Torsten Asmus

Investing today is much more difficult than it has been in the last decade. From 2008 to 2021 interest rates remained very low, the Fed continued to support equities, and earnings remain consistently strong other than during the Pandemic. Today the investing environment has changed significantly.

The simplest way to invest is by purchasing index funds such as the Vanguard S&P 500 ETF (NYSEARCA:VOO), an exchange traded fund that is indexed to the S&P 500. Last I covered this ETF in Aug 2022.

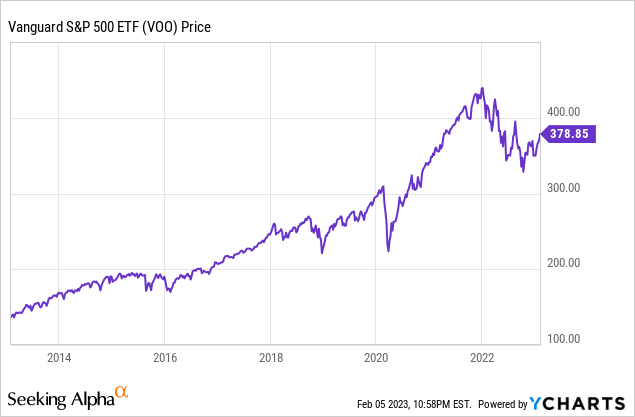

The S&P 500 outperformed most ETFs and other equity investing strategies over the last 10 years.

Index investing was a good strategy over the last decade primarily because the Fed continued to support equities with low rates and different form of quantitative easing, earnings growth was consistent, and inflation stayed under control. Today the investing environment has become much more complicated for a number of reasons.

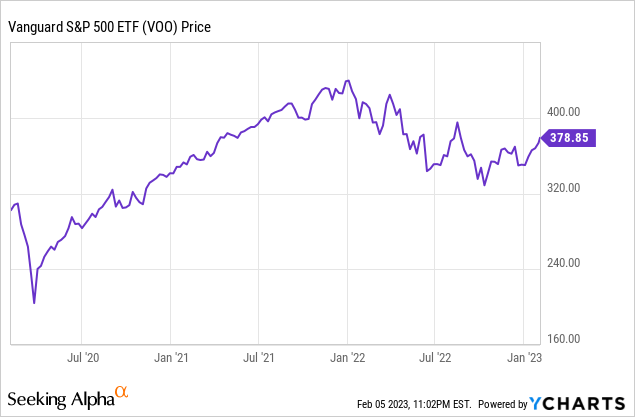

The S&P 500 has risen only modestly over the last two and a half years, and investors in the funds indexed to the S&P 500 have not gotten inflation adjust returns or income during this volatile period.

The S&P 500 has only risen around 7% a year over the last three years, and the market hasn’t increased at all over the last year, the yield of funds indexed to the S&P 500 such as the Vanguard S&P 500 fund are also minimal. This fund yields just 1.57%. Inflation rates have consistently been above 5% since early 2021, investors who have allocated capital primarily to index funds have struggled to get any real overall income or total returns.

The three main issues that index funds such as the Vanguard S&P 500 fund face today are rising rates, a rising dollar, and flatlining earnings.

Powell has already said the Fed is committed to raising rates to control inflation, and rates continue to rise well inflation also remains at historically high levels. A rising dollar and increasing costs have also put significant pressure on corporate earnings and margins. Inflation rates are also unlikely to subside significantly in the near-term.

Even though the dollar has pulled back recently, the dollar has still risen significantly against most major currencies over the last several years. About 37% of S&P 500 earnings come from outside of the United States, so a 10% rise in the dollar usually equates to a near 4% drop in earnings expectations. The dollar has risen well over 10% against most major currencies just since early May. Europe continues to deal with an energy crisis, China is still dealing with Covid issues, and inflation continues to impact many emerging market economies more than the US. The Dollar is likely to remain strong.

Several leading analyst firms also see earnings expectations for 2023 as being unrealistically optimistic as well. Goldman Sachs has already said they expect S&P 500 earnings growth to flatline in 2023, and Morgan Stanley has also recently said they think current consensus estimates calling for 4% earnings growth are unrealistic. Inventories also continue to rise in the consumer retail industry, the housing market has slowed, and many leading big tech firms have already laid off significant works. There remains a number of signs that the economy is likely to continue to slow in the near-term.

Many of the main factors driving inflation are likely to remain challenging as well. Supply chain issues originating in Asia aren’t likely to subside anytime soon as China and other Asian countries continue to deal with Covid outbreaks. The war between Russia and Ukraine, which has contributed to rising costs, continues, with Russia now planning a new offensive. The tight labor market, which is leading to wages rising, remains an issue as well. Inflation is likely here to stay, and that means that corporate margins and earnings should remain under pressure for some time.

The Vanguard S&P 500 fund is also not cheap using a number of metrics. The S&P 500 trades at 29.3x earnings, and 17.57x cash flow. This is well above the modern era market ear average of 19.6x earnings. Most analysts are also projecting earnings growth of this index to be in the range of 2-4%, and funds such as this Vanguard fund that are indexed to the S&P 500 are yielding below 2%. While there are factors that could lead earnings to accelerate faster than analysts are projecting, like China opening up their economy more aggressively, the rate of inflation slowing, or Europe’s energy crisis easing, overall growth rates in the US and abroad are more likely to remain slow for some time.

With the Fed committed to raising rates, inflation still negatively impacting earnings, and the dollar likely to remain strong against most major currencies for some time, the broader indexes are likely to remain rangebound for some time. Investing becomes more challenging in precarious markets such as this one, and most investors seeking inflation adjust income and total returns will need to be more creative in this kind of economic environment. Index funds that sell covered calls against their holdings to take advantage of volatility and offer investors significant income and total returns even in a flatlining markets, are likely to outperform index funds. These funds include the Global X S&P 500 Covered Call Exchange Traded Fund (XYLD), and the Global X Russell 2000 Covered Call Fund (RYLD), all ETFS that have consistently returned at least 9% a year over the last 3 years, and each fund offers monthly payouts as well.

Be the first to comment