nantonov

What luck has gave you will probably leave you. – Amit Kalantri

Today, we put Vertex Energy, Inc. (NASDAQ:VTNR) in the spotlight for the first time. Vertex is a specialty refiner and marketer of high-quality refined products based in Houston with a market capitalization of approximately $620 million. This refining made a bold move to transform the company in May of 2021 when it announced it was purchasing the Mobile refinery in Alabama (90,000 bpd capacity) from Royal Dutch Shell (RDS.A) for $75 million with the goal of becoming become a leading regional supplier of both renewable and conventional products. The deal officially closed on April 1st of this year.

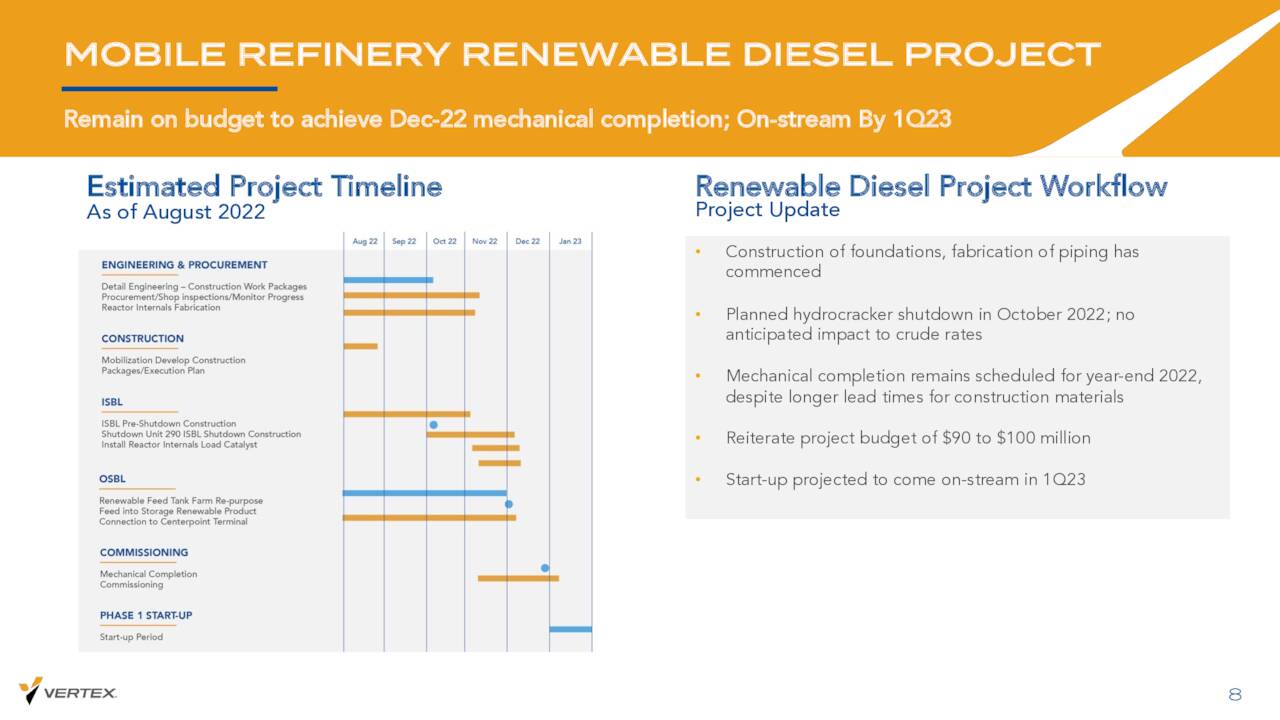

Management also said at the time it would spend an additional $85 million for the conversion of Mobile’s hydrocracking unit which scheduled completion by yearend 2022. The current estimated costs of that conversion are now in the $90 million to $100 million range. The scheduled completion date of this facility to produce renewable diesel fuel is roughly the same, with start up now projected for the first quarter of next year.

