asbe

Introduction

The aftermath of the Russian invasion of Ukraine saw Europe scrambling to find natural gas outside of Russia, which was a game-changer for the United States producers, along with their associated service providers. As such, it appeared the worst was over for USA Compression Partners (NYSE:USAC) with my previous article seeing their recovery gaining momentum and helping their unit price rally. When looking into 2023, there should be more upside potential as the narrative changes with management shifting their outlook towards growth, both operationally speaking and possibly even in regards to their distributions.

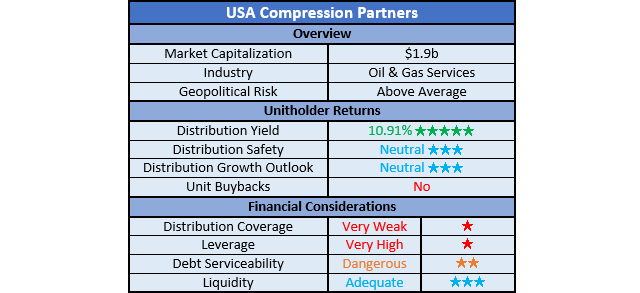

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

Author

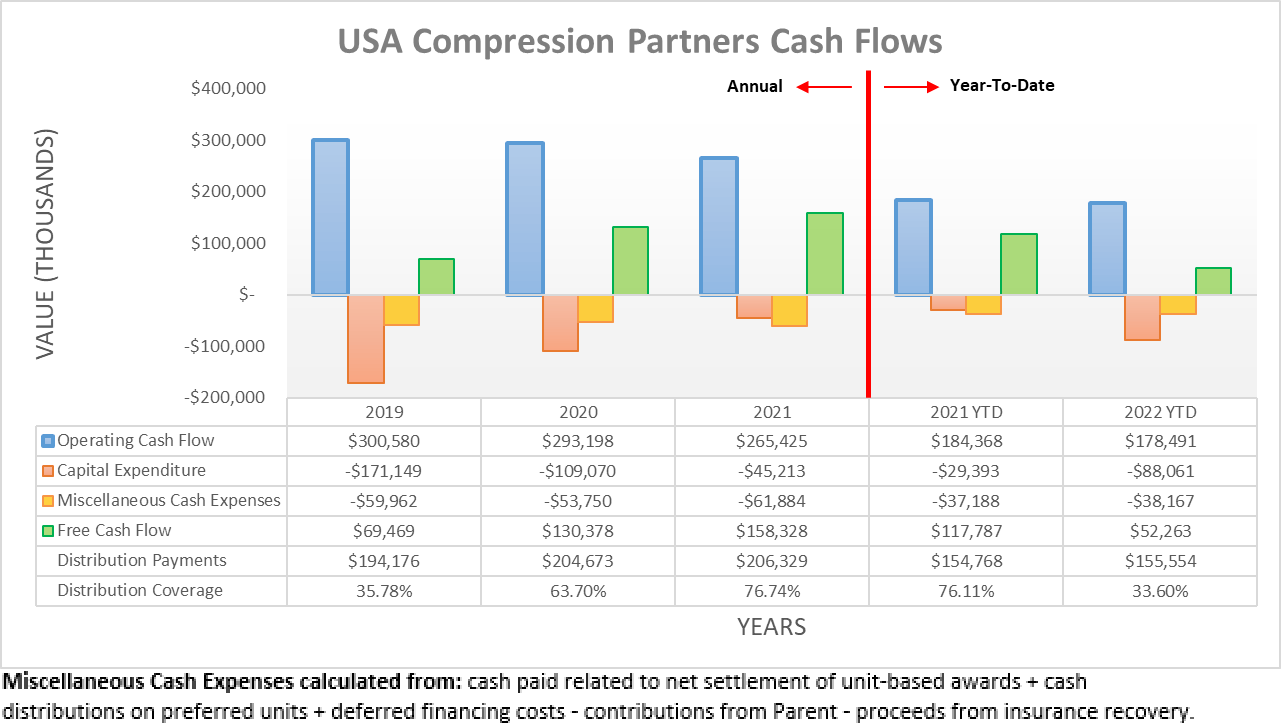

The second quarter of 2022 saw their recovery gaining momentum and whilst exciting and positive, it actually raised the stakes for the third quarter. If their cash flow performance was to slip lower once again, it would raise concerns that the second quarter was merely a blip on the radar. When first opening their results, their operating cash flow landed at $178.5m during the first nine months of 2022, thereby down only a minor amount versus their previous result of $184.4m during the first nine months of 2021. Whilst still down $5.9m year-on-year, this is still less in both absolute and relative terms than the $9.8m gap year-on-year following the first half of 2022, thereby implying a sustained recovery.

