The 6 eggs in Diversified’s Basket

Jonathan Knowles

Values are in CAD unless noted otherwise.

We had suggested an alternative the last time we wrote on Diversified Royalty Corp. (OTCPK:BEVFF) (TSX:DIV:CA). Diversified had delivered impressive returns to its investors over the last several years, but we were a bit weary of the debt load. One did not have to look too far for the alternative of our choice.

Diversified holds a good collection of businesses, most of which should be firing on all cylinders as Canada achieves widespread vaccination. The company’s decision to do a minimal cut to its dividend has paid off as it made it through the worst of the pandemic and now is poised to benefit. We still think the debt load is high the business. If you still like the business and want to access it in a more conservative manner, the convertible debentures trading on the TSX offer a good yield to maturity and we think they are safe.

Source: Diversified Royalty: Eggs In More Than One Basket

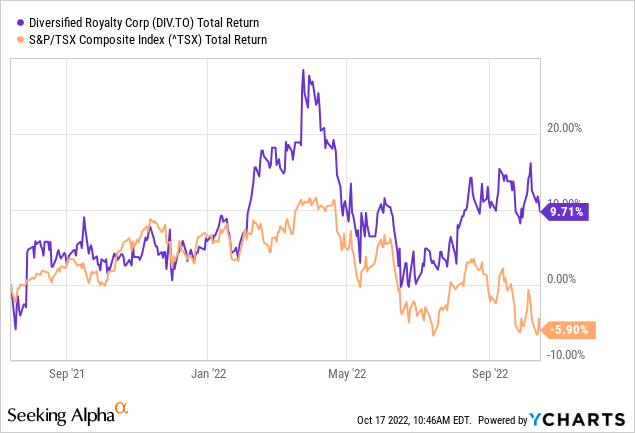

There was little chance these would be converted, and we liked the yield we would get for the remainder of the short duration. The commons have also done very well since then.

If you wanted to avoid the volatility for almost the same returns, you could have gone for our suggested alternative though.

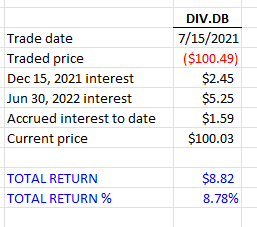

Author Calculations

Who would be unhappy with an 8.78% total return over the last 15 months? With the DIV.DB issue to be redeemed shortly (partially redeemed already), let’s review the numbers again and see if we think the business will hold up just as strong in the upcoming recession. We also throw in an alternative just like the last time.

The Business

Diversified is in fact diversified with its hands in six businesses from varied industries. It earns top-line royalties and management fees from well-established outfits, namely, Mr. Lube, AIR MILES@, Sutton, Mr. Mikes, Nurse Next Door, and Oxford Learning Centres. Like other royalty plays, this one too has a lean corporate level expense structure comprising salaries and benefits, G&A, professional fees and interest on credit facilities.

