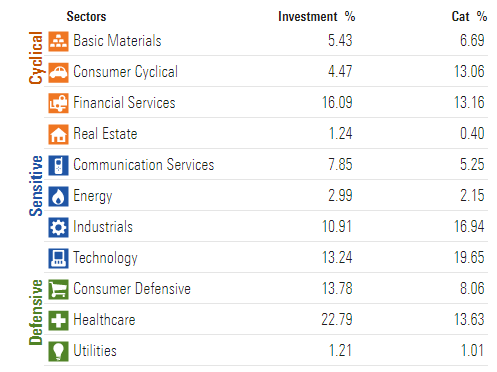

VIGI invests nearly 23% in the Healthcare sector, followed by Financials (accounting for ~16%), and Consumer Defensive stocks (accounting for ~14% of total assets). The top 3 sectors have a combined allocation of ~53%. Unsurprisingly, a number of cyclical sectors such as Real Estate, Consumer Cyclical, and Basic Materials have a low weight given their track record of irregular dividends. However, I am surprised to see a ~13% allocation to Technology given the fact that tech companies generally tend to reinvest profits into the business for future growth.

Morningstar

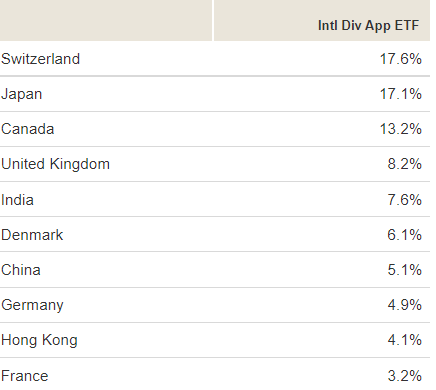

In terms of geographical allocation, VIGI invests over 17% in Switzerland, followed by Japan (~17.1%) and Canada (~13.2%). The top three countries account for ~48% of total assets. VIGI overweights developed markets like Switzerland and Japan, whereas emerging markets seem to be underrepresented.

Vanguard

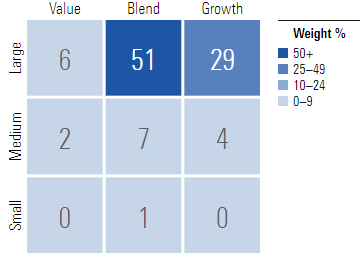

Half of the portfolio is allocated to large-cap blend issuers, characterized as large-sized companies where neither growth nor value characteristics predominate. Large-cap issuers are generally defined as companies with a market capitalization above $10 billion. VIGI allocates only 14% of funds to small and mid-cap stocks, likely leading to lower volatility compared to other dividend strategies that have a higher allocation to these two categories.

Morningstar

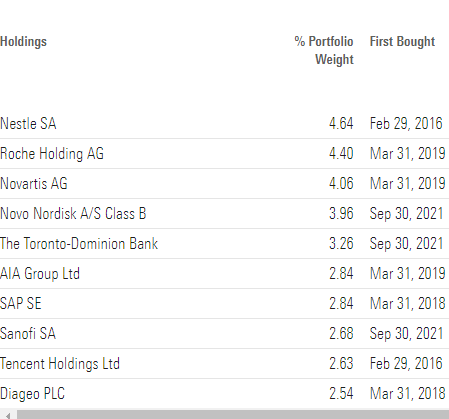

VIGI is currently invested in 349 different stocks. The top 10 holdings account for nearly 34% of the portfolio, with no single stock weighting more than 5%. Despite the significant percentage invested into the top 10 holdings, I believe VIGI is well-diversified considering its vast number of constituents.

Morningstar

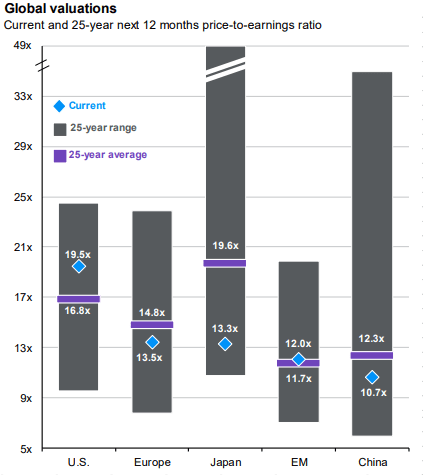

Since we are dealing with equities, one important characteristic is the portfolio’s valuation. According to data from Vanguard, VIGI trades at a price-to-book ratio of ~3 and an average price-to-earnings ratio of ~19. If we compare the fund’s price-to-earnings ratio to other developed and emerging markets around the globe, VIGI appears to be overvalued. Europe and Japan for instance are trading at ~13x earnings, whereas emerging markets are trading at ~12x earnings. That said, VIGI has high-quality constituents. The average return on equity for the portfolio is 18.3% and the historical EPS growth rate stands at ~12%. The mix of quality and high EPS growth might explain why the market is ready to pay a premium for this ETF.

JPM Guide to the Markets Q2 2022

Is This ETF Right for Me?

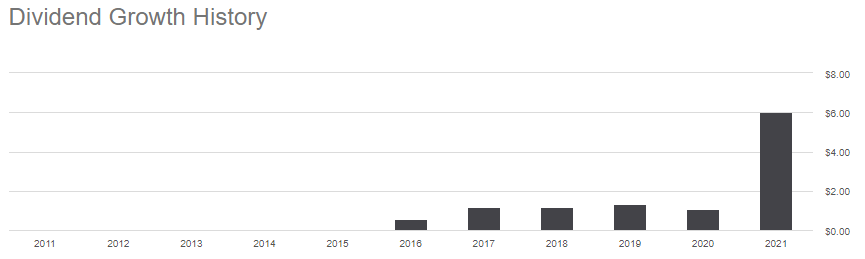

Dividend investors like VIGI because it owns a basket of quality dividend-paying stocks. In 2021, VIGI paid a $0.81 dividend per share, excluding the $5.18 in short and long-term capital gains returned to shareholders in December. The 2021 dividend amount is therefore slightly lower than in previous years. At the current share price of $79, the TTM dividend yield (excluding capital gains) stands at ~1%. I personally consider the yield too low for a dividend investor, but I like the fact that the strategy is capable of returning large amounts of capital gains.

Seeking Alpha

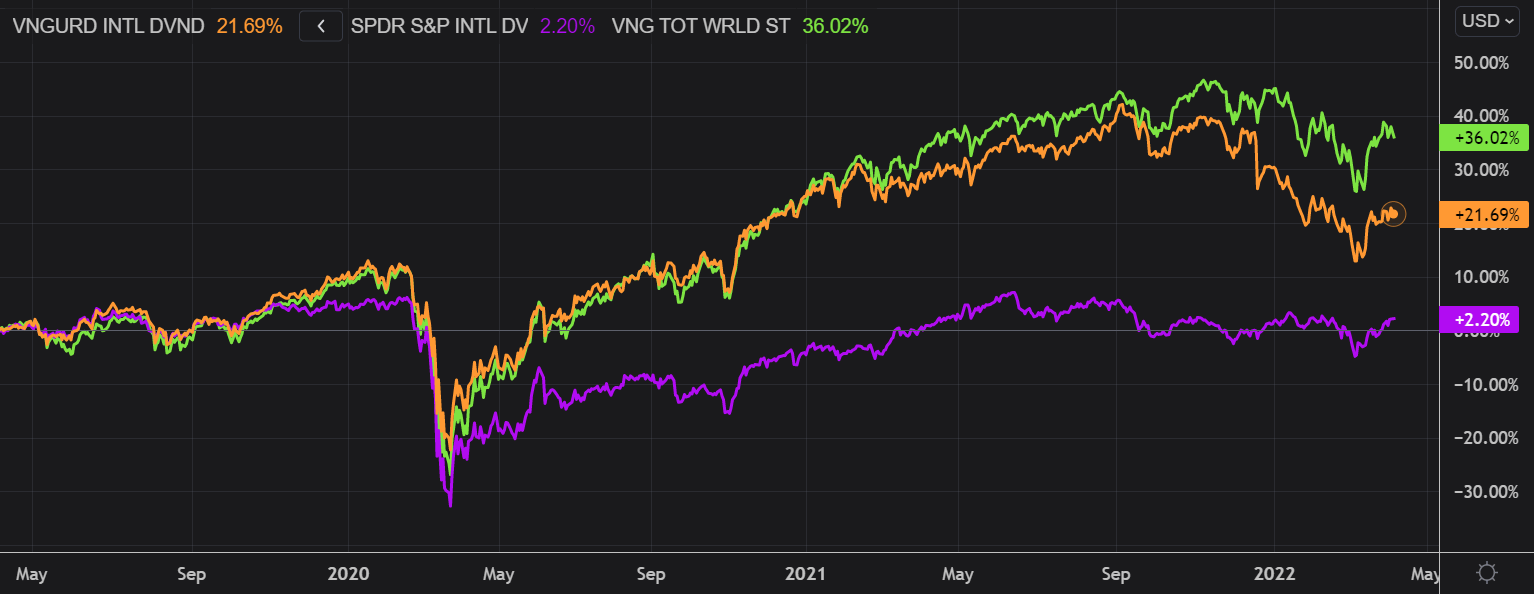

I have compared below VIGI’s price performance against the SPDR S&P International Dividend ETF (DWX) and the Vanguard Total World Stock ETF (VT) over the last 5 years to assess which one was a better investment. Over that period, VIGI outperformed DWX but failed to beat VT. It is interesting to see that both VIGI and DWX delivered similar returns up until Q4 2019, when the performance spread widened and DWX started to underperform. In my opinion, the sector allocation was a drag for DWX since it invests over 25% of total assets into utilities, which tend to pay higher dividends but deliver mediocre price returns.

To put VIGI’s performance into perspective, a $100 investment 3 years ago in this ETF would now be worth ~$121.69. This represents a compound annual growth rate of ~6.8%, excluding dividends, which is an average absolute return.

Refinitiv Eikon

If we take a step back and look at the performance from a six-year perspective, the results don’t change much. Both VIGI and VT came on top once again, outperforming DWX since mid-2017.

I personally believe many constituents are richly valued at the moment, which could prove to be a drag on VIGI’s future returns. While I have no doubts that these are high-quality businesses, I believe valuation will become more and more important over the coming months for market participants. This can turn out to be a risk factor for VIGI.

Refinitiv Eikon

Key Takeaways

VIGI provides exposure to a basket of high-quality dividend-paying international equities. The fund is well-diversified both across sectors and issuers. I personally believe VIGI’s dividend yield doesn’t compensate investors adequately for the risks involved, but I like the fact that the strategy is capable of generating important capital gains for shareholders. In terms of valuation, VIGI is more expensive than some peers, which adds some risks to the bullish thesis in a rising interest rate environment.

Be the first to comment