maki_shmaki/iStock via Getty Images

The Iron Ore Investment Thesis Depends On China’s Reopening Cadence

Iron ore is a critical commodity in steel production, which has spot prices tied to the global cycle of construction and manufacturing sectors. Over the past few weeks, China’s rapid reopening cadence from the previous Zero Covid Policy has tremendously boosted iron ore prices. As a result, spot prices are now quickly approaching $118 per metric tonne at the time of writing, rallying by 49.5% from the recent bottom in November 2022. This is because the country accounted for an immense 43.07% of the global iron-ore demand at 1.12B tonnes.

Now, why does this matter to Vale S.A. (NYSE:VALE)? The company remains one of the largest iron ore producers globally at 310M metric tonnes in 2022, with up to 360M tonnes planned by 2026. While the company does not break down its revenue by geographical segments, it is unsurprising that the stock has rallied by 38.6%, since the commodity comprises 59.7% of its sales over the last twelve months.

Market analysts are bullish about the recovery of iron ore prices to the $150-$200 range as well, near the hyper-pandemic highs, due to the massive injection by the Chinese government at 300B Yuan (the equivalent of $43B) for infrastructure investments. We are already starting to see signs of reversal with the recent relaxation in property regulations indeed, including lower mortgage rates, cap on real-estate commissions, financing policies toward debt-ridden developers, and easing previous cooling-down measures, among others.

In addition, a decade-old policy has already been reversed by the China Securities Regulatory Commission, allowing qualified property developers to obtain backdoor financing through other listed companies. Zerlina Zeng, senior credit analyst at CreditSights Singapore LLC, said:

This is a signal from the top regulators in an attempt to help restore market confidence in the real estate sector and create a positive feedback loop between the homebuyers, developers, and the physical market. (Bloomberg)

These strategies may not directly trigger the immediate recovery of the property market in China due to the regulatory time lag, the country’s rising COVID-19 infections, and Chinese New Year festivities. However, we expect these headwinds to rapidly lift by mid-2023, with market analysts already bullishly projecting a GDP recovery to 4.7% in 2023, against 2022 numbers of 3% and 2019’s 6%.

In addition, VALE is aggressively protecting the iron ore prices by carefully managing its production for 2023. The management delivered lower-than-expected guidance of up to 320M metric tonnes against the consensus estimates of 325.6M and its total capacity of 400M. By not flooding the market with surplus iron ore and focusing on higher-quality ore and value-added production, the company also expects to deliver improved profit margins, potentially expanding its dividends and cash flow ahead. Gustavo Pimenta, CFO of VALE, said:

The margins are substantially bigger. So even though I’m at 340-360 million tons, from a value creation standpoint, we’ll be adding a lot of value to our shareholders. (Bloomberg)

Lastly, China’s iron ore inventory remains low at 131.3M metric tonnes at the time of writing, suggesting a well-balanced supply and demand, further stabilizing the iron ore prices and crude steel production momentarily. Once the country’s property market recovers in earnest from H2’23 onwards, we expect to see a consequent rally in iron ore prices, triggering a similar rally in VALE’s stock prices.

The Base Metal Business Still Looks Robust, Despite The Separation

On top of a partnership with Ford Motor (F) to develop nickel in Indonesia, VALE has also signed long-term nickel supply agreements with Tesla (TSLA) and General Motors (GM). This is attributed to the demand for alternative batteries in the EV market, aside from the commonly used lithium iron phosphate LFP battery with an average power density between 160 and 200 Wh/kg. NMC (Nickel, Manganese, and Cobalt) batteries may offer up to 270 Wh/kg, which expands the EVs’ mileage by 20% to 300 miles per full charge. Therefore, it is unsurprising why some automakers continue to offer the premium NMC option, despite the higher price tag by 20%.

In the meantime, VALE also seeks to decouple its base metal business away from the core iron ore business segment, potentially unlocking up to $40B in additional value. Interestingly, the company seeks a partnership strategy instead, instead of the usual IPO path. While nothing was mentioned, we posit that the other party may be TSLA, since the latter was reportedly interested in buying a stake in Glencore back in 2021, though holding back due to the coal business complication. Assuming so, it made sense for the VALE management to revisit the business separation, despite the peak recessionary fears in 2023.

The nickel and copper business is important to VALE indeed, since it accounts for up to 15% of its annual revenues. Furthermore, the company seeks to expand its nickel production at a CAGR of 6.65% from 168K tons in 2021 to 300K tons in 2030, while similarly tripling its copper output to 900K tons at the same time. Its prospects are bright indeed, since the global market size for these two commodities is expected to expand at a CAGR of 4.9% to $500B by 2030.

With TSLA CEO famously guiding up to 20M of annual EVs output by 2030, it is no wonder that the company needs to shore up its long-term supply agreement, especially due to the intense electrification efforts by many other automakers and renewable companies. However, we are uncertain how it aims to finance the partnership at approximately $20B, due to the impact of recessionary fears on EVs demand. The automaker reportedly had to offer rare discounts for customers in the US, China, Japan, South Korea, and Australia to keep up its sales volume.

Meanwhile, TSLA continues to report a robust balance sheet, with cash/investments of $21.1B and minimal long-term debts of $1.4B in the latest quarter. However, with the Berlin and Texas Gigafactories still ramping up to their design capacity, the company may potentially report elevated capital expenditure in the short term, if the CEO is truly serious about its twelve Gigafactories globally by 2030. In addition, public sentiments on TSLA have also deteriorated, with negative perception expanding tremendously from 4.2% in November 2020 to 22% in November 2022. This has naturally impacted its stock prices, which tragically declined by -66.04% in the past year, against VALE at 19.59% and the S&P 500 Index at -17.12% at the same time.

On the other hand, we expect VALE to benefit from the eventual possible partnership, since we may see clear top and bottom line growth moving forward, attributed to TSLA’s projected revenue CAGR of 31.4% and EPS CAGR of 36.8% through FY2025. This may suggest a potential upward rerating of the miner’s forward execution as well, in our view, against the current market projection of -5.4% and -9.5% at the same time. Only time will tell.

So, Is VALE Stock A Buy, Sell, Or Hold?

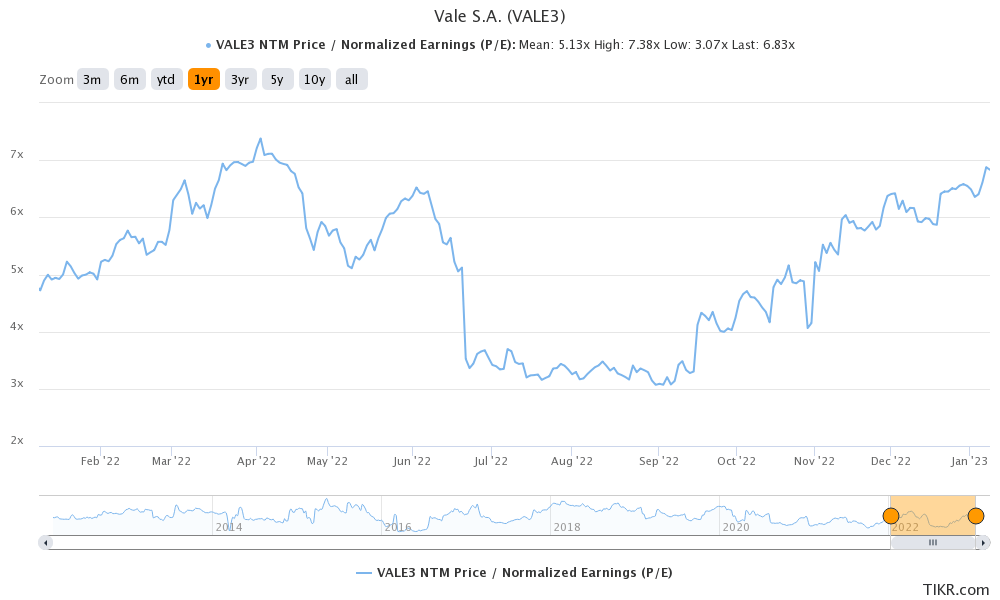

VALE 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

VALE is currently trading at an NTM P/E of 6.83x, in line with its 3Y pre-pandemic mean of 6.80x though higher than its 1Y mean of 5.0x.

