Petmal

So much has changed since my initial buy rating on Enovix (NASDAQ:ENVX) a few months ago and this article aims to bring things up to date and revise my model and target price expectations for the company accordingly.

Investment thesis

For those who have yet to read my initial article on Enovix, I recommend reading it first before reading this follow up article as it provides a basic foundation on the fundamentals of Enovix’s business.

I think that my initial investment case for Enovix remains intact and I am seeing greater conviction with the recent second quarter. I think that Enovix could be the industry leader in silicon anode lithium ion batteries as:

- Enovix has managed to overcome the key challenges that other competitors face in bringing to market a silicon anode lithium ion battery

- The company currently has 4 strategic accounts with mega cap technology companies that validates the battery technology that Enovix brings

- Enovix is positioning itself for growth in Asia with plans for an Asia Fab and establishing key distributors in Asia

- It has an upside optionality in Enovix Mobility where it attempts to do what it has done in consumer electronics and use it for electric vehicles.

Improving commercialisation with 3 new strategic accounts

In my previous article on Enovix, I mentioned about its first strategic account, one of the top consumer electronics companies in the world putting in its first order for its high energy density smart watch. In the recent quarter, Enovix further elaborated that this strategic account has already completed the initial phases of product development and in the quarter, Enovix has recognised $5 million in revenues from this customer. I think that this is great progress for Enovix as it shows that it is not only able to attract the attention of these large strategic accounts, but also eventually actually land sales contracts.

Apart from this first strategic account, the company also announced in their second quarter results that they have also completed technology calls for 3 mega cap technology companies. This is a big deal for Enovix as it shows that their product is able to attract the interest of very large companies with market capitalisation of more than $200 billion. With these technology calls, as management has explained further, these are essentially like technology validation points for these mega cap technology companies.

While it is definitely a big catalyst for the company if any of these new 3 strategic accounts lands an actual order, I think that their commentary after these initial technology validations also further increased my conviction in Enovix’s products and technology. According to the management in the second quarter call, one of the mega cap technology company told Enovix management that their goal was to move quickly to incorporate Enovix’s technology across its portfolio of products. In addition, the other 2 mega cap technology companies also thought that Enovix was the best advanced battery that they have conducted tests on. These are encouraging initial signs for Enovix and gives me greater conviction that the best and largest customers see the great value add that Enovix’s technology can bring to their wide range of products. In addition, I think that at the present moment, there is relatively limited competition for Enovix given that its offering is considered one of the best if not the best for most of these strategic accounts.

In addition, the company increased the number of accounts in its $1.5 billion revenue funnel to 75, adding 12 new accounts in the second quarter. The total number of accounts is almost double that from one year ago in the second quarter of 2021. Design wins also increased from $371 million in the prior quarter to $414 million in the current quarter.

All these new announcements about new strategic accounts, progress in the current strategic account and improving revenue funnel and design wins bodes well for the commercialisation strategy for Enovix as demand continues to be strong and growing.

BrakeFlow technology validated by industry

Although Enovix launched BrakeFlow technology in March 2022, it caught on in the past few months with news about customers saying positive things about it. BrakeFlow technology works as a system within the cell that is effective in increasing the cell’s tolerance against thermal runaway from internal shorts and at the same time not compromise on having high energy density. As a result, BrakeFlow technology enables Enovix to bring a safer battery design to consumers. I would recommend readers who are interested in the technology to watch this video by the chairman of Enovix, T.J. Rodgers, to get a better understanding on the new technology and what it means for Enovix.

The main reason BrakeFlow caught the attention of the media and investors recently is due to the new follow-on contract that Enovix was awarded to build wearable battery cells for the US army. In particular, the CTO of Inventus Power had good things to say about Enovix’s BrakeFlow technology after their extensive testing, which I will quoted below:

Safety is a top priority at Inventus Power and when we tested the Enovix battery cells with its BrakeFlow technology, the results were impressive

…said Chris Turner, CTO of Inventus Power.

Enovix batteries are the only next-gen, high energy density cells to pass our nail penetration test. We look forward to collaborating with the company on this program, to provide an even more resilient, high-energy battery to the U.S. Army.

As such, I think that the industry is starting to take note about the new BrakeFlow technology that Enovix has announced given that it now has the validation of a company with rather vigorous testing requirements and that Enovix was the only one out of those they tested that passed the crucial nail penetration test.