Author

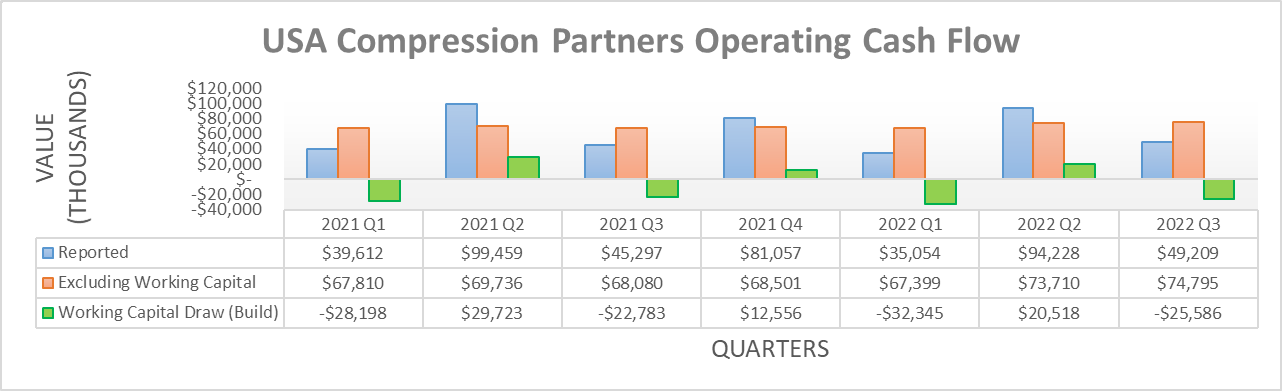

Thankfully, zooming down into their quarterly operating cash flow confirms their recovery was sustained during the third quarter of 2022. Whilst their reported operating cash flow was only $49.2m, it was still up almost 9% year-on-year versus their previous result of $45.3m during the third quarter of 2021. If excluding their working capital movements, their underlying result landed at $74.8m during the third quarter of 2022 and thus the highest result since at least the beginning of 2021. Apart from surpassing their previous equivalent results of $68.1m during the third quarter of 2021, it also edges ever-so-slightly above their previous equivalent results of $73.7m during the second quarter of 2022, which formally marked their highest result in recent times. Since this shows improvements both year-on-year and sequentially, it seems the second quarter was not merely a blip on the radar with evidence of their recovery being sustained.

Even though their capital expenditure ultimately leaves their distribution coverage very weak at only 33.60% during the first nine months of 2022, their distributable cash flow still sees full coverage of 1.07, as per their third quarter of 2022 results announcement. Accordingly, it was positive to see the narrative changing from a defensive stance to instead focus on growth in the years ahead, as per the commentary from management included below.

“Our ability to deliver high quality service to our customers while maintaining capital discipline should continue driving financial performance that we expect will afford us the flexibility to dedicate future cash flows to further capital investment, debt reduction, distribution increases, or a combination of the foregoing items.”

-USA Compression Partners Q3 2022 Conference Call.

After fighting to shed costs and capital expenditure for years, they are now realigning their outlook for growth, operationally speaking. In particular, it has been a number of years since management combined the words “distribution” and “increases” together in the same sentence. Ever since the severe downturn of 2020 and 2021 struck, they were always taking a more defensive stance that left the door open for distribution cuts, as many of my previous articles covered back at the time.