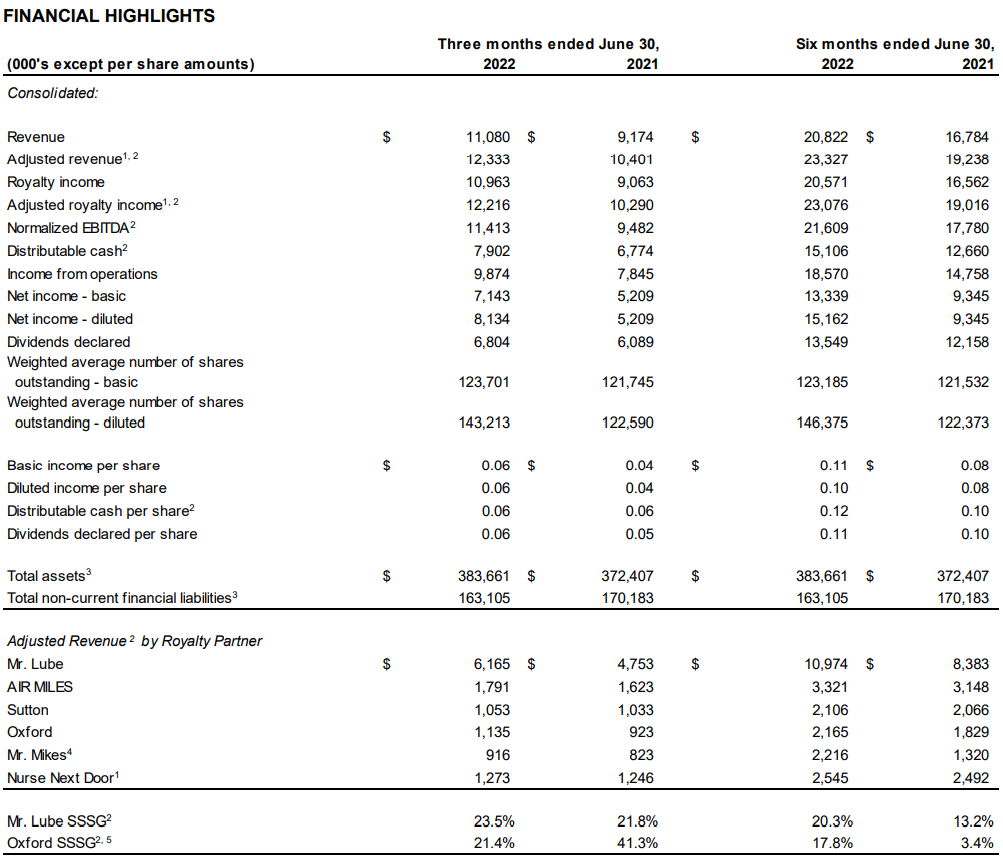

Q2-2022 & Valuation

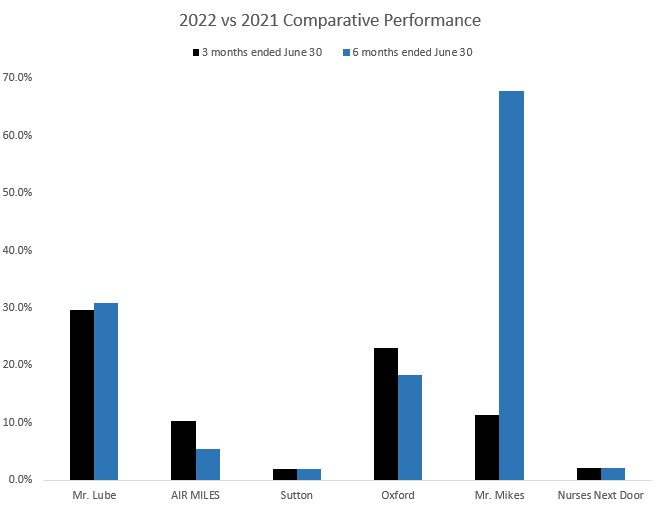

All six royalty partners showed an increase over the comparative periods, 2% and 4.4%, respectively.

Q2-2022 MD&A

This should not really come as a surprise since everything is back to business unlike the various COVID wave related closures we saw in the last couple of years.

Author’s Rudimentary Charting Abilities

Diversified earns 7.95% (increased from 7.45% on May 1, 2021) on non-tire sales from Mr. Lube and 2.5% on tire and rim sales. The royalty pool is adjusted annually on May 1 to reflect the net increase due to the new locations or vice versa. Both May 2021 and 2022 experienced an increase in the royalty pool (13 in 2021 and 4 in 2022). The outperformance with the comparative period has been attributed to the increase in the royalty pool, rate, growth in business, and removal of COVID-19 related restrictions.

Diversified earns 1% of the gross billings from the AIR MILES reward program. The key metric in this program, the AIR MILES reward miles issued increased by 7.8% in Q2 2022. Spurred by the summer travel after a hiatus of the last two seasons, the miles redeemed increased by 54%. While Sobeys will be exiting this program by Q1 2023, AIR MILES will now be expanding to competitors previously excluded due to their agreement with the former. Sobey’s absence will be noticed in terms of reduced miles issued as it contributed 10% of the licensee’s adjusted EBITDA.

Diversified earns a fixed rate per real estate agent in the Sutton royalty pool. This rate increases by 2% each July, which is roughly what we see in the comparative performance above. Year over year, the number of agents remained the same at 5,400. Considering what is happening to the Canadian real estate market, we would think this number will drop over the next 12 months.

Diversified earns 7.67% royalty on top line sales from the education services based, Oxford royalty pool, which is adjusted each May 1 to account for the net additions or closures. While the number of locations (in Canada and the US) remained the same compared to the prior year, this franchise witnessed record sales in May and June of this year. The move back to pre-COVID normalcy and in person tutoring resulted contributed to the stronger same store sales.

The food services franchise, Mr. Mike, witnessed impressive but predictable growth, being the biggest beneficiary of removal of the Covid restrictions. However, $0.55 million in income received from this restaurant chain was payment for the royalty and management fees deferrals it enjoyed over the last two years. Another $1 million towards these is still outstanding and the expectation is that it will be recognized on receipt down the line. With 38 locations in the royalty pool, Diversified collects 4.35% on the restaurant sales with a 2% per annum royalty growth in effect until 2023.

Diversified earns the greater of 6% of gross sales of the stores in the Nurse Next Door royalty pool or around $0.42/month subject to a 2% per annum increase built in. The increase we see over the comparative period is the aforementioned 2%. They added 20 new franchises in Q2 2022. This business is treated as a financing arrangement rather than an intangible asset for reporting purposes since Nurse Next Door has a buy-out option at any time after November 15, 2026.

