DNY59

Investment Thesis

Veeva’s (NYSE:VEEV) Q3 2023 results didn’t quite live up to investors’ expectations. Going into earnings I concluded my previous article with this,

While there’s clearly a lot to like about its path of innovation and execution, I nevertheless struggle to figure out how paying up more than 30x forward EPS for something growing at close to 15% CAGR is attractive.

Today, I stand by that statement. I continue to be bedazzled by Veeva’s strong profitability, but its valuation remains stretched for me.

What’s Happening Now?

Veeva is moving its customers from the Salesforce (CRM) Platform to the Veeva Vault Platform. Clearly, Veeva now has enough scale that it makes sense to go off and design its own offering, a more customized customer experience platform. This transition is expected to start early in Calendar 2024 and gain traction in 2025.

Meanwhile, closer in time, Veeva discussed on its earnings call that it’s seeing ”a little bit of additional scrutiny than we saw 90 days ago, but nothing significantly different than that”.

This is an echo of what nearly every other tech company is seeing right now, an elongation in the earnings cycle.

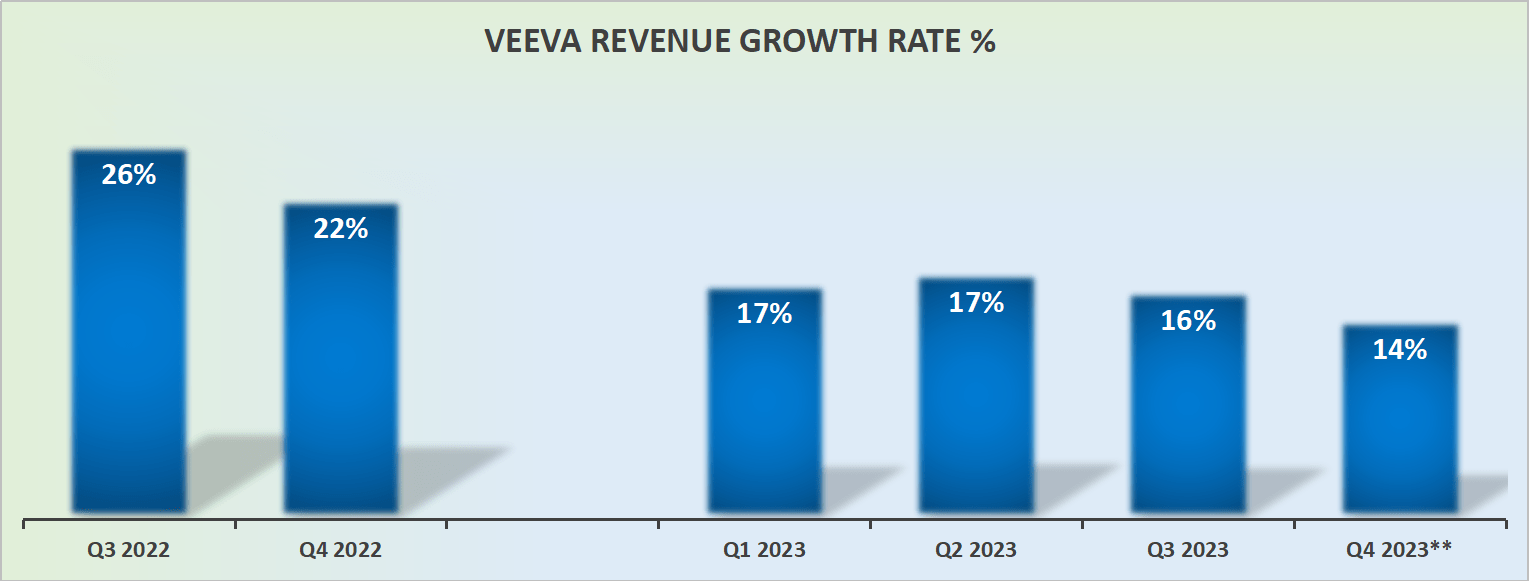

Veeva’s Revenue Growth Rates Slow Down, But Details Matter

Veeva’s revenue growth rates

At the most superficial level, Veeva’s revenue growth rates are slowing down. But once we look beyond this headline figure, the picture improves.

