Scott Olson/Getty Images News

Despite knowing legacy airlines were posting near record holiday earnings, United Airlines (NASDAQ:UAL) only trades at approximately half of pre-COVID levels. The airline actually reported shockingly strong guidance for 2023. My investment thesis remains ultra bullish on the stock due to the market disconnect with the earnings power of the airline.

Big 2023 Ahead

United reported Q4 earnings that topped analyst targets, but what really matters is the comparison to 2019 levels. The airline posted the following strong comps to Q4’19:

- Capacity down 9%

- TRASM of up 26%

- CASM up 21%, and CASM-ex up 11%

- Operating margin of 11.1%, adjusted operating margin of 11.2%, both up over 2 points

- Pre-tax margin of 9.1%, adjusted pre-tax margin of 9.0%, both up and around 1 point

Heading into 2023, the market was still valuing airlines as if bankruptcy risk was a legitimate possibility. United Airlines dipped to only $37 at the start of the year. The rally to $50-plus needs to be kept in perspective and not treated as if the recent price jump should cap the upside.

The guidance for 2023 should blow away most investors ignoring the airlines since the COVID shutdowns. United Airlines just predicted a 2023 EPS of $10 to $12 while analysts only have EPS targets of $6.42. Despite all of the additional interest expenses from higher debt levels and additional shares outstanding, the management team forecast a return to double digit profits per share.

Clearly, the market thinks CEO Scott Kirby is nuts with the stock hardly budging in after-hours trading. United Airlines last traded at just $52.40.

Source: Seeking Alpha

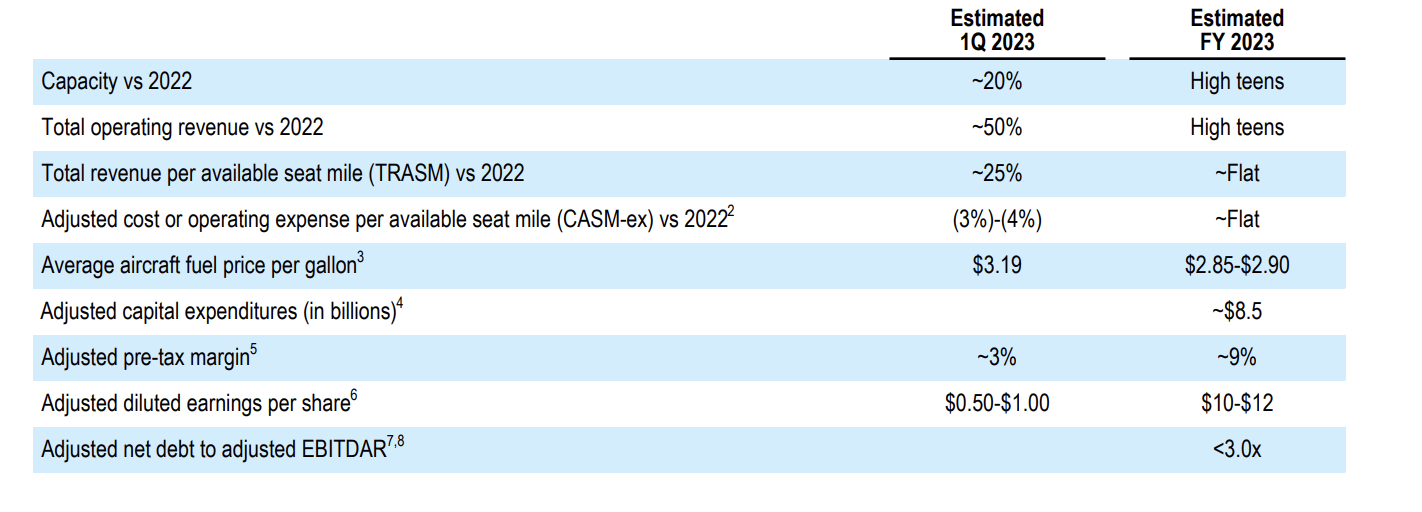

Investors need to remember management previously guided to a huge margin improvement in the business model with the United Next program. This year is just the start of the goal with a forecast for pre-tax margins of ~9% for the year matching the levels already obtained in a normally weak holiday quarter where United Airlines earned $2.46 per share.

