As an Upstart (NASDAQ:UPST) investor, I’m rooting for the good, preparing for the bad, and positioning for the ugly.

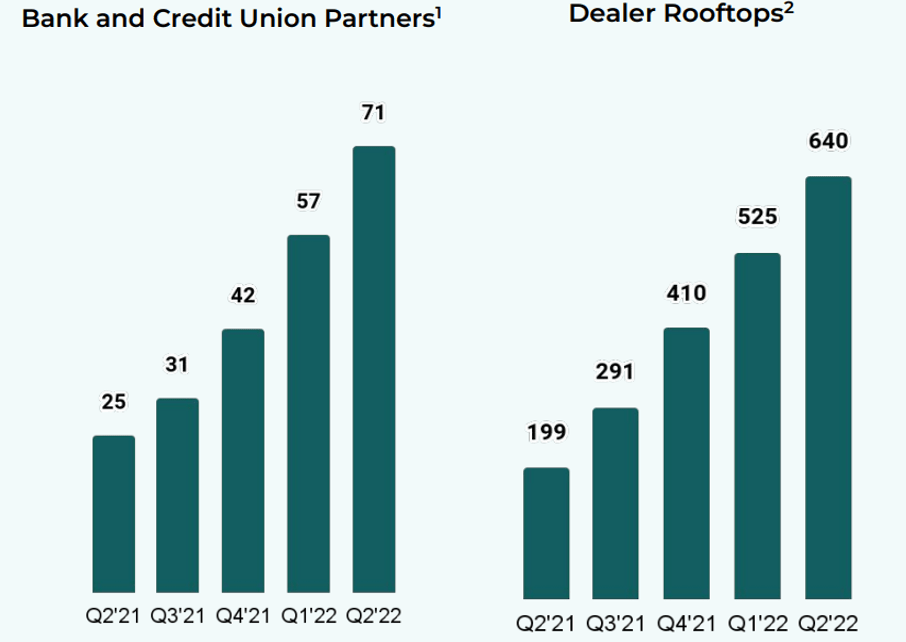

The Good: Upstart is suffering a violent contraction in lending volumes due to a rapidly deteriorating credit market. However, when we look under the hood, the company is still adding new partners to its AI-powered lending marketplace and expanding its presence among auto dealerships.

Even during this uncertain macroeconomic environment, Upstart adding more partners to its marketplace is setting up the company for a brighter future. When the credit cycle turns (and it will turn at some point [hopefully, in 2023]), Upstart’s business is likely to come back stronger than ever (if its credit performance holds up well).

In the meantime, Upstart’s robust unit economics and low fixed cost structures are set to enable the business to remain free cash flow positive during this down cycle. With $800M of cash on its balance sheet, Upstart has enough firepower to survive through these tumultuous macroeconomic conditions.

The Bad: Upstart’s lending marketplace is funding constrained, and according to recent commentary from the company’s C-suite, Upstart’s funding partners are still being risk averse (homogeneously), and no progress has been made on securing committed funding for their marketplace (plans announced in Q2 earnings call). In fact, the management admitted during recent conferences that the committed funding plan is something for the next downturn in debt markets.

Links to recent conferences held in mid-September:

With funding partners and institutional investors bailing on Upstart, its volumes could remain in free fall until the credit cycle turns (and that’s likely not happening until the Fed pivots).

The Ugly: In my analysis of Upstart’s Q2 results, I highlighted the fact that its credit performance data for 2021 cohorts was unimpressive. And recent data from KBRA shows that many of Upstart’s ABS securitization trusts have recently suffered (or are set to suffer) trigger breaches [Current Cumulative Net Defaults [CND] > Expected CND].

KBRA news release

Upstart’s AI has never been tested in a recessionary environment, and if its credit performance fails to match or outperform FICO-based loans, institutional investors and funding partners may pull back permanently from Upstart’s marketplace. In such a scenario, Upstart will not be able to scale due to the limitations of its balance sheet. The company’s long-term future will then be as a financial lending institution, similar to LendingClub (LC) or SoFi (SOFI). Again, this doesn’t mean Upstart would be a bad business; it would just be a very different business than what Upstart’s management has set out to build. The valuation would look a lot different too, but more on that later.