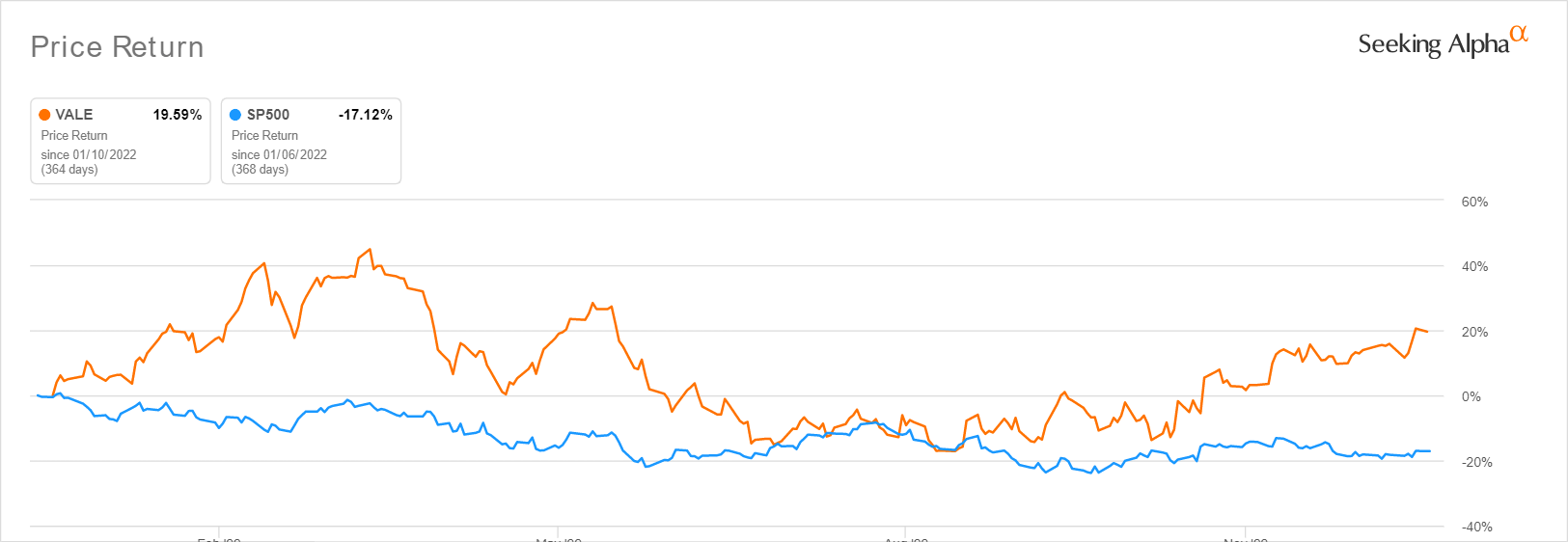

VALE 1Y Stock Price

Seeking Alpha

Based on VALE’s projected FY2024 EPS of $2.30 and current P/E valuations, we are looking at a moderate price target of $15.70. While consensus estimates are more bullish, with a price target of $19.20, there appears to be limited upside potential from current levels indeed. Though China’s intermediate demand for iron ore may surge, the optimism is probably already baked in its valuation, attributed to the impressive 49.5% stock recovery since September bottom.

Depending on how things develop over the next few years with the contrarian rebound in Chinese demand and global recessionary fears, VALE may likely remain volatile as well. For now, market analysts are prudently projecting FY2024 revenues of $39.58B and EPS of $2.45, with Free Cash Flow generations of $8.9B at the same time. However, investors must note that its dividend payouts may be impacted, due to the separation of its iron ore and copper/nickel business, possibly triggering dividend payouts of $0.86 by FY2024. This suggests yields of 4.9% against its 4Y average of 7.53% and sector median of 2.12%.

In the meantime, we prefer to rate the VALE stock as a Hold for now, due to the reduced margin of safety. Do not chase this rally.

Be the first to comment