Source: United Airlines January investor update

United Airlines has long forecast the ability to produce industry leading margins of 14% over the long term with a current target of 2026. My prior estimate forecast an EPS potential of $17-plus for a stock struggling around $50 for several years now.

Big Spending Fears

For whatever reason, the airlines are still treated like the sector from decades past that regularly went bankrupt due to a lack of financial discipline. The sector aggressively spent the years prior to COVID lockdowns returning capital to shareholders, not losing money.

The airlines made a mistake of not having the financial flexibility to handle a near shutdown, but most companies are in the same scenario. United’s plan to purchase hundreds of aircraft from Boeing (BA) probably brought back those fears of aggressive spending, but United is acquiring assets the airline would otherwise have to pay leases. The asset generally holds value due to slow replacement production of new aircraft.

United Airlines forecasts spending $8.5 billion on capex this year. The airline should earn $3.3 billion during the year with a $10 EPS. Along with annual depreciation costs of $2.5 billion, United will still be cash flow negative with the aggressive order of modern aircraft leading to heavy spending.

One reason the huge spending is justified is that United isn’t even back to pre-COVID capacity levels and GDP data still supports far higher airfare spending levels. The industry as a whole should be soaring past 2019 levels here four years later.

The air travel revenue to GDP sat at nearly 0.5% in the decade prior to 2020 shutdowns and the massive rebound in 2022 only saw a return to industry domestic revenue at 0.45% of GDP. In essence, the airline industry still has to grow revenues 15% over the 2022 levels in order to match the GDP percentage due to the strong nominal GDP growth since 2019.

Source: United Airlines Q4’22 presentation

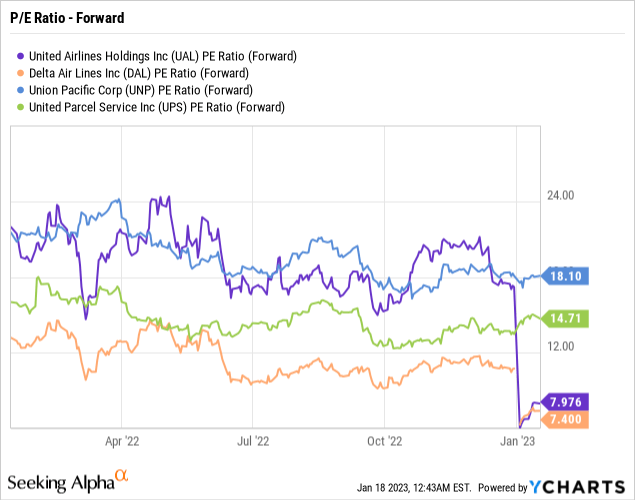

The aggressive spending is only set to last a few years and should roll off as United generates vastly higher profits with more fuel efficient aircraft. Delta Air Lines (DAL) has always been seen as the leader that should trade similar to industrial transport peers, but one has to wonder why United shouldn’t join those ranks.

Both rail and package delivery sectors have faced tough years, yet these stocks trade at closer to 15x EPS targets. Union Pacific (UNP) trades at 18x forward EPS estimates with limited growth targeted for 2023 while United Parcel Service (UPS) has EPS estimates dipping this year, yet the stock still trades at 15x those estimates.

Investors need to realize that United Airlines is now a profit machine. The airline would trade at $150-plus with a similar valuation multiple based on the 2023 targets from the company.

Takeaway

The key investor takeaway is that United Airlines is still priced for another COVID shutdown. Instead, the airline is focused on building a bigger airline with modern aircraft and the operating cash flows to pay down debt or add new aircraft.

The stock is far too cheap barely topping $50 and only rallying $1 in after-hours trading after boosting 2023 EPS targets nearly $5 above analyst estimates.

Be the first to comment