dvulikaia

Verano (OTCQX:VRNOF) has been a difficult stock over the past year. Not only has the stock price continued to struggle as multiples compressed, but growth rates have come to a standstill as the industry works through excess supply and price compression. Meanwhile, the company’s adjusted EBITDA margins are being pressured and free cash flow has virtually disappeared. The company remains on a stronger financial footing than smaller peers due to its leaner cost structure and wide scale. I remain bullish on the long-term outlook for the US cannabis industry and VRNOF has what it takes to survive long enough to reap the rewards when normalization inevitably occurs.

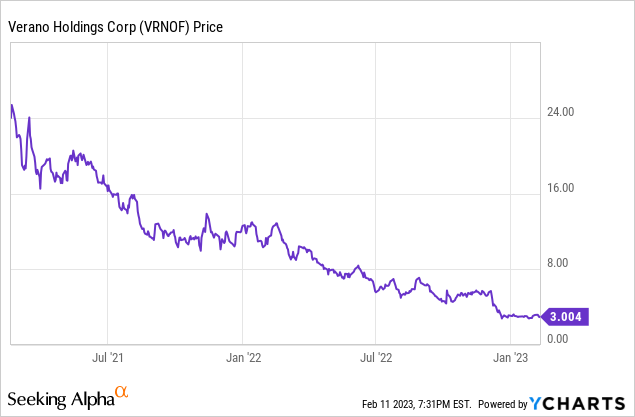

VRNOF Stock Price

VRNOF stock has been crushed since it came public in early 2021.