Dividends

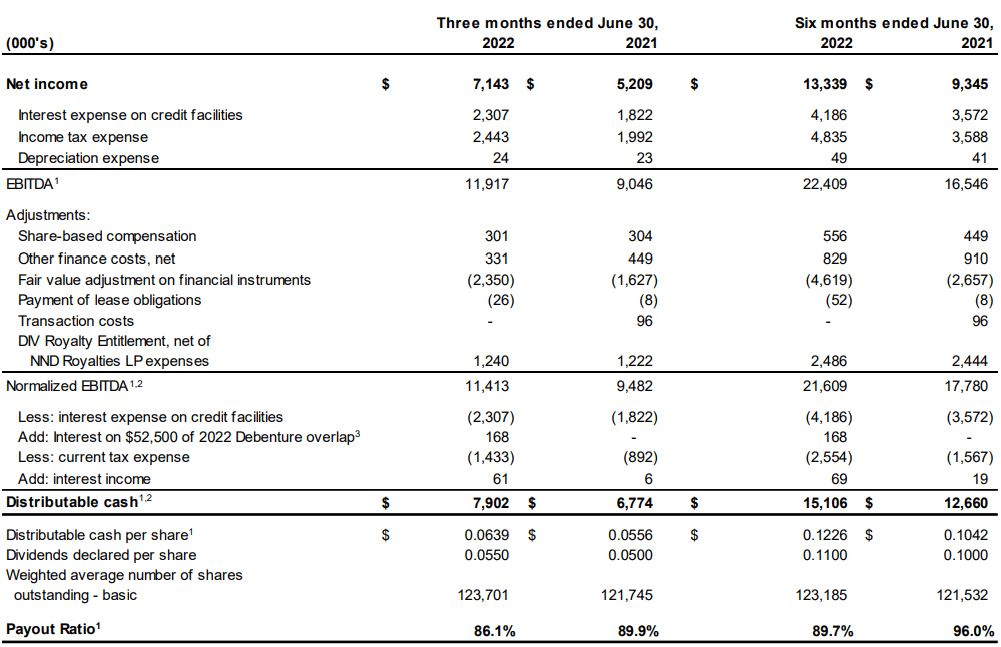

The last time we wrote on this company, we expected the payout ratio to come back down to under 100%. That along with our target of 24 cents a share of distributable cash has come to pass.

Q2-2022 MD&A

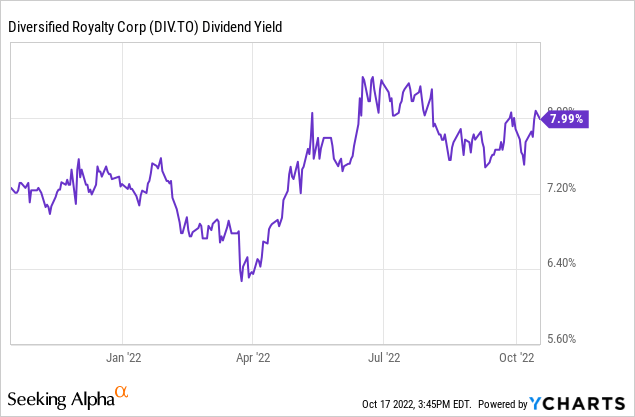

COVID-19 brought about a decline in this Royalty Corp’s dividend payments from recently increased 19.58 cents a month to 16.67 cents a month. Due to the nature of their business and streamlined expenses, royalty businesses usually pay out most of what they make to their shareholders. Accordingly, we started seeing increases in the payouts in conjunction with positive developments like easing of the COVID restrictions and subsequent increases in the revenues. The dividend now stands at 18.33 cents a month, still under the pre-COVID levels. We do not expect them to go crazy with hikes in the next little while as they have the upcoming recession and the higher financing costs on their plate.

Alternative

8% yield is nothing to scoff at, but as we earlier saw, this comes with the common stock price volatility. Retirees or income investors with a less robust constitution should consider other set of debentures issued by this company.

TMX

With a lock out period until June 30, 2025, these currently yield 6.5%.

The 2027 Debentures mature on June 30, 2027 and bear interest at an annual rate of 6.00% payable semi-annually in arrears on the last day of December and June in each year, with the first such payment having been made effective June 30, 2022. At the holder’s option, the 2027 Debentures may be converted into common shares of the Company at any time prior to the close of business on the earlier of the last business day immediately preceding June 30, 2027 and the date specified by the Company for redemption.

Source: Q2-2022 MD&A

However, with the capital appreciation built in (redemption at par), the yield to maturity is 8.47%.

Canadian Convertible Debentures

Verdict

With the impact of the higher financing costs and the recession expectations, we would choose to wait it out with the debentures rather than the volatility of the common shares of this inflation hedge. The company runs very asset-light and debt to EBITDA is about 3.9X. Inflation has continued to help them, and current interest coverage is bordering on 4X. This coverage should move lower as the credit facility is floating.

Q2-2022 M&DA

with the expected rate hikes, interest coverage likely drops to 2.75X by the end of 2023, but we see this as adequate. We view the diversified set of royalty partners performing about in line with the Canadian economy, but we see Diversified Royalty outperforming as it retains a positive sensitivity to the high inflation numbers. The yield is solid and with less than 5 years left to maturity, there is low duration risk. In case the shares perform really well (not our outlook) the conversion feature at $4.05 comes into play. But we are only interested in this for a safe yield. We rate the debentures a buy and the common shares a hold.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Be the first to comment