As much as we know that a unit price should eventually realign with its intrinsic value in the medium to long-tern, the narrative surrounding their units nevertheless plays a role in their prices, especially in the short-term. Despite not seeing much scope for distribution growth during 2023 given their competing capital expenditure and subsequently discussed very high leverage, I nevertheless still expect the narrative changing to operational growth, rather than survival will help propel their unit price higher. Plus, as their now sustained recovery hopefully sees stronger financial performance in the year ahead, it should help improve their financial position along with their distribution coverage and thus lower risks. Furthermore, their recent inclusion into the Alerian MLP indices should help see additional demand for their units, which by extension means further prospects for a higher unit price.

Author

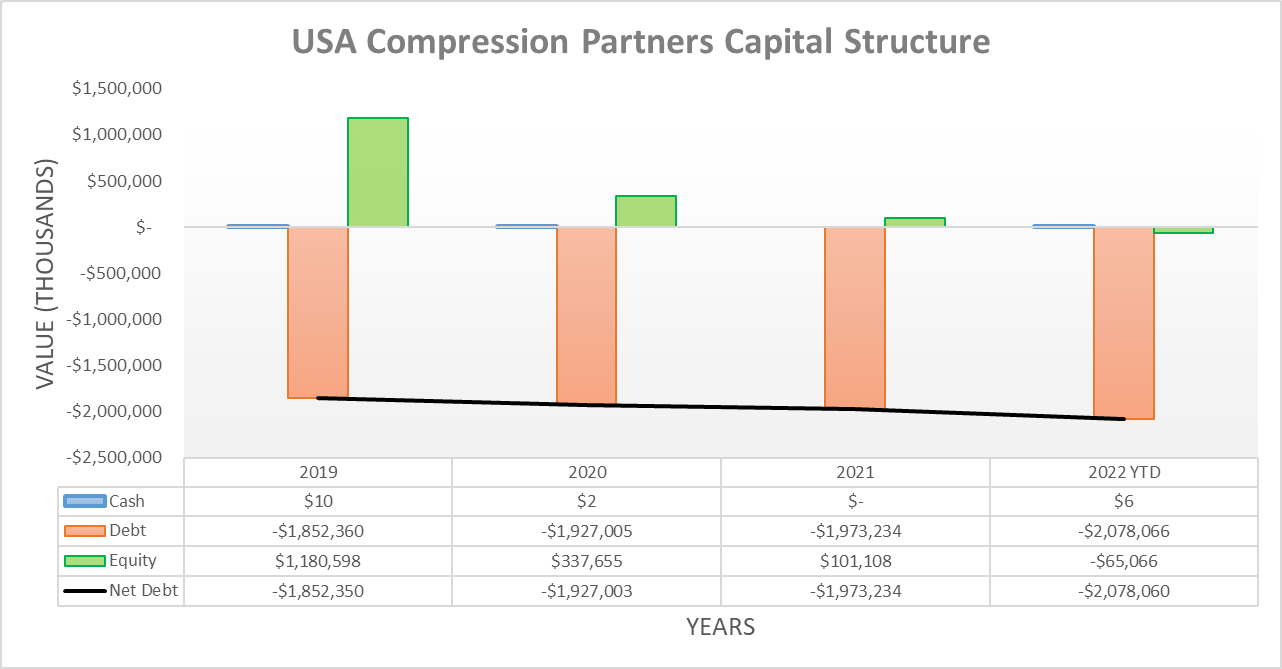

Even though their financial performance held its recovery during the third quarter of 2022, their net debt still edged higher, in part due to their working capital build. At least the increase was only small with its latest level at $2.078b versus its previous level of $2.017b following the second quarter. Since this barely changed, similar to their cash balance of only $6m, it would be redundant to reassess their leverage, debt serviceability and liquidity in detail.

Furthermore, their covenant leverage ratio still decreased to 4.84 versus its previous result of 4.90 following the second quarter of 2022, as per their previously linked third quarter of 2022 conference call. In this particular situation, the single most important element when it comes to sustaining their distributions is seeing this number stay beneath the covenant limit of 5.25 for their credit facility.