August Company Presentation

To help financed this effort the company announced it would sell its 69M gal/year Marrero used oil refinery in Louisiana and the 20M gal/year Heartland used oil refinery in Ohio as well as other assets of its used motor oil collection and re-refinery business to Clean Harbors’ (CLH) Safety-Kleen subsidiary for $140 million in cash one month later.

These assets would have generated more than $100 million in annual revenues for Safety-Kleen. At the time of the Mobile refinery acquisition, management stated once the conversion was completed it would give that facility the capacity to potentially generate at least $3 billion in revenue and $400 million in annual gross profit.

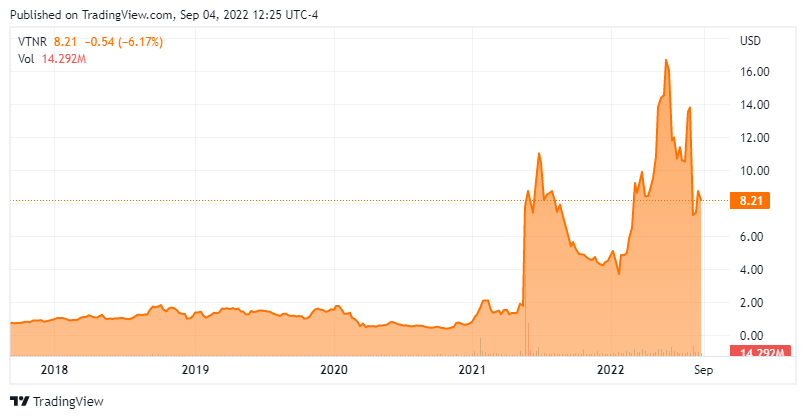

Unfortunately the Safety-Kleen deal fell through in late January of this year following regulatory review with the U.S. Federal Trade Commission. A few weeks later the company announced a five-year product supply agreement with California-based Idemitsu Apollo Renewable for 100% of renewable diesel produced as the soon to be completed conversion. Vertex’s management stated it expected to generate $6 billion in revenues over the life of the contract. All of this ‘news flow‘ has resulted in a very volatile five quarters for the company’s stock and shareholders.

Seeking Alpha

Second Quarter Results:

