Antonio_Diaz/iStock via Getty Images

Its Lowered Guidance Does Not Inspire Confidence, Unfortunately

Target Corporation (NYSE:TGT) previously reported underperforming gross margins of 25.8% and operating margins of 3.9% in FQ3’22, notably declining by -3.2 and -4 percentage points YoY, respectively. While those numbers have shown QoQ improvements of 3.2 and 2.6 percentage points, respectively, management’s lowered FQ4’22 guidance of 3% operating margins does not inspire confidence indeed. Especially, since it has previously delivered consistent pre-pandemic operating margins of ~6% and hyper-pandemic levels of ~10%.

Part of these headwinds have been attributed to the rising inflationary pressure on discretionary spending, as shared by Brian Cornell, the CEO of TGT, during its previous earnings call:

With high rates of inflation contouring the road, their purchasing power, many consumers this year have relied on borrowing or dipping into their savings to manage their weekly budgets… As a result, our guests are exhibiting increasing price sensitivity, becoming more focused on and responsive to promotions and more hesitant to purchase at full price. (Seeking Alpha)

However, the biggest culprit will be TGT’s record-high inventory levels of $17.1B in FQ3’22, growing by 11.6%/$1.79B QoQ, 14.4%/$2.16B YoY, and 50.2%/$5.72B from FQ3’19 levels. It appears that the management has overestimated consumer demand, leading to overstocking. As a result, it is unsurprising the company had to clear inventory through multiple markdown sales by the end of 2022, compressing its margins in the short term. While the calendar year-end has always been the company’s strongest quarter, the tougher YoY comparison may pose further headwinds in its upcoming earnings call, with the consumer holiday spending trends looking unpromising.

In the meantime, TGT’s balance sheet is deteriorating rapidly, with declining cash/ investments of $1B and growing long-term debts of $14.38B in FQ3’22. These numbers indicate a drastic decline of -12.5% QoQ/ -82.5% YoY and an expansion of 6.9% QoQ/ 24.1% YoY, respectively. Notably, the latter has increased its annual interest expenses by 7.1% to $453M over the LTM, as well.

Oddly, the TGT management also chose to increase its dividends paid out by 18.8% QoQ/ 12.9% YoY to $497M in the latest quarter, while similarly increasing its capital expenditure by 14.6% QoQ/ 57.8% YoY to $1.8B. These numbers are not encouraging, since the company has also been generating negative Free Cash Flow [FCF] for the past three quarters.

While TGT has guided a total savings of up to $3B over the next three years (to be further discussed in the upcoming earnings call), it remains to be seen how the management expects to turn the business around. The Feds’ recent meeting minutes suggest that interest rates may be raised to over 5% by mid-2023, with a pivot only occurring from 2024 onwards.

We are already seeing some signs of declining consumer spending, with the November CPI showing a reduced index for commodities (less food and energy) at -0.5% sequentially, compared to 0.8% in June 2022. The food (at home) index is similarly decelerating to 0.5%, compared to 1% in June 2022. These points to more uncertainty and volatility over the next few quarters, as the company grapple with slowing consumer demand, elevated long-term debts/ inventory, declining financial health, and finally, compressed margins.

The Anti-Theft Solution May Impact TGT’s Consumer Base As Well

Over the past few quarters, TGT has also been reporting massive theft headwinds, potentially affecting its gross margins by $600M for 2022. This is equivalent to a 0.56% shrink, translating into a lower in-store inventory level than recorded in the system. The impact is massive indeed, since the number represents a tremendous YoY expansion in losses by 50%, exacerbated by the factors discussed above.

The same issue has been reported by Walmart (WMT), costing the company up to $3B in annual losses since 2015 at a 1% shrink, though interestingly, lesser for Costco (COST) at $272M/ a 0.12% of shrink. Investors interested in COST’s anti-theft strategies may refer to this interesting article here.

Notably, the issue of inventory shrink has cost US retailers up to $100B in 2021, emphasizing the importance of a swift solution. TGT’s answer has proven to be the new rollout of a cart-control system by Gatekeeper (OTCPK:GKPRF), a shopping cart loss-prevention provider, which serves 47 of the 50 largest global retailers. The latter claims that its systems may save retailers up to $15K annually on cart retrieval, maintenance, and replacement.

However, early consumer responses have been less than pleasant, due to the geofence system locking the use of TGT’s carts beyond the store property. Many exasperated consumers have been forced to drag locked carts across carparks, notably slowing down traffic. Joe Budano, CEO of Indyme (retail security devices) has historically witnessed a significant counter-effect of up to a -25% decline in retail sales afterward, which arises from the negative in-store shopping experiences. Frustrated consumers have been found to shop at other retailers or opting for e-commerce instead.

TGT has similarly offered an e-commerce segment indeed. However, its digital comparable sales growth has been decelerating YoY from 30% in FQ3’21, to 9% in FQ2’22, and finally to 0.3% by FQ3’22, normalizing from its hyper-pandemic levels. On the other hand, investors may be encouraged by the fact that digital sales now represent up to 20% of the company’s business, compared to 10% in the previous quarter. With the anti-theft feature only launched in December 2022, there are also many opportunities in enhancing the consumer experience, potentially mitigating consumer migration.