VRNOF Stock Key Metrics

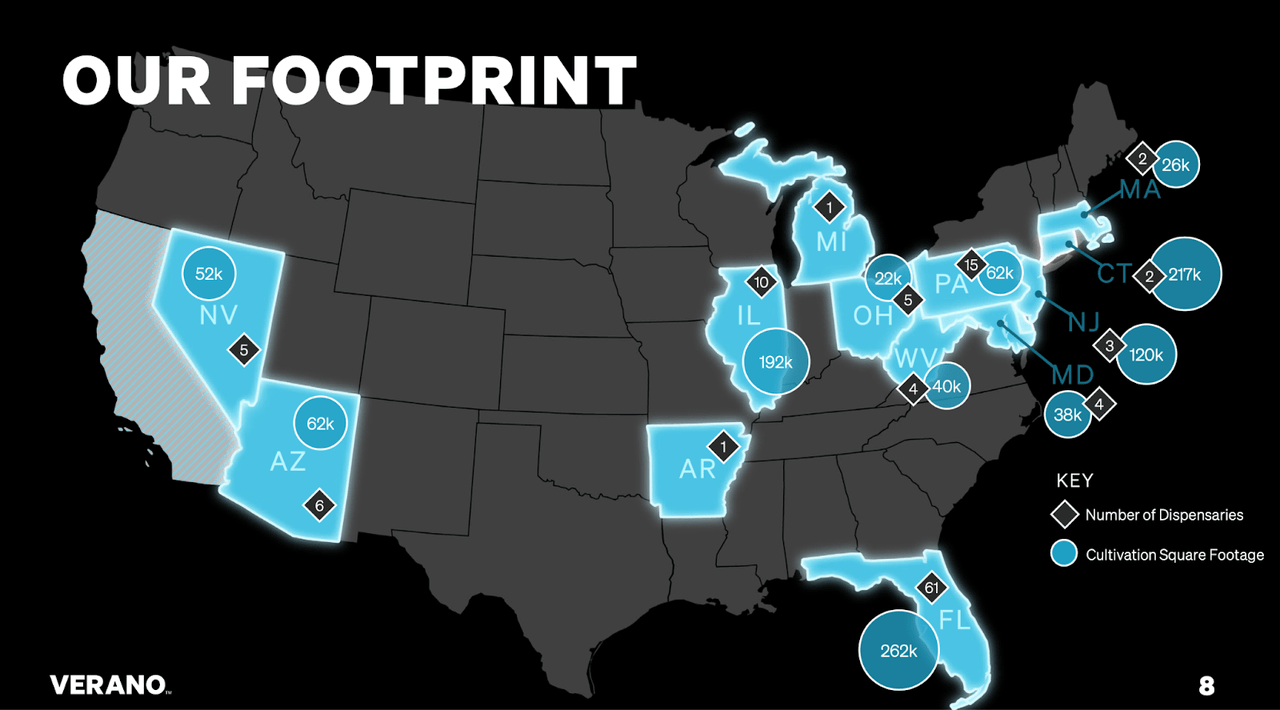

VRNOF remains one of the largest multi-state operators (‘MSOs’) with a 14 state footprint. It is worth noting that VRNOF no longer includes Minnesota or New York in its footprint due to repudiating its merger agreement with Goodness Growth (OTCQX:GDNSF).

2022 Q3 Presentation

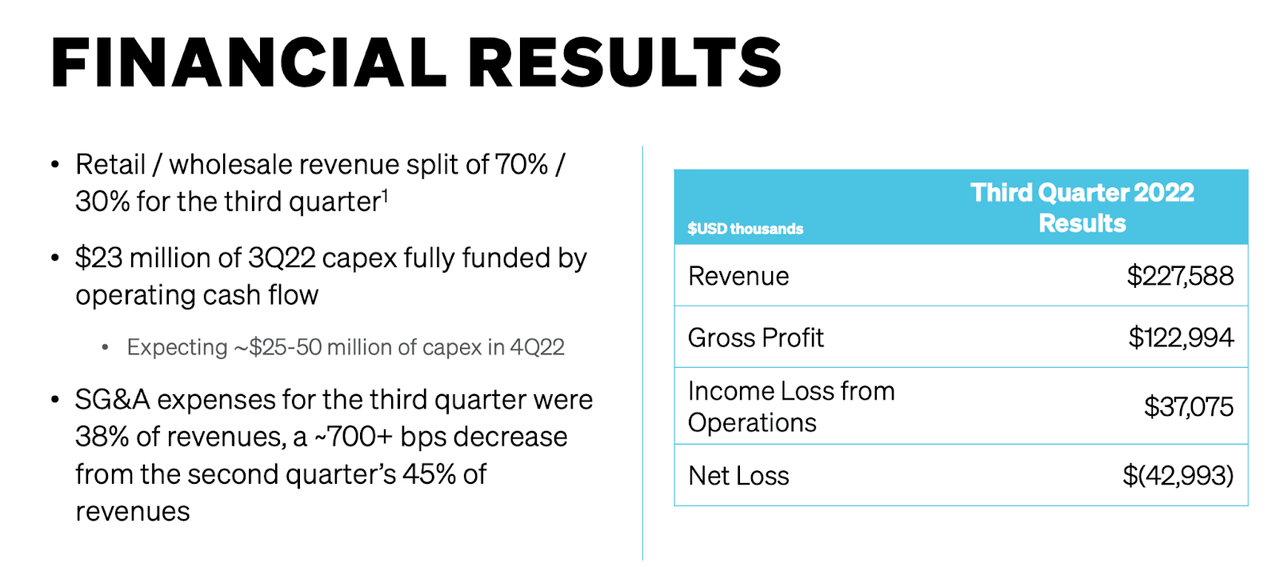

The latest quarter saw continued financial struggles, as revenue grew by only 2% sequentially and 10% YOY to $228 million. This is supposed to be a high-growth industry, but elevated supply has crashed the party.

2022 Q3 Presentation

VRNOF saw great weakness in the medical states of Pennsylvania and Florida, with that weakness partially offset by strength in the adult-use state of New Jersey. I personally wish that these MSOs would give a better state-by-state breakdown of fundamental results as the current disclosures make it hard to understand what is happening at a granular level.