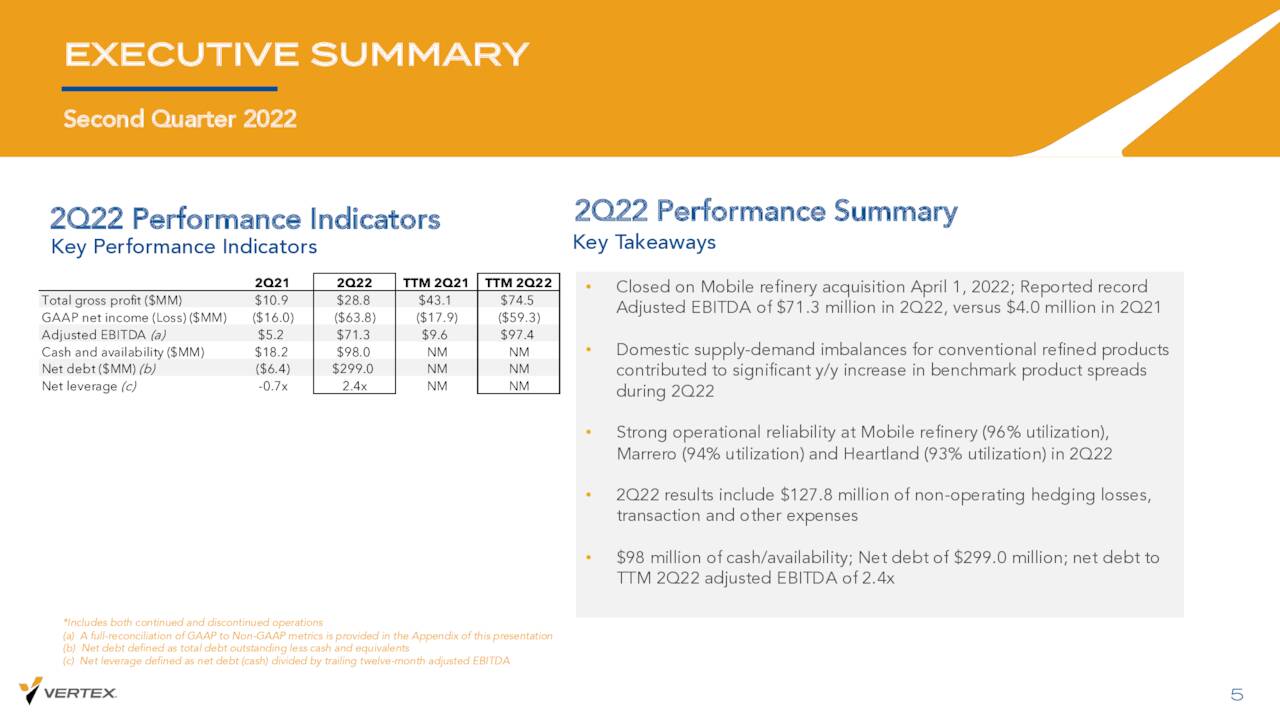

On August 9th, the company reported second quarter numbers. Vertex disclosed a GAAP net loss of 98 cents a share, more than two bucks a share worse than expectations.

August Company Presentation

There were several items that made up all and more of the $63.8 million net loss for the quarter including a $46.9 unrealized commodity derivative loss, a $23.2 million loss on an intermediation agreement due to backwardation, and a $46.1 million realized commodity derivatives loss. The company had this to say about the Vertex’s hedging program within its second quarter earnings press release:

Earlier this year, we entered into an inventory hedging program designed to mitigate financial risk, while positioning us to generate ratable cash flows with which to support our business for the first six months during the transition period. This program worked as planned during the second quarter, ensuring a ratable stream of cash flow into the business during a period of significant, planned capital investments. However, given expectations for a continued tightening in product supply and strength in refined product margins over the near-to-medium term, we intend to close out our remaining hedges in the third quarter, while maximizing our spot market exposure beginning in the fourth quarter 2022.