I think that with BrakeFlow technology as an additional cherry on top of the cake for Enovix in terms of being a leader and having a breakthrough in lithium ion battery safety, the case for Enovix’s batteries are increasingly becoming more compelling for its key customers, especially from a safety point of view.

Operational progress and scaling up

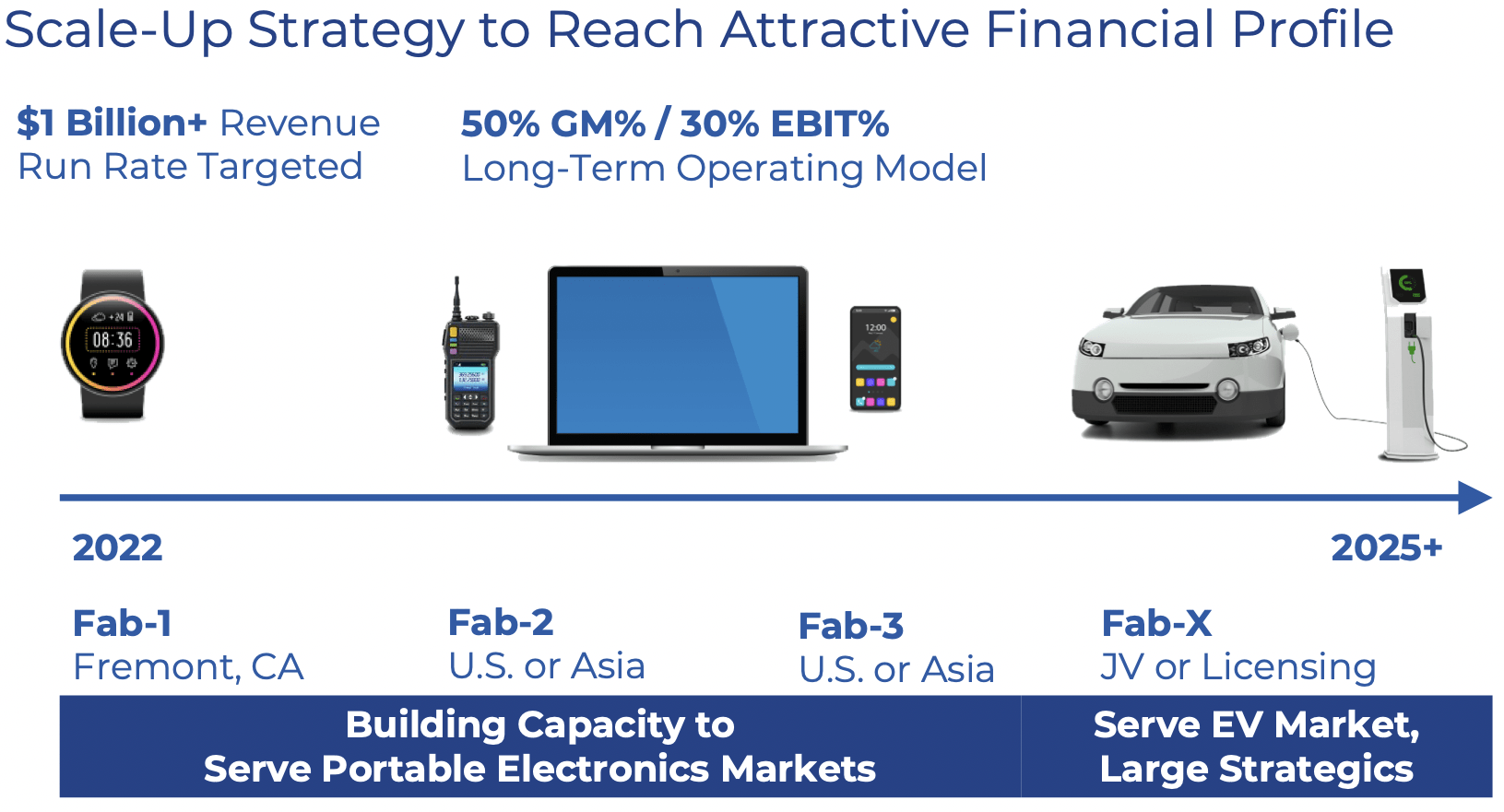

Another piece of good news was that the company has managed to deliver its first commercial product from its first production plant called Fab-1 and recognise the resulting product revenues in the current quarter, which meets expectations for the beginning of operational roll out.