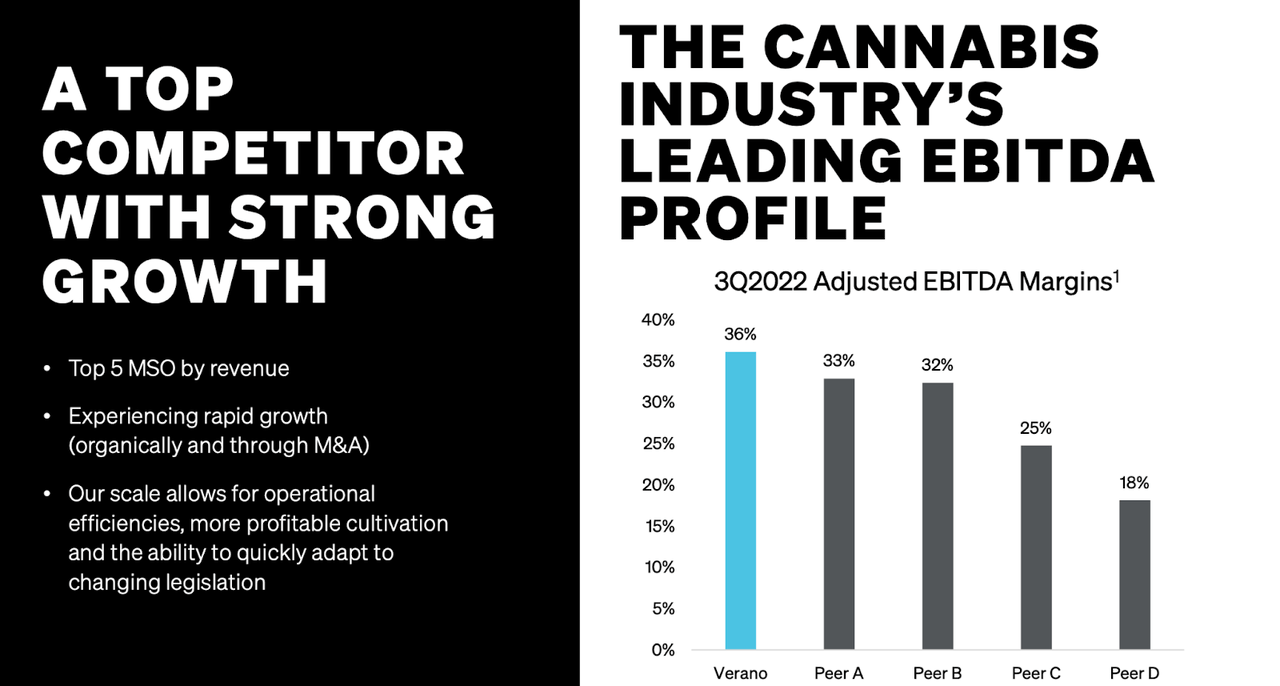

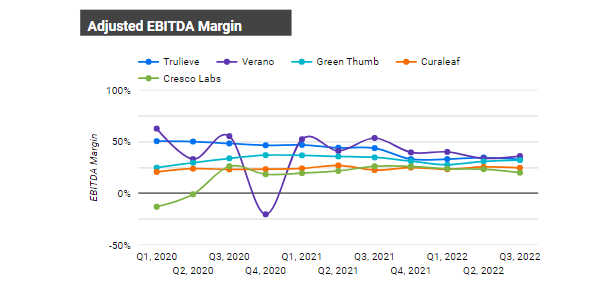

Adjusted EBITDA came in at 36% of revenues, which was highest among peers but far below the 48.9% margin posted in the prior year’s quarter.

