Bruce Bennett

Verizon (NYSE:VZ) is one of the largest American telecommunication companies. The company has a market capitalization of just under $170 billion and a massive dividend yield of more than 6.5%. As we’ll see throughout this article, the company has the ability to drive more substantial returns than solely its dividends making the company a valuable investment.

Verizon Progress

Verizon is in the midst of an expensive 5G transition as evidenced through the $45 billion the company spent on C-band spectrum.

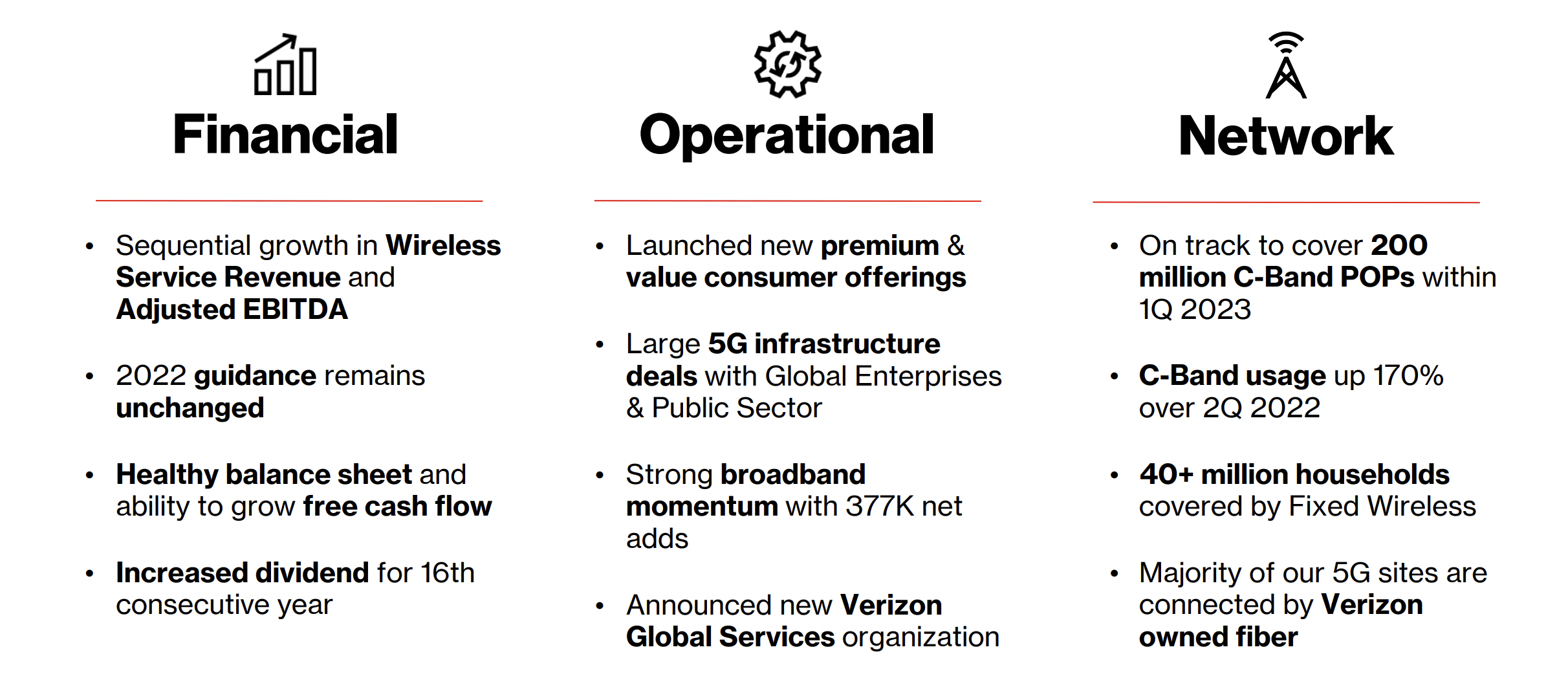

Verizon Investor Presentation

Verizon has continued to line up with its 2022 guidance while working to increase its FCF. The company increased its dividend for the 16th consecutive year and has continued to launch new offerings for customers. In broadband, the company saw 377k net new customer adds. Across the network the company’s expansion of C-Band usage is substantial and the company is working to continue expanding it.

The hope for the company is that the capital requirements of 5G will decrease substantially enabling the company to increase FCF and shareholder returns. Its need for continued massive capital spending will decrease.

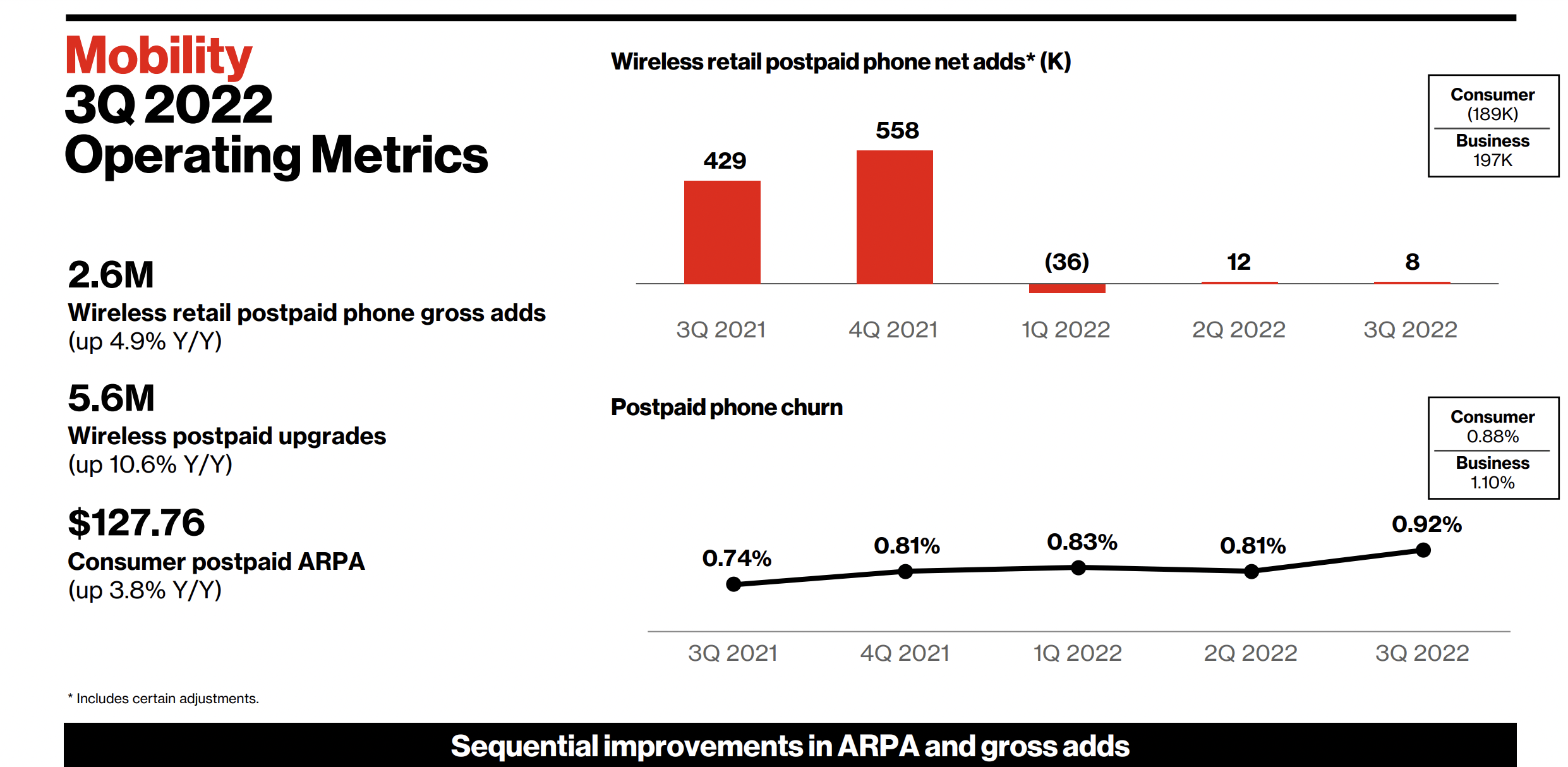

Verizon Segment Performance

Verizon has continued to see performance across all of its segments but increasing volatility.

Verizon Investor Presentation

The company saw continued YoY postpaid phone subscriber adds although churn kept the net adds low for the company. Churn has increased some in recent quarters, especially in the 3Q, and we expect churn to remain higher than normal given the economic uncertainty. The company’s $127.76 ARPA remains strong with its almost 4% YoY increase, which will help maintain the company’s overall margins.

Verizon Investor Presentation

The company saw 377 thousand broadband net adds in the quarter with 61k FIOS internet net adds. The company is less focused on gigabit than some of its competitors (such as AT&T) but it also has an incredibly strong and existing broadband business that makes chasing fiber less interesting for the company. Still its $3.2 billion Fios revenue is quite impressive.