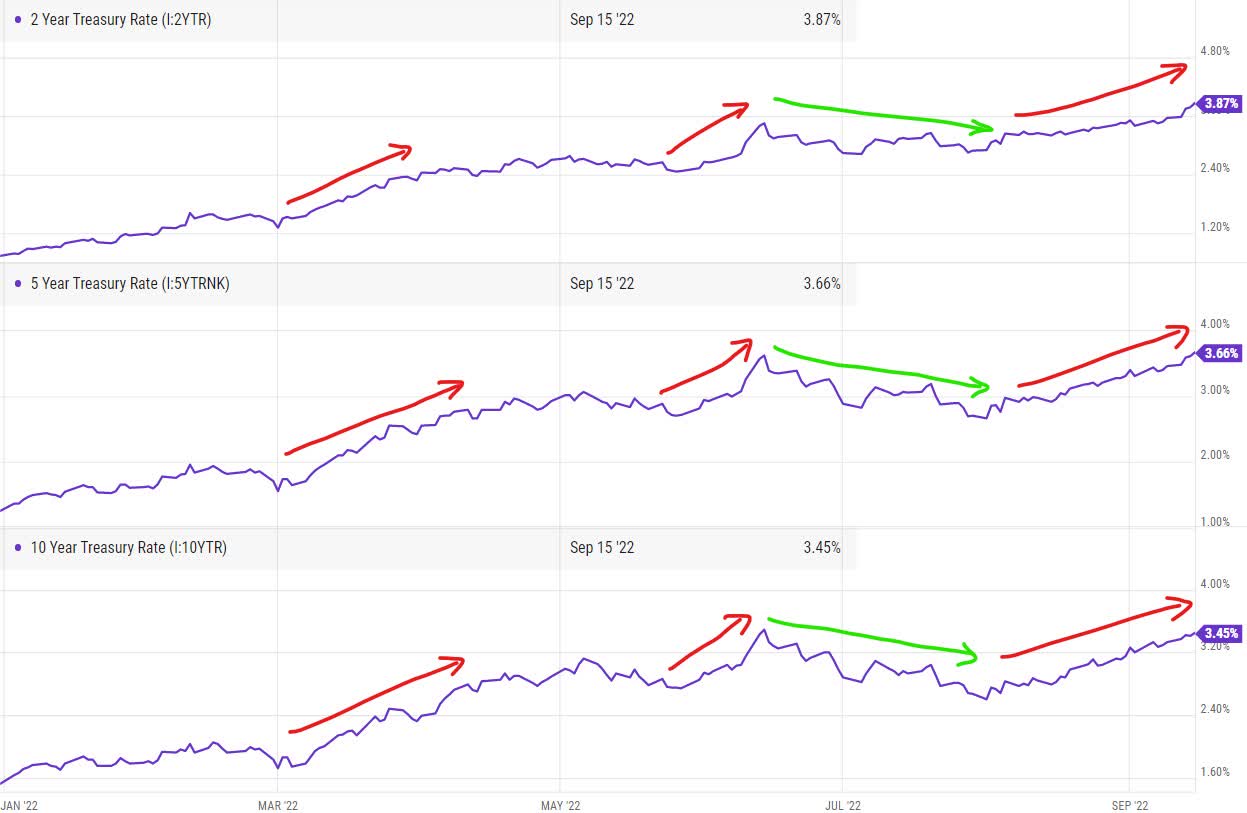

In the first half of Q3, Upstart’s business would have gotten some relief as interest moderated somewhat; however, the second half of Q3 saw surging interest rates, as shown in the chart below. As of writing, the 2-yr treasury yield is inching towards 4%, and the 10-yr treasury yield is ~3.6%.

US Treasury Yields (YCharts)

Inflation readings are coming in hot despite consumer sentiment being down in the dumps, and the yield curve inversion is pointing towards a potential recession. Honestly, I think that Upstart’s credit performance data is set to get worse over coming quarters as it would for almost all lending institutions amid an unprecedented quantitative tightening from central banks across the globe.

