Bill Oxford

Earnings of PennyMac Financial Services, Inc. (NYSE:PFSI) will plunge this year mostly because of lower mortgage production amid a rising interest-rate environment. However, the mortgage servicing division will likely benefit from higher interest rates. Further, income from the investment management division will likely remain stable, which will offer some support to the bottom line. Overall, I’m expecting PennyMac Financial to report earnings of around $6.13 per share for 2022, down 58% year-over-year. The year-end target price is somewhat close to the current market price. Hence, I’m adopting a hold rating on PennyMac Financial Services.

Mortgage Banking Industry Making a Harder Landing than Expected

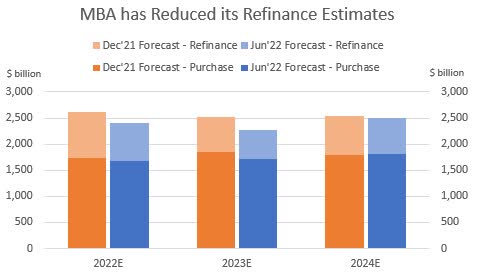

The mortgage refinancing volume appears on track for a harder landing than previously expected. The Mortgage Bankers Association (“MBA”) has materially revised downwards its refinancing expectation for both 2022 and 2023. In June 2022, MBA estimated a refinancing volume of $1,681 billion for 2022, down 3% from the estimate given in December of 2021.

Mortgage Bankers Association

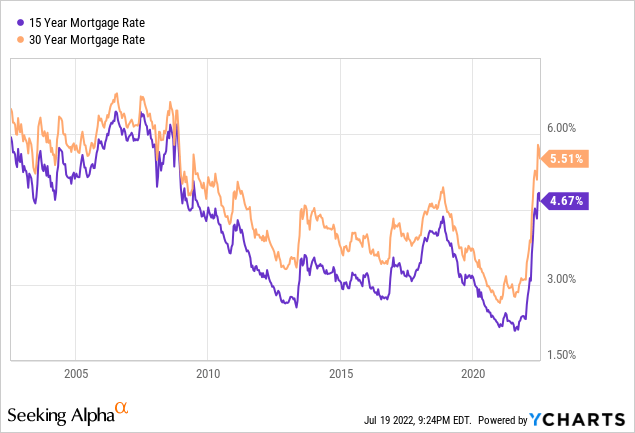

The plunge in refinancing volume witnessed so far this year is mostly attributable to the sooner and greater-than-expected monetary tightening. In December 2021, the Federal Reserve projected the Fed Funds target rate to be around 0.9% (median) for 2022. As per the latest report, the Fed is now projecting a target fed funds rate of around 3.4% for 2022. Due to the steep trend of the fed funds rate, mortgage rates are at multi-year highs, as shown below.

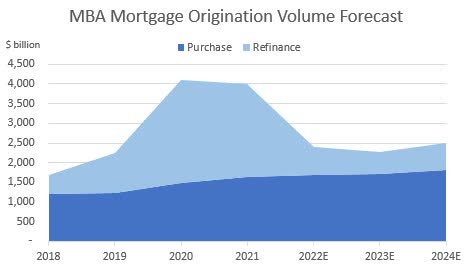

MBA is now projecting the total mortgage origination volume, including refinancing volume, to decline by a whopping 40% year-over-year in 2022.

Mortgage Bankers Association

Company-specific Factors Provide a Brighter Outlook

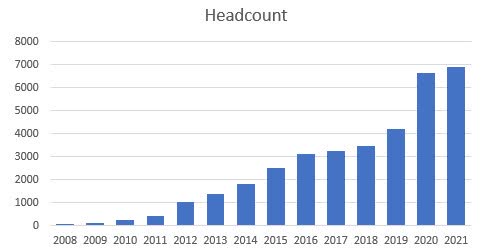

Although refinancing volume will almost return to the 2018 level this year (see chart above), PennyMac Financial Services’ share of that refinancing market will most probably not return to the 2018 level. This is because the company has significantly expanded its team size since 2018, as shown below. The greater human resource will help boost PennyMac’s share of the mortgage market.

Earnings Presentations, SEC Filings

Moreover, mortgage servicing income will benefit from higher interest rates. As can be gleaned from details given in the first quarter’s conference call, PennyMac earns interest income on its custodial deposit balances. As a result, the upward shift in short-term interest rates this year will boost the company’s revenues.

Further, revenues from the investment management division will likely remain stable. Under the investment management division, PennyMac Financial manages PennyMac Mortgage Investment Trust (NYSE: PMT), a mortgage REIT. The 2022 consensus earnings estimate for PMT can be seen on Seeking Alpha’s earnings page.

Expecting Earnings to Dip by 58%

Considering the industry-wide and company-specific outlook, I’m expecting PennyMac’s total net revenues to decline by 38% year-over-year in 2022. Meanwhile, the margin will likely continue to decline, but it’ll receive some support from cost control efforts, as mentioned in the conference call. Overall, I’m expecting PennyMac Financial Services to report earnings of $6.13 per share, down 58% year-over-year. The following table shows my income statement estimates.

| 2017 | 2018 | 2019 | 2020 | 2021 | 2022E | |

| Financial Summary | ||||||

| Total Net Revenues | 955 | 985 | 1,477 | 3,706 | 3,167 | 1,957 |

| Expenses | 630 | 717 | 948 | 1,465 | 1,808 | 1,465 |

| Profit Before Tax | 326 | 268 | 529 | 2,241 | 1,359 | 491 |

| Net Income for Common Sh. | 101 | 92 | 393 | 1,647 | 1,003 | 362 |

| EPS – Diluted ($) | 4.0 | 2.6 | 4.9 | 20.9 | 14.7 | 6.1 |

|

Source: SEC Filings, Author’s Estimates (In USD million except per share items) |

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a recession can make people postpone their home purchases, which could make the revenue fall by more than my expectation. The new Omicron subvariant also bears monitoring.