That said, I think that while this first delivery is a major milestone reached, the more crucial portion of the operational roll out will be the scaling up and operational improvements that needs to be made to ensure that high manufacturing yields are achieved.

To that end, the management team main priority is then to improve Fab-1 in the third quarter, optimise certain processes and rebuild old ones to ensure that after the adjustments made in the third quarter, hopefully the company is then well positioned for the ramp up in production for 2023.

I like that management is not just focused on improving the revenue funnel and commercialising customers, but the management is well aware that even with the best customers and the largest orders, the key to their success is their operational success and reliability. I am of the opinion that more mega cap technology companies will be keen to add Enovix technology to their products after Enovix management has demonstrated their operational reliability and efficiency, as well as being able to deliver products on time and with the best quality. I am confident that Harrold Rust, with the operational experience he has had, will bring great value add to the ramping up of high volume production facilities for Enovix.

As management focuses on Fab-1 and improving operational efficiency there, it is already looking ahead to its Gen-2 production line design to further improve the operational efficiency by, for example, reducing the footprint needed compared to Gen-1 production line. However, management said in the second quarter earnings call that they expect to be incorporating what they learnt from Fab-1 as well as to also integrate the BrakeFlow technology into its Gen-2 production line and as a result, they are extending the time they need for designing Gen-2. They expect that Gen-2 will be rolled out in Fab-2 in the second half of next year.

As can be seen below, after their roll out of Fab-1, they are expecting to be having an additional Asia Fab apart from an additional domestic Fab in the next few years. The company remains open to capital light ways to grow like licensing or joint ventures, which will be the likely option for their future electric vehicles market and possibly for its strategic accounts if suitable.

Scale up strategy (Enovix 2Q22 presentation)

Valuation

I have prepared a financial model to value Enovix from the point of view of a relatively early stage company. As I expect most of its revenues to ramp up in 2024 and 2025, I have forecasted the financials for Enovix until 2025, with slight adjustments to revenue estimates in 2024 and 2025 to account for the strong demand for Enovix products. As a result, I expect the Enovix will see its revenues grow from the current $7 million in 2022 to $850 million in 2025, growing at a CAGR of 230% over the period. In addition, I expect Enovix to generate positive EPS of $0.65 in 2025.

Based on an assumption of 50x 2025F P/E and 6x 2025F P/S multiples and discounting that, my target price for Enovix is $35.20, implying 86% upside from current levels. I believe that the high price tag is reasonable for Enovix given that they are well positioned for future large design wins with significant revenue acceleration to come by 2025. Furthermore, there are high barriers to entry as Enovix is potentially several years ahead of many of its competitors and it is thus able to offer higher performance and safety features than its competitors and earn a higher margin from that.

Risks

Operational and execution risk

Now that Enovix has delivered its first product and officially started operations in its Fab-1, the company needs to be able to operate at high levels of efficiency to satisfy the needs of its customers. Furthermore, execution risk is real because of the need for these large strategic accounts to have the exact specification of product that they have ordered and at a high quality, delivered on time when it is needed. As a relatively small and early stage company, Enovix needs to prove to its customers that it is able to execute well and operate efficiently to continue attracting large strategic accounts.

Competition risk

While Enovix appears to be well ahead of competition at the moment, I think that a key risk is that there are many startups and private companies developing new and emerging technologies that may compete with Enovix in the future. One such competition is a private company called Sila Nanotechnologies, that is in the silicon anode lithium ion battery space. While there is relatively little information about the company out there due to their private company status, it could be making huge progress in their technology that could rival Enovix in the future.

Conclusion

As elaborated earlier, I think that the recent significant customer milestones show that Enovix offers leading battery technology for the large strategic customers that it is attracting. I am of the view that this momentum in strategic account interest will continue as more mega cap technology companies become aware of the higher performance benefits and safety profile that Enovix brings. In addition, the new BrakeFlow technology also adds to the compelling value add perspective of Enovix as the company brings added safety to lithium ion batteries that is not seen in the current market. Lastly, the company is executing well and with the key operational milestone of the first fab-1 delivering its first product and recognising its first product revenue, the next step would be to improve productivity and operational yield to ensure that ramp up next year becomes smooth. My target price of $35.20 for Enovix implies 86% upside from current levels and there is a positive skew for the company in terms of risk/reward at the moment as the company gains huge momentum in its business.

Be the first to comment