If Upstart’s credit performance is better than peers during the next few quarters, we will see a sharp recovery in its marketplace lending volumes once the credit cycle turns. However, if Upstart’s relative performance is not better than peers, we may be left with a slow to no growth, digital-lending fintech business (with no bank charter [i.e., high-cost structure]). Upstart’s management has presented data that shows its AI’s superior risk separation capabilities, and the next few quarters will determine if this data is reliable.

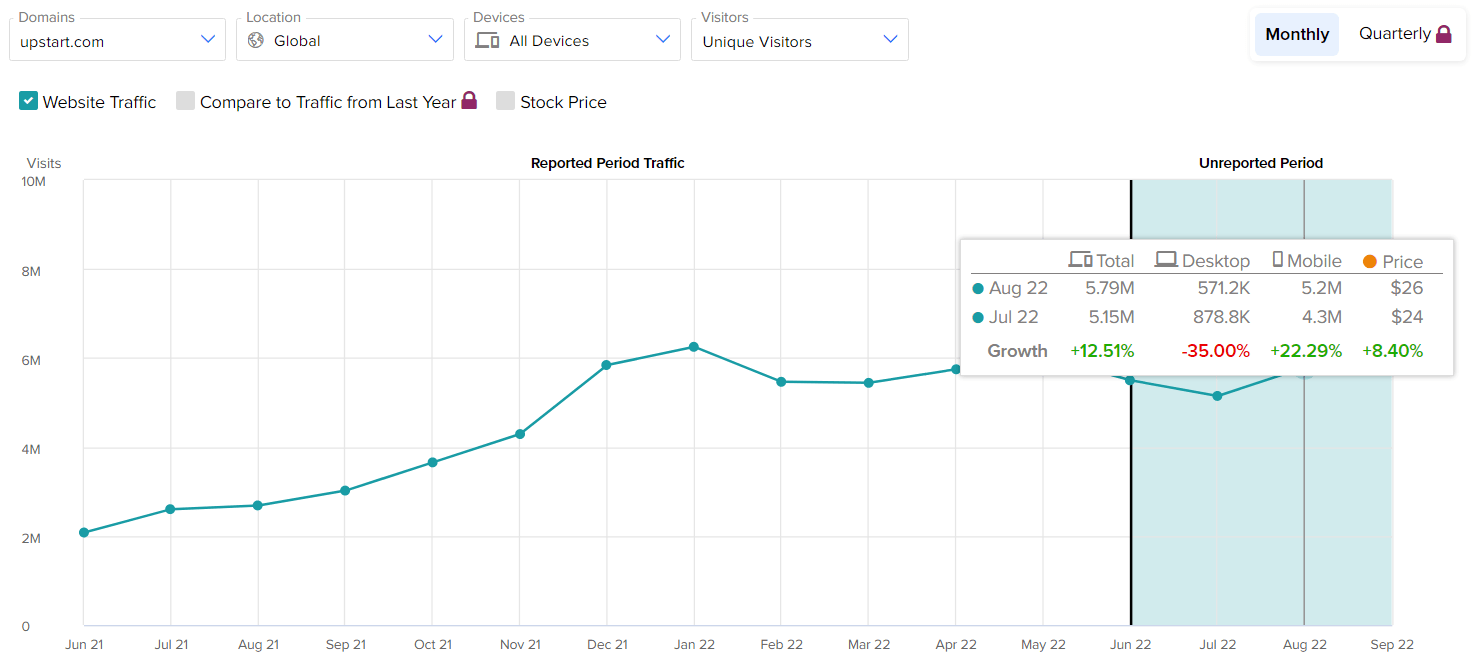

Another concerning data point I have come across is Upstart’s website traffic. While total traffic grew by 12% y/y in August, Desktop views tanked by ~35%. Rising interest rates are set to lower the demand for loans and impact Upstart’s conversion rates (as seen in Q2). As a result, Upstart’s lending activity may continue to contract for the foreseeable future.

TipRanks

With all of this information in mind, let’s re-evaluate Upstart’s intrinsic value and expected returns.