Adopting a Hold Rating

Compared to its peers (selected by market capitalization), PennyMac Financial is somewhat cheap on the price-to-earnings and price-to-book multiples. The following table summarizes data on valuation multiples provided by Seeking Alpha.

| PFSI | Peer Avg. | WSFS | CLBK | COOP | AX | OTCQB:FMCC | |

| Peer Comparison | |||||||

| Price-to-Earnings (“TTM”) | 3.9 | 11.3 | 9.9 | 24.7 | 2.1 | 9.6 | 10.2 |

| Price-to-Earnings (“FWD”) | 7.3 | 10.2 | 12.4 | 25.9 | 3.3 | 9.4 | 0.3 |

| Price-to-Book (“TTM”) | 0.8 | 1.4 | 1.0 | 2.2 | 0.7 | 1.4 | NM |

| Source: Seeking Alpha |

PennyMac Financial is offering a dividend yield of 1.6% at the current quarterly dividend rate of $0.20 per share. The earnings and dividend estimates suggest a payout ratio of 13% for 2022, which is easily sustainable. Therefore, the earnings outlook presents no threats to the level of dividend payout.

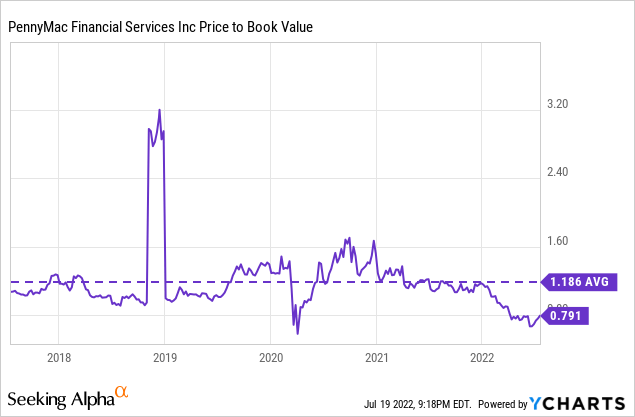

I’m using the historical price-to-book (“P/B”) and price-to-earnings (“P/E”) multiples to value PennyMac Financial. The stock has traded at an average P/B ratio of 1.186x in the past, as shown below.

Multiplying the average P/B multiple with the forecast book value per share of $64.8 gives a target price of $76.8 for the end of 2022. (I have estimated the book value per share for December 2022 by adding the earnings estimate and subtracting the dividend estimate from the December 2021 book value per share.) The price target implies a 53.7% upside from the July 19 closing price. The following table shows the sensitivity of the target price to the P/B ratio.

| Price-to-Book | 0.99 | 1.09 | 1.19 | 1.29 | 1.39 |

| BVPS – Dec 2022 ($) | 64.8 | 64.8 | 64.8 | 64.8 | 64.8 |

| Target Price ($) | 63.9 | 70.4 | 76.8 | 83.3 | 89.8 |

| Current Market Price ($) | 50.0 | 50.0 | 50.0 | 50.0 | 50.0 |

| Upside/(Downside) | 27.8% | 40.7% | 53.7% | 66.7% | 79.6% |

| Source: Author’s Estimates |

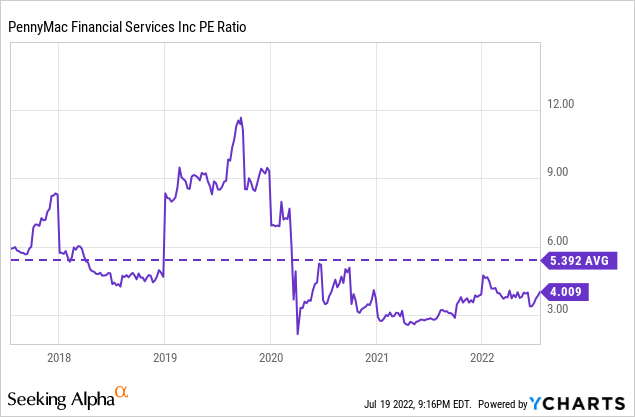

The stock has traded at an average P/E ratio of around 5.392x in the past, as shown below.

Multiplying the average P/E multiple with the forecast earnings per share of $6.1 gives a target price of $33.0 for the end of 2022. This price target implies a 33.9% downside from the July 19 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| Price-to-Earnings | 3.4 | 4.4 | 5.4 | 6.4 | 7.4 |

| EPS – 2022 ($) | 6.1 | 6.1 | 6.1 | 6.1 | 6.1 |

| Target Price ($) | 20.8 | 26.9 | 33.0 | 39.2 | 45.3 |

| Current Market Price ($) | 50.0 | 50.0 | 50.0 | 50.0 | 50.0 |

| Upside/(Downside) | (58.4)% | (46.2)% | (33.9)% | (21.6)% | (9.4)% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $54.9, which implies a 9.9% upside from the current market price. Adding the forward dividend yield gives a total expected return of 11.5%. As this expected return is not high enough for me, I’m adopting a hold rating on PennyMac Financial Services.

Be the first to comment