Only time will tell, since e-commerce sales in the US have also burgeoned at a much faster rate by 63.9% since 2019. Notably, Amazon (AMZN) still commands the largest market share at 37.8% by June 2022, easily dwarfing TGT at 2.1% by multiple times over.

So, Is TGT Stock A Buy, Sell, or Hold?

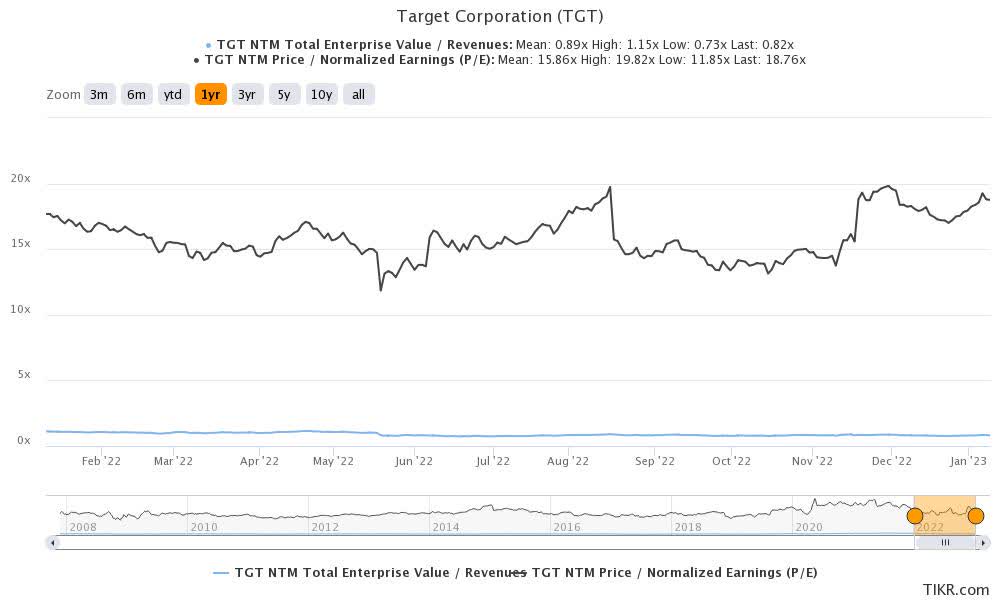

TGT 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

TGT is currently trading at an EV/NTM Revenue of 0.82x and NTM P/E of 18.76x, higher than its 3Y pre-pandemic mean of 0.69x and 14.18x, respectively. Otherwise, it is still higher against its 1Y P/E mean of 15.86x.

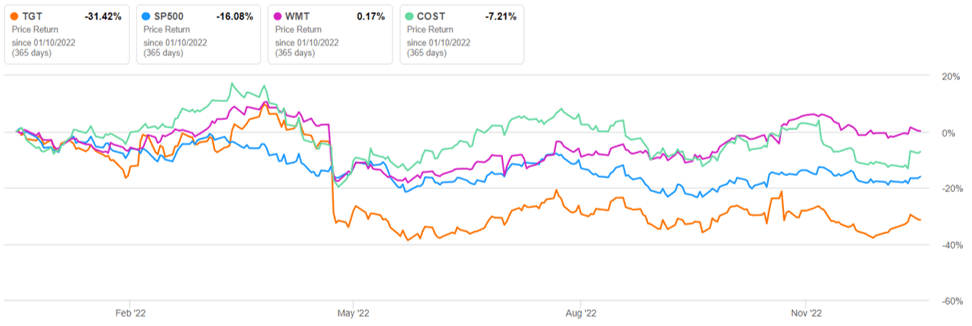

TGT 1Y Stock Price

Seeking Alpha

While things may improve from 2024 onwards, TGT’s short-term outlook looks unpromising, attributed to the management’s lowered guidance. This is naturally reflected in its stock price, trading sideways since its tragic plunge in May 2022. As a result, it made sense that the consensus estimates project a price target of $177.53, suggesting a minimal 13.82% upside potential from current levels. Market analysts also project a pessimistic revenue CAGR of 2.3%, EPS CAGR of -5.6%, and FCF CAGR of -8% through FY2025, naturally explaining the price target’s stark difference from the hyper-pandemic high of $249.32.

On the other hand, the TGT stock is already trading with massive baked-in pessimism with a moderate support level at the $140s, suggesting its minimal downside potential. Based on its projected dividend payout of $4.30 in FY2024, opportunistic investors may also enjoy expanded yields of 3.1% at those levels, against its 4Y average of 2.07% and sector median of 2.10%.

As a result, existing TGT investors looking to drip may be interested at that entry point, since it will provide an improved margin of safety at 26.8%. Naturally, this assumes that adding will result in a lower dollar cost average.

Be the first to comment