Upstart’s Fair Value And Expected Returns

To find the fair value and expected return of Upstart, we will use TQI’s Valuation model:

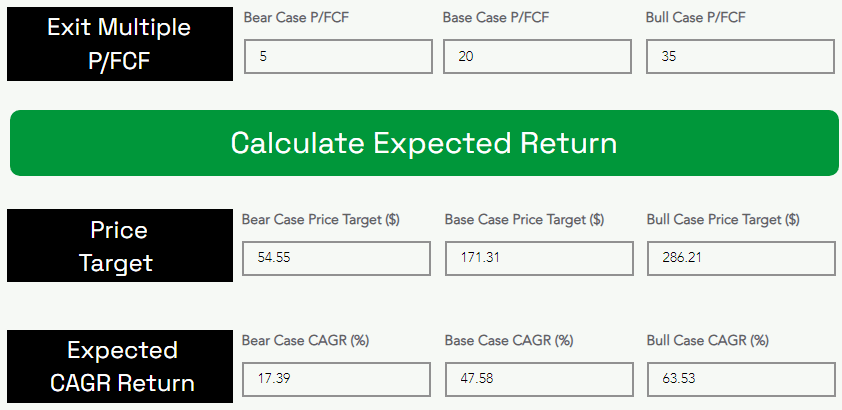

After internalizing Upstart’s Q3 revenue guidance, recent management commentary at conferences, interest rate trajectory, and website traffic data, I am cutting my revenue forecast for 2022 from $900M to $800M. All the remaining assumptions are held constant from my previous analysis.

TQI Valuation Model (tqig.org)

TQI Valuation Model (tqig.org)

In accordance with these results, I am cutting my fair value estimate for Upstart from ~$58 to ~$47 per share and reducing my 5-yr price target to $171 per share. Since these expected returns are well above my required IRR of 25% for high-risk, moonshot growth bets like Upstart, I continue to rate Upstart a ‘Strong Buy’ for long-term investors.

My Positioning For UPST

As I said at the start of this article, I am positioning for the ugly; however, before we see how that looks, let’s go over some history.

So, as you may know, Upstart has been a part of my portfolio since early 2021, and I have added to my long position on several occasions through my monthly capital allocation plans. After factoring in all my purchases, I owned Upstart at a cost basis of $78 in May 2022. My investment thesis and hedging strategy (expired in August 2022) can be found here:

While actual guidance came in worse than my bear case projections, the stock still squeezed higher. However, the horror of the Q3 guide and yet another business model pivot led me to suggest profit-booking.

Author’s note

And here’s what I wrote in my detailed review of Upstart’s Q2 earnings report:

After a strong rally going into Q2 earnings, Upstart’s stock squeezed up to $37.50; however, we have seen a sharp retracement in the stock over the last three trading sessions. On Upstart’s earnings day [8th August], I issued a buy rating on the stock at $29 per share, and while the stock is now trading below this level, I want to congratulate those who took profits on the post-ER rally.

Author’s Note

As we know, Upstart’s financial numbers are heading in the wrong direction, and the company is undergoing a business model transition. With turmoil in debt markets unlikely to end in the near term, the stock could remain volatile over the coming months. Upstart has hit turbulence, the seat belt sign is on, and all trading bets are off.

From a long-term perspective, I continue to remain bullish on Upstart. The business is still operating at breakeven FCF with robust unit economics. With ~$800M in cash, Upstart’s liquidity position is strong enough to get through this downturn in the debt markets. Once debt markets normalize, Upstart could emerge as a big beneficiary since its credit underwriting will have been war tested (i.e., proven). Personally, I have been proactively managing risk in Upstart through option-based hedging strategies; and I will continue to do so for the next couple of quarters.

On the expiry of my previous hedge (19th August 2022), I exercised my $48 Puts and bought back an equivalent number of shares over the last two weeks of August (at ~$25.6 per share). While I had the opportunity to double my position (by number of shares) in Upstart [effectively cutting my cost basis to $39 per share], I kept the excess cash to deploy into Opendoor (OPEN), Hims & Hers (HIMS), and Roku (ROKU). The reason for doing so was management’s flip-flop on Upstart’s use of the balance sheet as a bridge for loans, concerns around credit performance, and shrinking lending activity. Now, in effect, I ended up reducing my portfolio exposure to Upstart by half (it is still a double-digit portfolio weight for me). My effective cost basis for Upstart is now ~$55.5 (previously, it was $78), and I think the last hedge worked out very well.