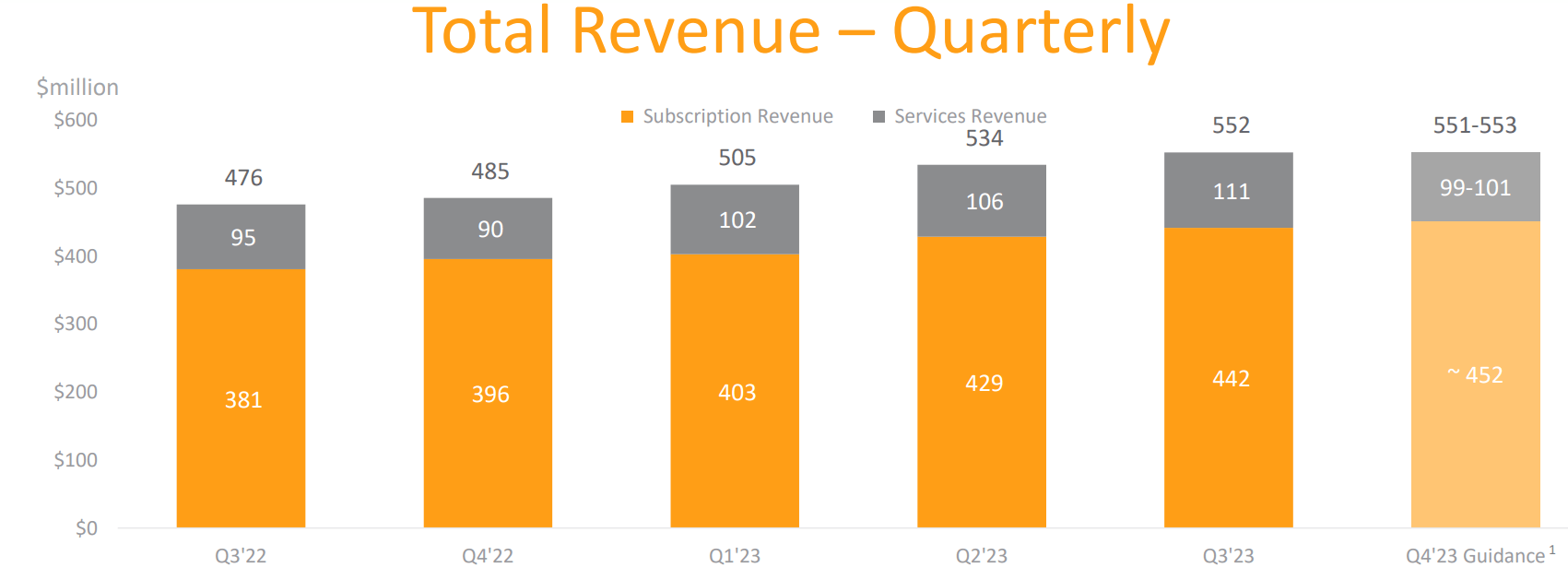

Veeva Q3 2023

What you see above, is that sequentially, Veeva’s subscription business continues to expand. While its Service business is causing a headwind to Veeva.

However, keep in mind that Veeva’s Subscription business carries gross margins of approximately 86%, which are much higher than the gross margins associated with its Service business.

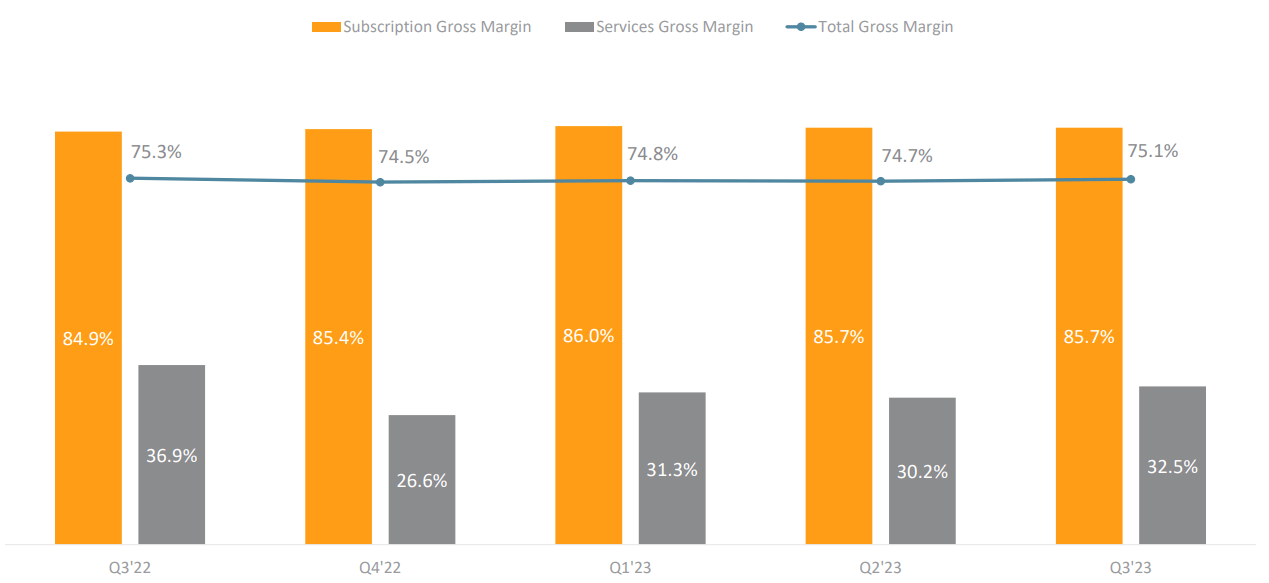

Veeva Q3 2023

Hence, this is my point. Veeva is delivering strong and stable profitability where it matters most, its core offering.

And this takes me to discuss the crown jewel of this investment thesis.

Crown Jewel, Profitability Profile

The one aspect that has always been key to Veeva’s investment thesis, is that it’s a highly profitable company. At least as far as tech companies go.

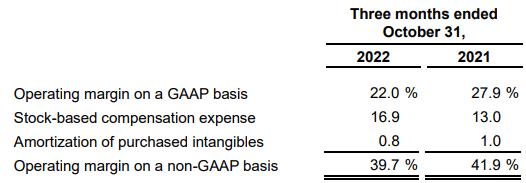

With that in mind, consider the table that follows.

Veeva Q3 2023

As you can see above, on a GAAP basis, Veeva’s operating margins were 22% profitable. This is astounding. Asides from Adobe (ADBE) and the mega caps, I don’t personally know of any US-based tech company that has these kinds of profit margins. That being said, outside of the US, it’s a different story. But investing outside of the US comes with its own trials and tribulations, too.

On the other hand, Veeva’s GAAP profits margins did shrink by approximately 590 basis points. In a time when investors are highly fretful and anxious about profitability, this will surely weigh down on investor sentiment.

Furthermore, we have to keep in mind that compared with the same period a year ago, stock-based compensation is up 50.2% y/y. So, investors will be feeling some level of vexation to see stock-based compensation significantly outperforming top-line growth.

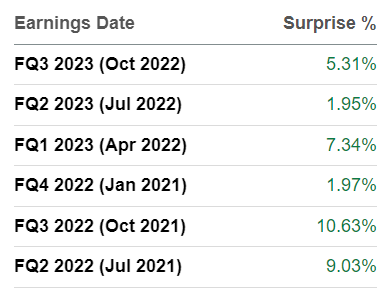

On yet the other hand, I maintain that where an investment in Veeva performs particularly well is that it has a history of beating analysts’ EPS expectations.

Veeva earnings surprises

Going back several quarters, Veeva has consistently beaten bottom-line estimates, by close to 2% each time and often significantly more.

With that in mind, let’s discuss Veeva’s valuation.

VEEV Stock Valuation – 39x Non-GAAP EPS

Looking out to the next fiscal year (ends January 2024), Veeva is priced at less than 40x next year’s non-GAAP EPS. Obviously, in this macro environment, a lot can happen in twelve months. This is a highly unstable macro environment, and projecting earnings is challenging, uncertain, and error-prone right now business.

As a reminder, just looking out the next 90 days, Veeva’s guidance came in below consensus view. So, a lot can happen between now and the end of fiscal 2024.

On the other hand, as noted already, there aren’t too many tech companies where discussing a company’s earnings even starts to make sense. Indeed, the vast majority of tech companies are still trying to figure out how to make a profit. Thus, the fact that not only Veeva is highly profitable, plus its valuation multiple isn’t that stretched, clearly is bullish for investors.

The Bottom Line

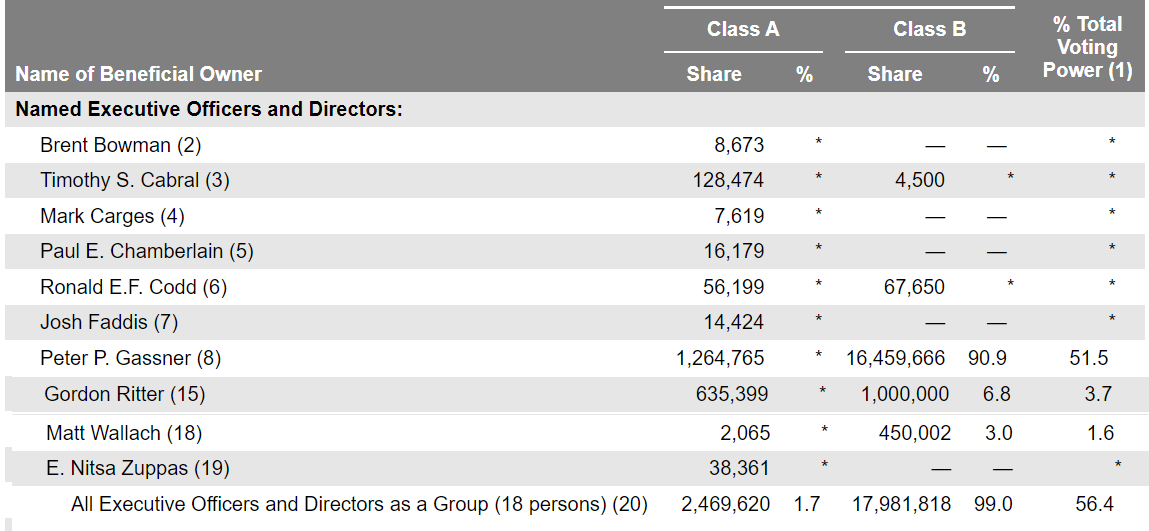

I’ve often maintained that when one invests alongside management, management will do what’s right for long-term shareholders.

What the table that follows shows, is a tangible reflection of that point of view.

Veeva proxy statement

As you can see here, management holds a fair amount of ownership of Veeva. Note, class B shares, voting shares, are converted into one share of Class A common stock.

Accordingly, management is highly motivated and financially incentivized to increase Veeva’s intrinsic value and drive its share price higher with time.

It’s reassuring to know that passive investors are in good hands.

Be the first to comment