2022 Q3 Presentation

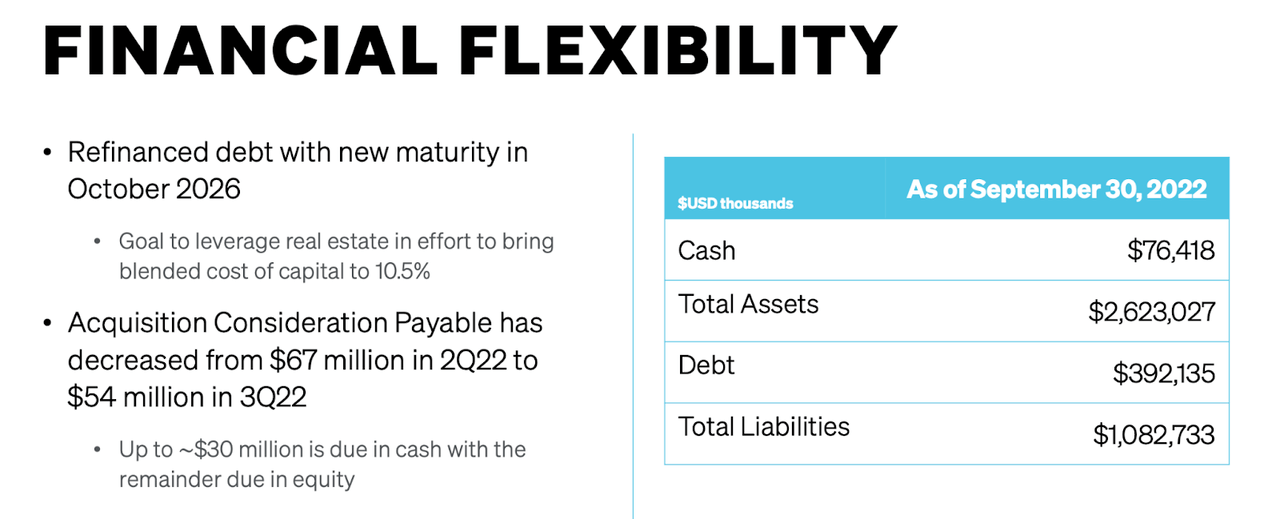

VRNOF ended the quarter with $76.4 million of cash versus $392 million of debt. That is a sizable debt load on a nominal basis, but the 1.2x debt to EBITDA ratio is competitive relative to top MSO peers.

2022 Q3 Presentation

On the conference call, management noted their intention to leverage their unencumbered real estate to bring down their cost of capital to approximately 10.5% in the medium term.