With interest rates climbing higher and the Fed steaming forward with its quantitative tightening program, Upstart’s lending volumes may contract further in coming quarters. While I am happy with the progress Upstart is making on expanding its marketplace through the addition of partners and extension into other loan categories, the near to medium term business outlook for Upstart looks bleak.

Upstart has ample cash to survive this debt cycle downturn; however, as Upstart’s balance sheet risk increases with more loans showing up on the books, the market may choose to price it like a traditional lender. And I have outlined in my previous research notes that such a valuation (1-1.5x book value) would put Upstart’s market cap at around ~$0.8-1.2B. This figure is half of where Upstart is trading right now, and I am preparing for this sort of ugly scenario with my new hedging strategy.

For every 100 shares of Upstart, I bought 1 $25 Put, sold 1 $40 Call, and sold 2 $12.5 Puts. This hedging strategy cost me absolutely nothing (in fact, it yielded 3 cents a share); however, it limits my upside to +56% [$40], provides downside protection up to -50% [$12.5], and obligates me to double my position (by number of shares) at $12.5 per share if the share is trading below this level at expiry.

Managed Risk Portfolio (The Quantamental Investor)

Since I can exercise the $25 Put to fulfill this obligation, I am effectively gifting myself the ability to significantly reduce my cost in the event of a meltdown in Upstart’s stock. Under $12.5, I will start losing more money, but I am willing to take this risk as I still believe in the mission and vision of Upstart, and there’s a good chance this business will bounce back stronger in a new credit cycle.

The hedging strategy showcased above is implemented within “TQI’s Managed Risk Portfolio”, which is a collection of tactical positions on some of TQI’s highest conviction investment ideas, designed to deliver superior risk-adjusted returns over the next 12 months. In a vicious bear market, TQI’s Managed Risk Portfolio is our way of swinging for the fences with insurance policies limiting our downside risks.

Final Thoughts

As a long-term investor, I continue to believe in Upstart’s vision of transforming the credit industry with artificial intelligence, and I truly hope that Upstart can succeed where predecessors like LendingClub have failed. Nothing is guaranteed in investing, but Upstart is one of those generational bets that can end up disrupting a multi-trillion-dollar industry.

While Upstart is facing several headwinds, the company has enough liquidity ($800M in cash) to get through this debt cycle downturn. The fact that Upstart is not burning cash (operating near FCF breakeven) helps. If Upstart’s AI proves its ability to price credit risk better than traditional FICO-based models, we can expect explosive volume growth at Upstart over the next few years. However, investors may need to wait patiently for the credit markets to unfreeze, which may not happen until the Fed pivots (slows or reverses its quantitative tightening program). And in this period, Upstart’s management is likely to be forced into raising balance sheet risk to support lending volumes.

Marketplace funding constraints and the risk of Upstart being left holding a big bag of bad loans are sending shockwaves into Upstart’s investor base that was primarily betting on a marketplace business with massive scalability and no balance sheet risk. With the financial performance set to get worse amid rising balance sheet risk, Upstart’s stock may suffer more pain in the near term.

Considering the asymmetric risk/reward on offer, I continue to like Upstart as a long-term buy at ~$24. However, I am taking this high-risk, high-reward bet with an insurance policy, i.e., an options-based hedging strategy. Since early May, I have been hedged on most of my portfolio in a similar vein to Upstart, and this proactive risk management has enabled me to protect my wealth, increase holdings in my highest conviction ideas with little to no additional capital, and sleep well at night during this vicious bear market of 2022.

Key Takeaway: I rate Upstart a ‘Strong Buy’ for long-term investors at $24.

Thanks for reading, and happy investing. Please let me know if you have any thoughts, questions, or concerns in the comments section below or send me a direct message on SA.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment