In addition to Tesla, we continue to have high conviction in the ability of our other core holdings to outperform. Despite the stock’s underperformance year-to-date, we include Spotify in that cohort.

At its June investor event, Spotify reiterated its long-term goal of reaching 1 billion users by 2030, driving $100 billion in revenue with 20% operating margins. We believe these goals are not only achievable but could prove to be conservative in the long run. The company is building what it is calling “The Spotify Machine,” a sort of reinforcement feedback loop of growth, new users, new creators, and new high-margin monetization opportunities.

We believe Spotify’s business model will work best at truly global scale, and we believe the company is still in the early days of growth. To be clear, we don’t expect the company to generate excessive profits in the short-term as we believe the company should reinvest all available capital into growth and territory expansion. It’s also worth noting that Spotify is free cash flow positive and has a strong balance sheet-this reduces the likelihood of further share dilution and lowers near-term risk as shareholders.

As investors, we tend to look at our portfolio as one might look at a group of bananas: Some are yellow and ripe and ready to eat now, and others are green and will take some time to ripen. Spotify is a green banana.

At scale, Spotify will command significant leverage to increase revenues through re-negotiation with labels, subscription price increases, and other high-margin monetization strategies that have yet to launch, but are in the product pipeline (e.g. audiobooks, paid podcasts, live audio, events, ticketing, etc.). We believe Spotify’s market value today (~$20b) represents one of the more extreme mismatches between price and value in the market.

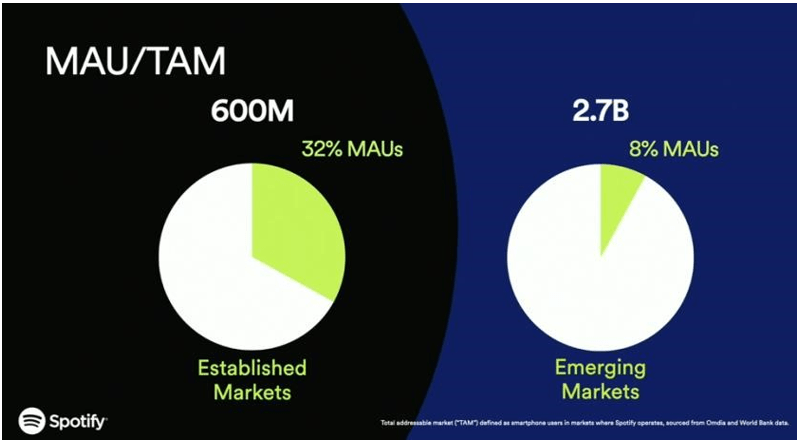

There are many ways to value a company, but in any risk-off market environment, valuations tend to compress for any company that does not generate near-term profits. However, in our experience, sentiment can shift rapidly on a company like Spotify. Our valuation methodology for Spotify focuses primarily on global user growth, market expansion, and platform monetization that we believe will enable a geyser of free cash flow. At 422 million active users growing roughly 20% a year, we are well on our way.

What’s often missed about Spotify’s monetization strategy is that it is not one-dimensional. For Spotify, getting more content onto the platform (especially non-music content) is helping to build a powerful reinforcement loop to attract new users-and new advertisers. As we note below, advertising will be a large driver of gross profit and net income over the long-term, and yet we believe most Wall Street analysis tends to underemphasize this growth driver. As Spotify’s Chief Content Officer said at the Investor Day, “gone are the days of ads accounting for less than 10% of Spotify’s total revenue.”

Below are a few of our observations from the event:

The TAM is objectively massive – We believe MAU growth still has a huge amount of runway, and Spotify reiterated its 1B MAU target by 2030 (from ~420mm today). At scale, this enables enormous leverage to increase revenues through re-negotiation with labels, price hikes, and other high-margin monetization strategies that have yet to launch (audiobooks, paid podcasts, live events, ticketing, etc.)

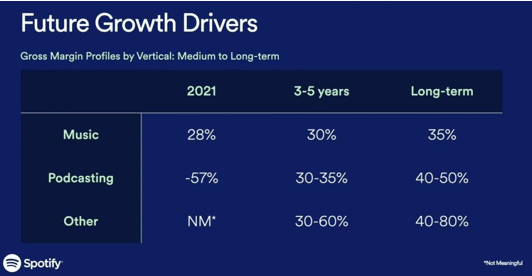

Spotify continues to invest its capital into growth of the product, which we think will lead to very attractive margins at scale. Right now, the podcast business is still a drag on consolidated gross margins, but that’s because it’s in the early stages of growth and there are significant costs to acquire content and build out podcast infrastructure. The strategy is working, which improves the LTV of users and adds incremental value back to the platform, which is why we’re excited about the reinvestment of capital.

At the Investor Day, Spotify shared that 7% of listening hours on its platform are podcast hours (up from ~1% in 2018), and of those podcast hours only 14% are monetized today. At scale, podcasting could reach a 50% gross margin business – a margin profile that is not reflected in today’s value.

We believe Spotify’s advertising platform growth is akin to Facebook’s mobile ad program circa 2012 or even Google AdWords in its early days. Spotify’s advertising business used to be a non-essential part of our thesis. Now, it’s clear that advertising growth is going to be a big driver of both revenue and margin over the next several years. We are in the very early innings of on-demand audio advertising, but we think it has the potential to be a massive, AWS-like driver for Spotify’s core operations. Podcasts are key to driving bigger ad-spends.

“In the US, when we bundle music and podcast advertising, the average size of the spend on a campaign is 4 times that of a music-only campaign, so we’re driving bigger spends from advertisers and growing our revenue significantly.”-Dawn Ostroff

Spotify’s music Marketplace is a real tech business – high initial capital outlay, but revenue can increase without additional investment, giving it a high long-term profit potential. One of the major knocks on Spotify is that it pays out too much to music rightsholders, but we can see that its marketplace business is driving rapid gross profit growth. Management now expects Marketplace gross margin to increase 30%+ this year, and continue to grow at healthy double-digits.

“In 2018 our Marketplace contribution to gross profit was only $20 million. In 2021 it grew to $160 million, 8x the size in just four years. We expect that number to increase another 30% or more in 2022. We see tremendous upside in Marketplace, and anticipate that its financial contribution will continue to grow at a healthy double-digit rate in the years ahead. Marketplace is the quintessential example of our approach to capital allocation. There was a significant up- front cost to build-and-launch these offerings, but we saw compelling data which gave us the confidence to double-down and invest aggressively against our goals.”- Paul Vogel, CFO

Revenue, margin targets, price targets. In the next decade, Spotify’s goal is to generate $100b in revenue and achieve 40% gross margins at scale, with a 20% operating margin. We think this goal is not only achievable, but perhaps even conservative, should any of the company’s new high-margin initiatives (advertising platform, audiobooks, etc.) take off faster than anticipated. Even on a shorter-term basis, we think the stock is fundamentally mispriced – at a time when the future looks very bright for the core business, shares are down some 65% from highs – which we see as a temporary dislocation of price and value. Even on a conservative basis and with a recognition of the challenging macro environment, we think the stock should be on a path to 10x over the next several years, driven purely by improving fundamentals and earnings growth. By 2024/2025, we think it’s likely that Spotify will be achieving significant positive earnings- growing at more than 50%-far beyond consensus expectations.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment