Lurin

Over the past months, real estate investment trusts (“REITs”) (VNQ) have dropped heavily. As a result, they are now priced at steep discounts to pre-Covid-19 levels. This is especially surprising since real estate has experienced significant appreciation since then.

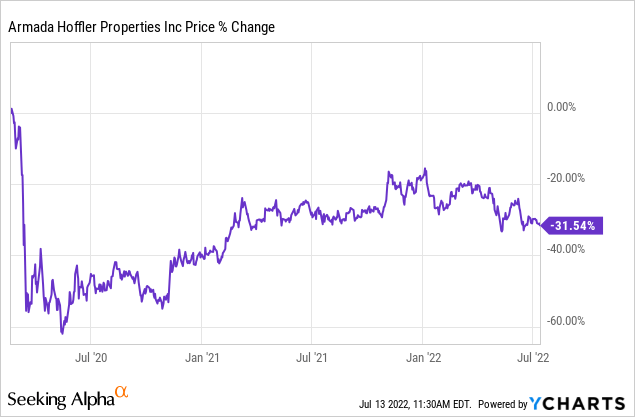

A good example is Armada Hoffler Properties, Inc. (NYSE:AHH), one of our Top Picks at High Yield Landlord. It is currently priced at a 31% discount to pre-Covid-19 levels, and yet, it is objectively more valuable than ever before:

It is objectively more valuable than ever before because it owns high-quality properties that have grown their net operating income (“NOI”) and also experienced cap rate compression. The higher the NOI, and the lower the cap rate, the higher the property value.

Example: a property that generates $100,000 is worth $1,000,000 at a 10% cap rate, but it is worth $2,000,000 at a 5% cap rate ($100,000/0.05). If the NOI rises to $110,000, and you use a 5% cap rate, the value becomes $2,200,000.

About half of AHH’s properties are multifamily communities (as measured by NAV), and those have experienced significant cap rate compression and are expected to grow same property NOI by 10% in 2022 alone. The rest of its properties are mainly service-oriented retail properties and Class A office buildings that are also growing in value, but at a somewhat slower pace.

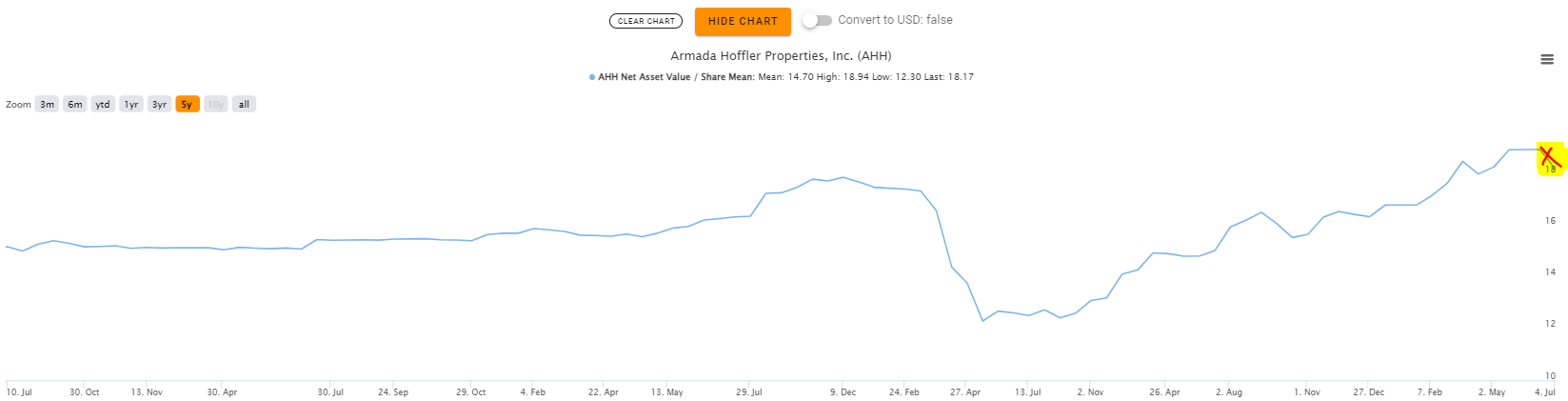

So, there is no question that AHH is today much more valuable than it was before the pandemic. The consensus estimate of analysts is that AHH’s net asset value per share reached a new all-time high of $19 in June:

TIKR

Yet, the current share price is around $12, representing a hefty 30% discount.

Why Is The Market Discounting AHH So Heavily?

We think that investors fear that AHH may struggle to finance its many development projects now that its equity is discounted, and interest rates are on the rise. If the cost of capital surges too high, these development projects may suddenly turn dilutive to shareholder value.

But here comes the very good news:

AHH just proved to the market that it can access very cheap equity by selling some of its retail properties at historically low cap rates.

It just announced the sale of two retail properties leased to Costco (COST) and Home Depot (HD) at a 4% cap rate. The management then reaffirmed that they will keep doing similar deals to self-fund their development projects (emphasis added):

“As we discussed earlier this year, selling assets in the low to mid 4% cap range represents the most cost-effective funds available to us and should have little, if any, impact on earnings. More importantly, this disposition, along with others pending, allow us to self-fund our equity needs for the remainder of the year.”

This is great news, as it should remove or at least mitigate the primary concern of the market.

It appears that investors falsely think that AHH’s retail properties are risky, since retail is hated, and we may be headed into a recession.

But in reality, these are some of the most resilient real estate investments that exist. They are anchored by service- and value-oriented tenants such as Kroger (KR), Whole Foods (AMZN), and TJ Maxx (TJX). They enjoy long leases, high occupancy rates, and near double-digit releasing spreads:

Armada Hoffler

These properties are inflation- and recession-resistant and are in great demand from investors according to the management (emphasis added):

“Despite recent market volatility, investor demand for high credit, single-tenant, net leased assets with longer lease terms remains strong. After securing early long-term lease extensions with both tenants, we capitalized on this demand and successfully transacted at a price that far exceeded our expectations.”

In the coming quarters, we expect AHH to sell more of its retail properties at historically low cap rates, raising cheap equity, which it will then reinvest into higher-yielding multifamily development projects.

It will lead to strong FFO per share growth, but importantly, it will also lower its exposure to retail, all while increasing its exposure to multifamily real estate.

Today, apartment REITs trade at much higher FFO multiples than retail REITs and so this should be a further catalyst for the stock.

| Apartment REITs | Retail REITs | |

| Avg FFO Multiple | ~22x | ~11x |

Right now, you can still invest in AHH at just 12x FFO and an estimated 30% discount to NAV. That’s too cheap for a company with AHH’s growth prospects and the quality of its assets.

We believe that as AHH announces more similar deals and makes further progress with its development projects, its valuation multiple will expand closer to ~16x FFO, unlocking 30%+ upside to shareholders.

While you wait for the upside, you also earn a 5.4% dividend yield and the value of the company keeps on rising at a rapid pace. With nearly 10% FFO per share growth guided for 2022, AHH can deliver solid double-digit total returns for shareholders even without any multiple expansion.

That makes it a great investment opportunity following the recent dip. AHH should trade at a premium to pre-Covid-19 levels, but it is temporarily priced at a 30% discount, which likely won’t last much longer.

Be the first to comment