August Company Presentation

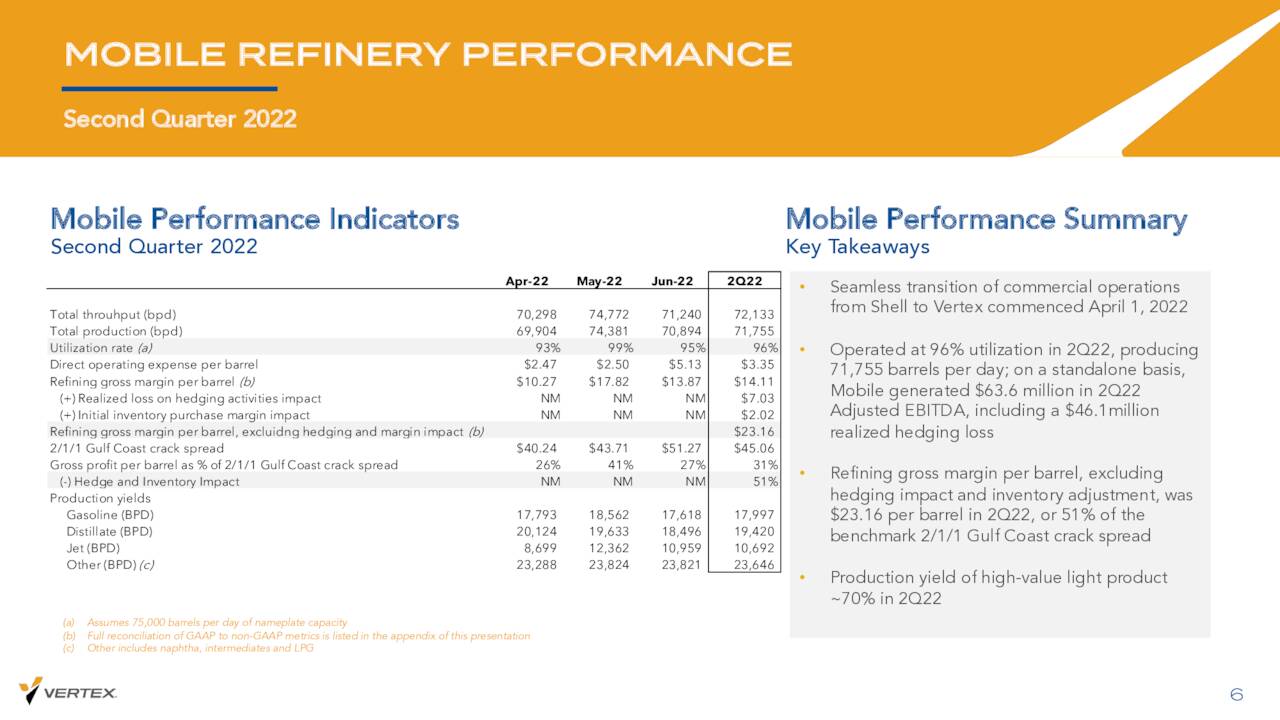

The company averaged just under 72,000 barrels per day of output. This is approximately 96% of capacity and above previous guidance of 69,000 to 70,000 barrels. Revenues surged to nearly $1 billion as the Mobile facility had its first full quarter of operations under Vertex. Adjusted EBITDA reached a record $71.3 million in the quarter, compared with just $4 million in the same period a year ago. The benchmark 2/1/1 Gulf Coast crack spread was $45.06 a barrel in the second quarter. This was just over an increase of 200% compared to 2Q2021.

August Company Presentation

Analyst Commentary & Balance Sheet:

The company’s CEO sold just over 70,000 shares in his holdings on July 12th and then again on July 20th. This looks like it was just over 20% of his overall stake in the firm. A director sold just over 130,000 shares in the company in early June which appears to be his entire stake in the firm. This is the only insider activity in the stock so far this year. It also appears approximately 30% of the outstanding float in VTNR is currently held short.

August Company Presentation

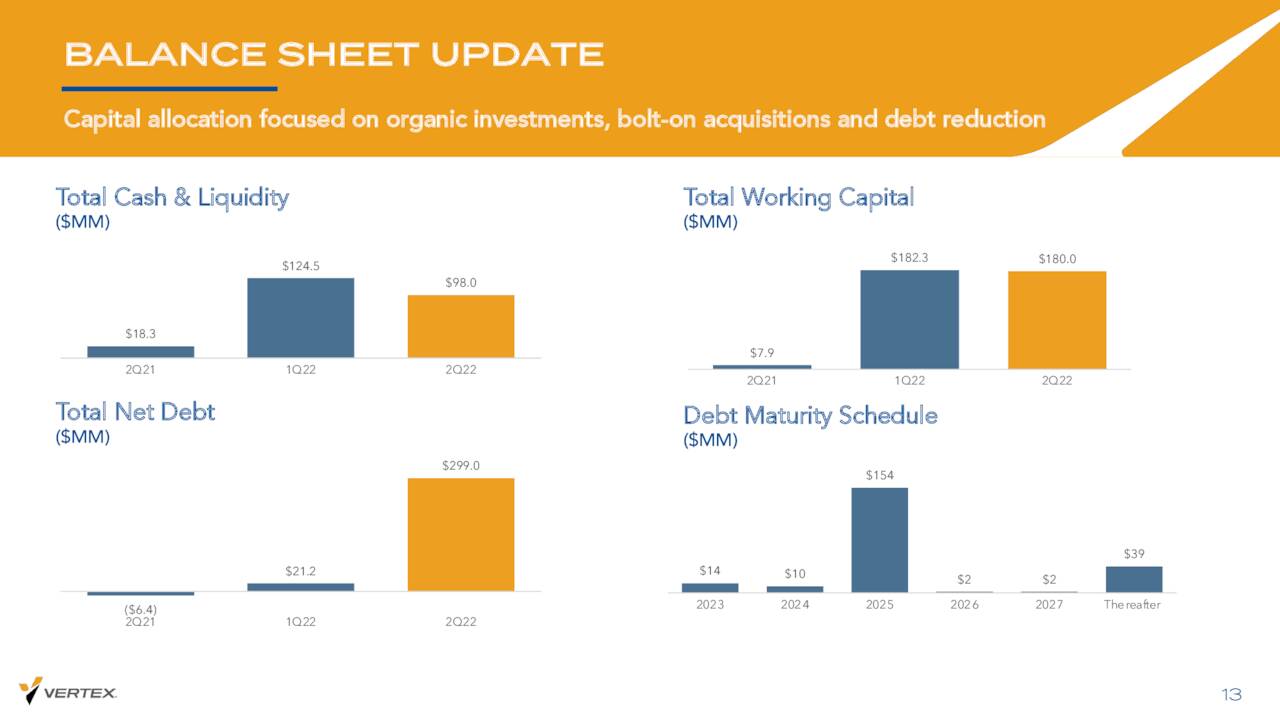

Since second quarter earnings were posted, Oppenheimer has downgraded its rating on Vertex to Market Perform while H.C. Wainwright ($15 price target) and Stifel Nicolaus ($18 price target) have reiterated their Buy ratings on the shares. The company ended the second quarter with nearly $100 million of liquidity against net debit of nearly $300 million.

Verdict:

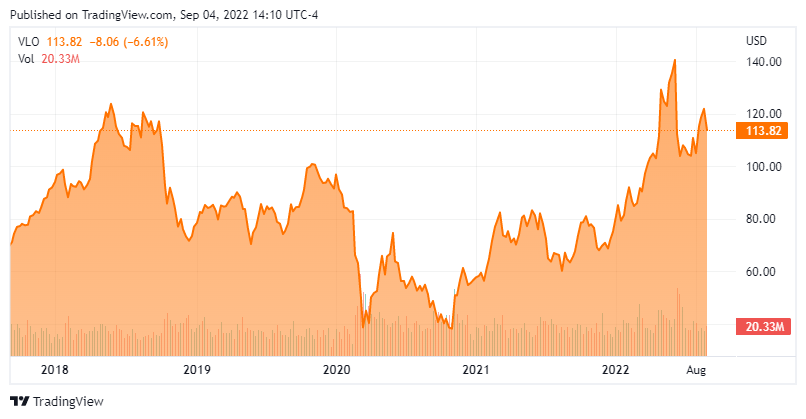

There a lot of mixed messages around trying to build an investment case for buying Vertex. Refiners are enjoying historical high crack spreads and there are moats around the business given we haven’t built a brand new refinery complex in the U.S. since the late 70s. These factors have certainly have helped lift the stock of refinery giant Valero (VLO) since the beginning of 2021. Vertex’s acquisition of the Mobile facility and its conversion project should lead to an explosion of revenues and one would hope profits.

Seeking Alpha

On the flip side, execution on several fronts by management leaves something to be desired and the deal with Clean Harbors falling through is a negative. The proceeds would have bolstered the company’s balance sheet and help management focus completely on the Mobile facility, where the company gets the vast majority of its revenue and EBITDA. Leadership is still pursuing the sale of these assets, which it hopes to do by the end of the year. The large short interest in the stock and the insider selling of the shares this summer also are concerning to some degree. The economy has also cooled considerably in 2022 from where it was in 2021.

I think Oppenheimer’s analyst had a nice summary around the company at this moment in time when he downgraded the shares in August:

“From an operating continuity perspective, Vertex’s first quarter of integrating the Mobile refinery had several positives, including the refinery reporting 96% capacity utilization. However, hedging and energy markets volatility negatively impacted monetization of spreads, which have seen compression since quarter-end.”

The Mobile acquisition is “transformative” for Vertex and still-elevated spreads as positive, “but given lack of visibility and management’s outlook for continued volatility in removing prior guidance, we believe investors will need to see consistent EBITDA/FCF generation from the business to regain conviction,” according to Kaye.

Therefore, I plan to avoid Vertex until it shows a bit more traction on its key initiatives.

Diligence is the mother of good fortune, and the goal of a good intention was never reached through its opposite, laziness. ― Miguel de Cervantes

Be the first to comment