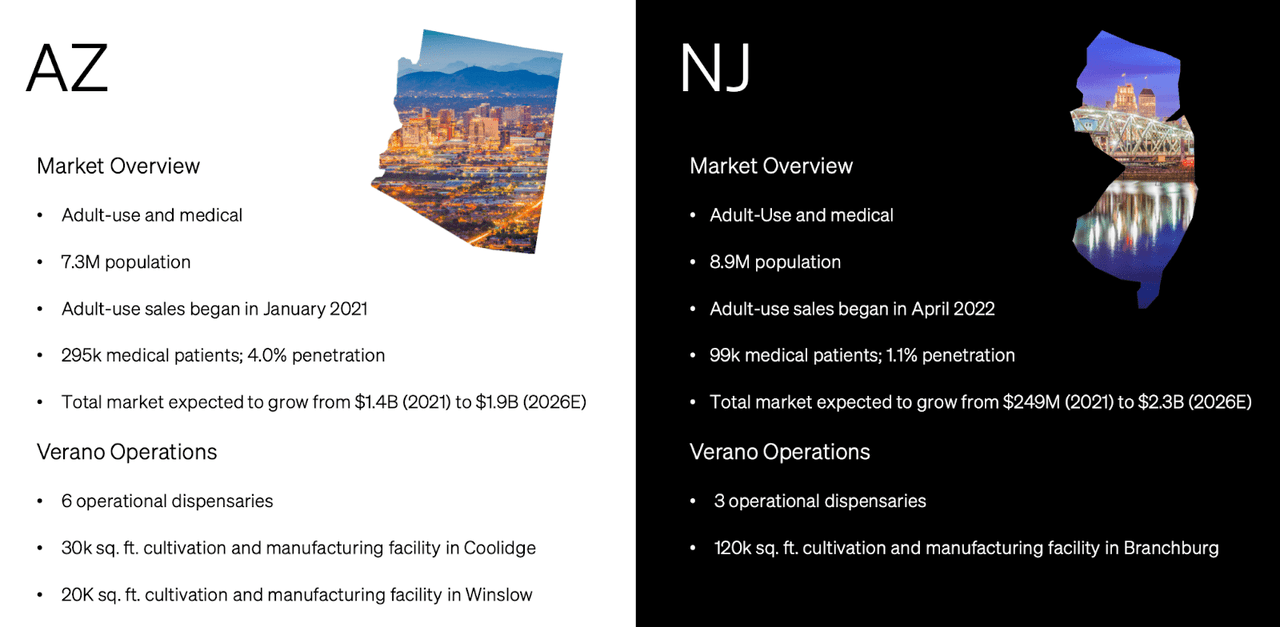

New Jersey continued to be a strong state for the company as VRNOF owned its third and final dispensary in the state in Zen Leaf Neptune. New Jersey wholesale revenue grew 3x over the prior year and retail revenue grew 5x YOY. Management noted that they expect to see normalization over the coming months as the “initial adult-use excitement wears off.”

2022 Q3 Presentation

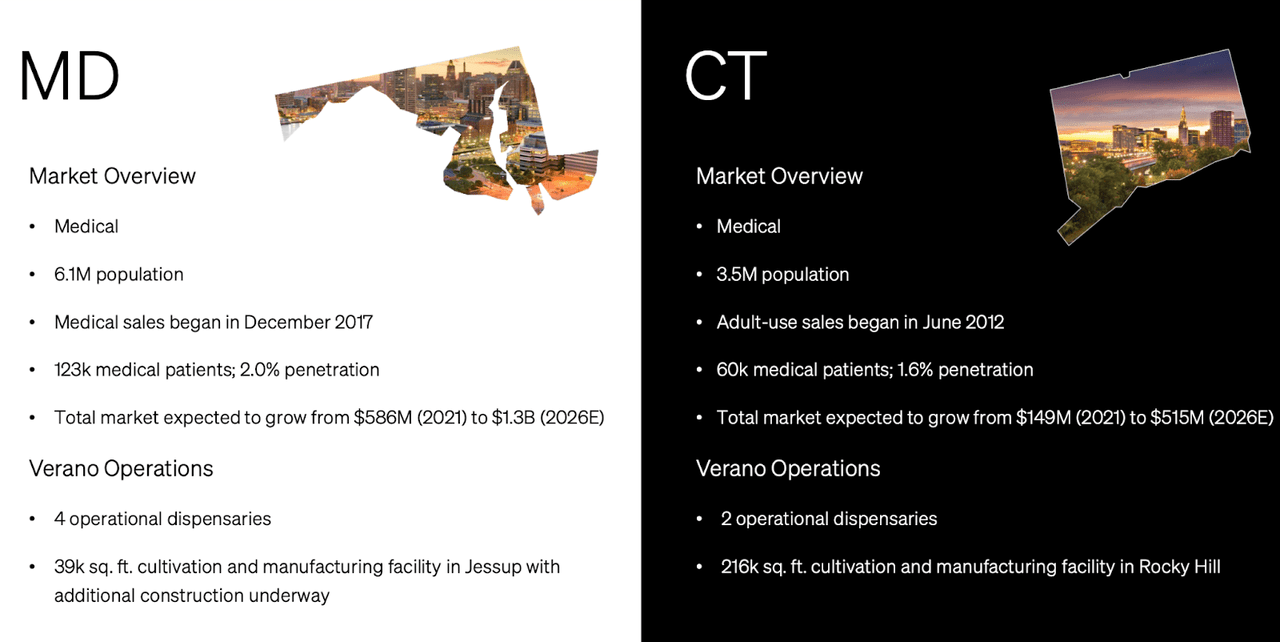

VRNOF was a winner in the 2022 midterm elections, as Maryland voters passed a ballot measure to legalize adult-use sales. VRNOF is still waiting for Connecticut to roll out adult-use cannabis sales after the state legalized it in 2021 (note there is a typo in the presentation slide below)