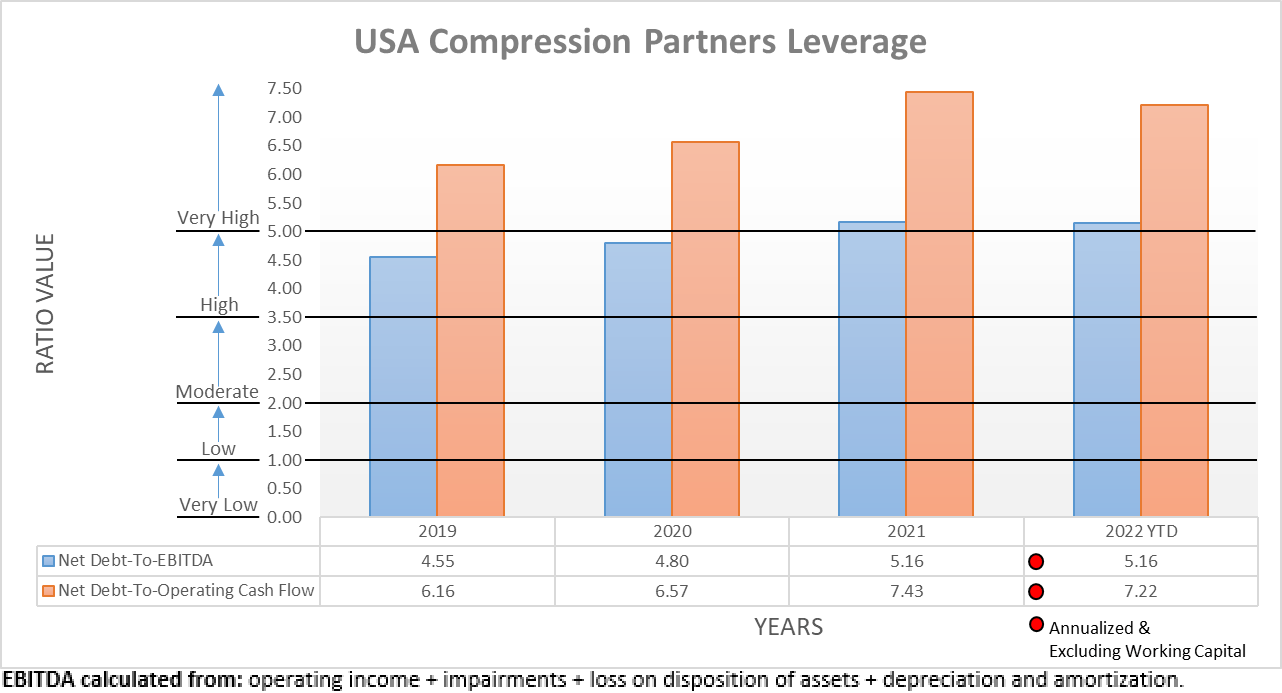

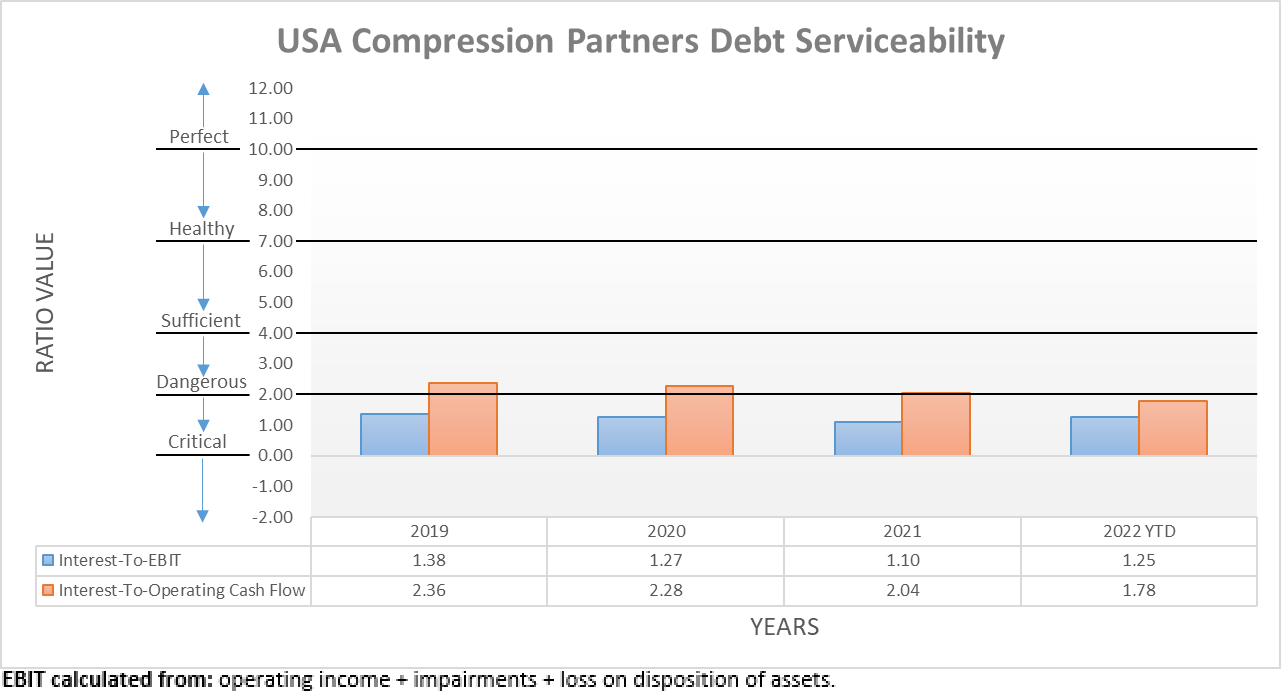

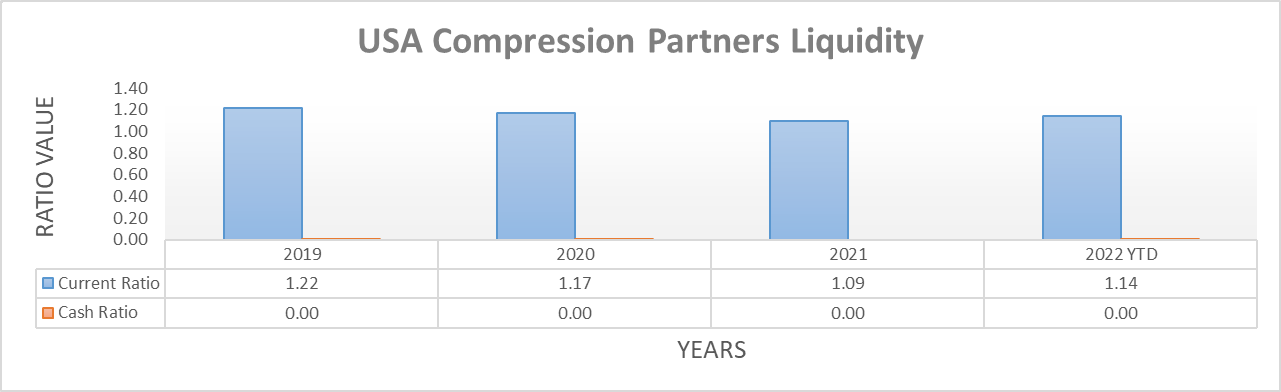

The three relevant graphs are still included below to provide context for any new readers, which shows their leverage is unsurprisingly still very high with a net debt-to-EBITDA of 5.16, plus an accompanying net debt-to-operating cash flow of 7.22. Accordingly, it was only a given their debt serviceability would remain under pressure, as their interest coverage is only a dangerous 1.25 and 1.78 when compared against their EBIT and operating cash flow, respectively. At least their one saving grace remains their adequate liquidity, which sports a current ratio of 1.14 that makes up for their essentially non-existent cash balance and its resulting cash ratio of 0.00. If interested in further details regarding these topics, please refer to my previously linked article.

Author Author Author

Conclusion

When looking into 2023, as the narrative changes from a defensive stance and questions of whether their distributions will be cut to instead focus on growth, I expect their unit price will continue rallying higher, especially given the obvious appeal of their double-digit distribution yield. Despite certainly not being a low-risk investment, their very high leverage and distribution coverage should improve as their financial performance continues its recovery on the back of higher natural gas production in the United States following the Russia-Ukraine war. When wrapped together with evidence of their recovery being sustained, I see no reason to believe that I should change my rating and thus, I once again feel my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from USA Compression Partners’ SEC Filings, all calculated figures were performed by the author.

Be the first to comment