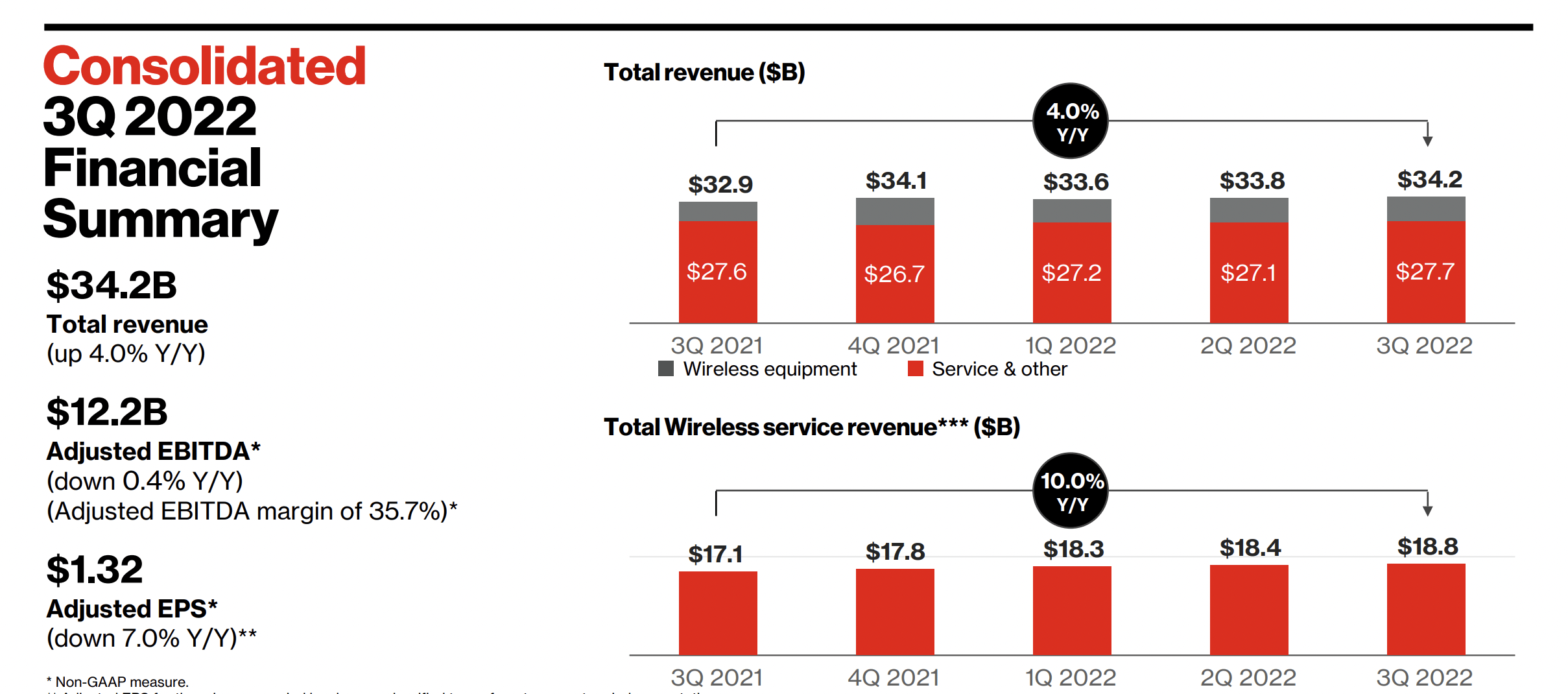

Verizon Financial Performance

Putting this all together we get the company’s financial performance and its continued focus on cash flow.

Verizon Investor Presentation

The company saw $34.2 billion in quarterly revenue, a 4% YoY increase. The majority of that is from the company’s service and other revenue with the company’s service business seeing 10% YoY revenue increase. The company saw a $12.2 billion adjusted EBITDA a 0.4% YoY decrease with 35.7% margins.

This slight decline in margins is concerning but overall the company’s margins remain strong. The company’s adjusted EPS decreased 7% YoY but keeps the company at a single-digit EPS.

YTD to the company has had $28.2 in CFFO, a $3 billion YoY decline. The company’s capital expenditures have remained higher as well, at $15.8 billion, or an almost $2 billion YoY decline. That shows the continued massive capital obligations that the company has. The company’s FCF remained strong at $12.4 billion, or roughly $16 billion annualized, with a ~70% payout ratio.

The company’s total debt post cash is just under $148 billion. We expect the company to continue maintaining its dividend and we’d like to see it utilize are remaining cash for debt repurchases.

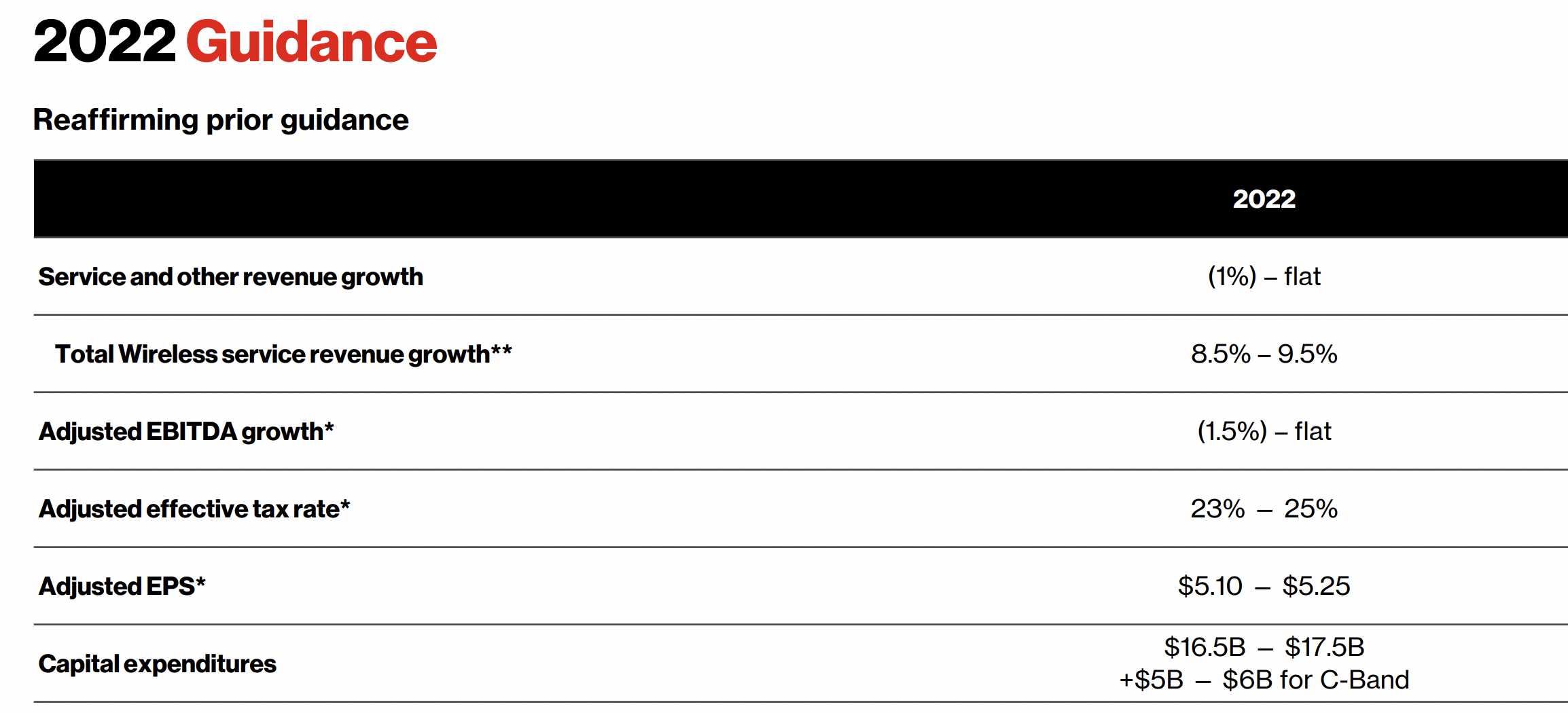

Verizon Guidance

So far the company has stuck by its prior guidance.

Verizon Investor Presentation

YoY, the company has kept its guidance in line with what was originally expected. The company’s adjusted EBITDA growth is disappointing, but partially expected in an expensive market. The company’s single digit P/E ratio shows its strong net earnings along with the company’s continued FCF yield of roughly 10%.

Its FCF could increase from $16 billion towards $20+ billion should the company manage to reduce its debt, enabling much more substantial and direct shareholder returns. The company could also use buybacks to save on dividend expenditures at current prices as long as the dividends remain well above interest rates.

Our View

Verizon is a unique company part of an oligopoly with T-Mobile (TMUS) and AT&T (T) with an incredibly strong portfolio of assets. That’s especially true on the east coast where the company is centered. The company has struggled to grow, but it’s managed to maintain its customer count, even with increasing churn in what’s been a volatile tech market.

The company has remained on track with its 2022 guidance and we expect that it’ll be able to handle this recession. The company’s FCF remains high and its payout ratio of 70% remains more than manageable for the company. The company has announced multiple times its continued commitment to maintaining its dividend.

We’d like to see the company aggressively pay down its debt outside of its dividend and at the current share price we think the risk-reward skews towards investing in Verizon for the long run.

Thesis Risk

The largest risk to the thesis in our view is the company’s debt load. The company has $160 billion in total debt along with $145 billion in long-term debt. The company has billions in annual interest expenditures, which can escalate rapidly with rising interest rates, and continued capital obligations that can make it hard for the company to continue shareholder returns.

Conclusion

Verizon stagnated through 2022 in a tough economy. At the same time, the company was forced to invest a massive amount of capital on building 5G to the tune of 10s of billions. The company was behind competitors such as T-Mobile and it’s been forced to spend rapidly in order to catch up with its business targets.

At the same time, from this and prior spending, the company has a massive amount of debt. That debt is costing the company billions in interest especially in a rising rate environment. The company can continue to afford its impressive dividend of almost 7%, however, we’d like to see it ramp up its interest spending as well.

Let us know your thoughts in the comments below.

Be the first to comment