2022 Q3 Presentation

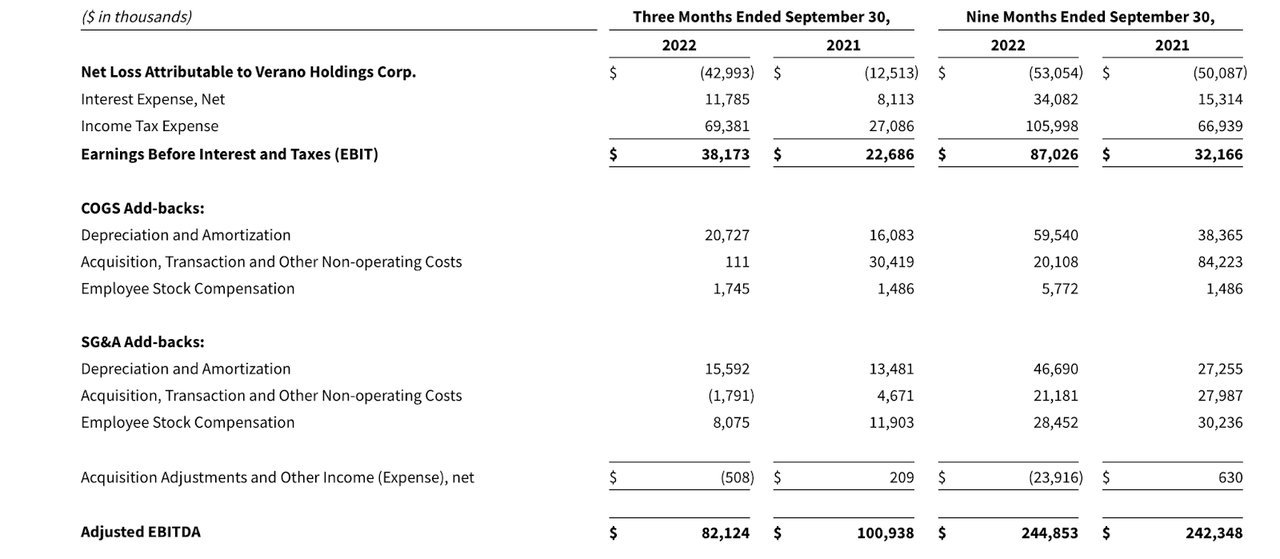

I have been focusing on MSOs which can generate positive free cash flow even inclusive of 280e taxes, as I view decriminalization to still be many years away (though I remain hopeful that President Biden can follow through on his announcement to re-schedule the plant).

VRNOF remains one of the few MSOs which are generating positive free cash flow, which I define as being adjusted EBITDA minus interest and tax expenses. Free cash flow stood at $0.9 million in the quarter – down from $65.7 million in the prior year, largely due to an increase in tax expenses. I note that if we normalize the latest quarter’s tax rate (as the payment encompassed many quarters of past due taxes), then free cash flow would have been approximately $44 million higher.

2022 Q3 Presentation

Is VRNOF Stock A Buy, Sell, or Hold?

After seeing strong margins heading into 2021, all the MSOs have seen margin pressures during a period in which investors may have been hoping for margin expansion.

2022 Q3 Presentation

VRNOF has historically traded at a discount to peers and continues to do so today.

Cannabis Growth Portfolio

I find that discount to be undeserved considering that many of these companies own very similar assets and VRNOF generates solid cash flows. With the stock trading at just 4.4x adjusted EBITDA, the valuation is not so commanding for investors willing to wait for eventual legalization. Meanwhile, the tough operating conditions may lead to a “shake out” of weaker operators as the strongest surviving operators come out stronger.

Key risks include rising interest rates and ongoing price compression. VRNOF may need to refinance maturing debt at higher interest rates which would put further strain on cash flows. It is unclear if price compression is subsiding and how this impacts the long-term growth trajectory. This is an environment in which investors should invest with management teams that are focused on cash flow generation over loss-generating revenue growth. This is one reason why I prefer VRNOF over industry-favorite Curaleaf (OTCPK:CURLF). But it is possible that management changes tune moving forward – I would not be pleased to see a large M&A deal. I continue to rate VRNOF a strong buy on account of the low valuation but caution the lack of near term catalyst and the elevating risk profile.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment