Sergei Dubrovskii

Houston-based Helix Energy Solutions Group, Inc. (NYSE:HLX), or “Helix,” is one of the world’s leading offshore energy specialty services companies.

The company operates through three segments: Well Intervention, Robotics, and Production Facilities, with the well intervention business currently contributing approximately two thirds of revenues.

Helix recently acquired the Alliance group of companies (“Alliance”) for $120 million in cash, a Louisiana-based provider of services in support of the upstream and midstream industries in the Gulf of Mexico shelf, including offshore oil field decommissioning and reclamation, project management, engineered solutions, intervention, maintenance, repair, heavy lift and commercial diving services.

The acquisition will contribute Adjusted EBITDA of up to $25 million and increase consolidated revenue by approximately 15% this year.

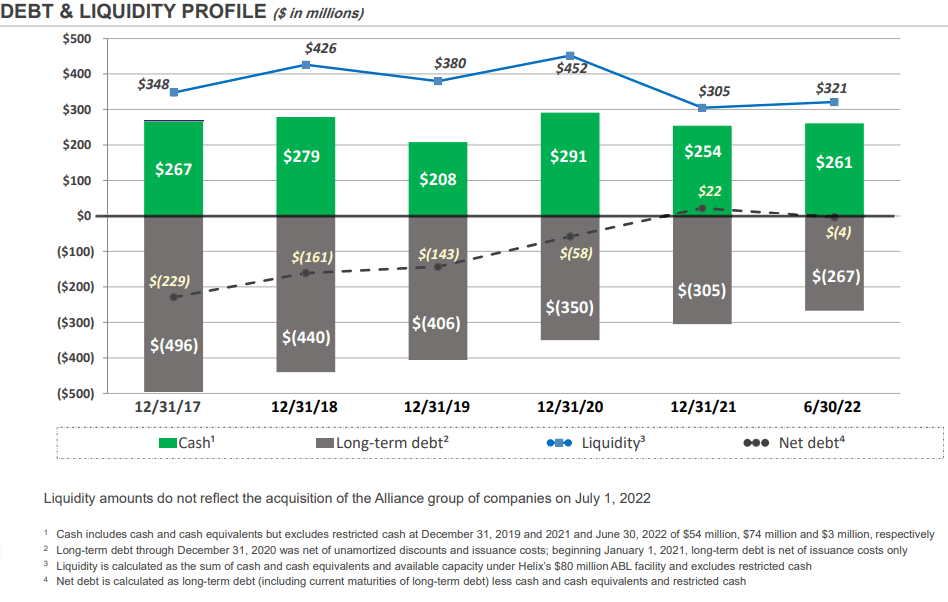

Helix has done quite well for most of the industry downturn as financial results were boosted by a number of high-margin legacy contracts. As a result, the company has not only managed to stay afloat but also reduced debt substantially in recent years:

Company Presentation

Please note that the recently completed Alliance acquisition will reduce cash on hand by $120 million next quarter.

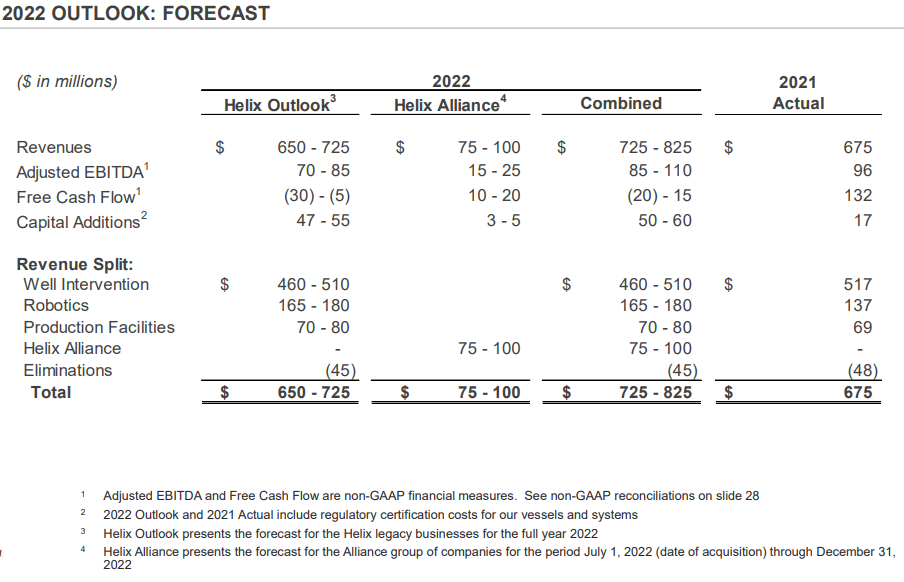

That said, management expects 2022 to be a transition year with several vessels undergoing regulatory inspections, a slow return for the North Sea market and a number of units performing short-term work at reduced rates with the company’s two modern well intervention vessels in Brazil causing an estimated $35 million EBITDA hit alone.

As a result, the combined company’s free cash flow will only be around break-even levels, down from $132 million recorded last year:

Company Presentation

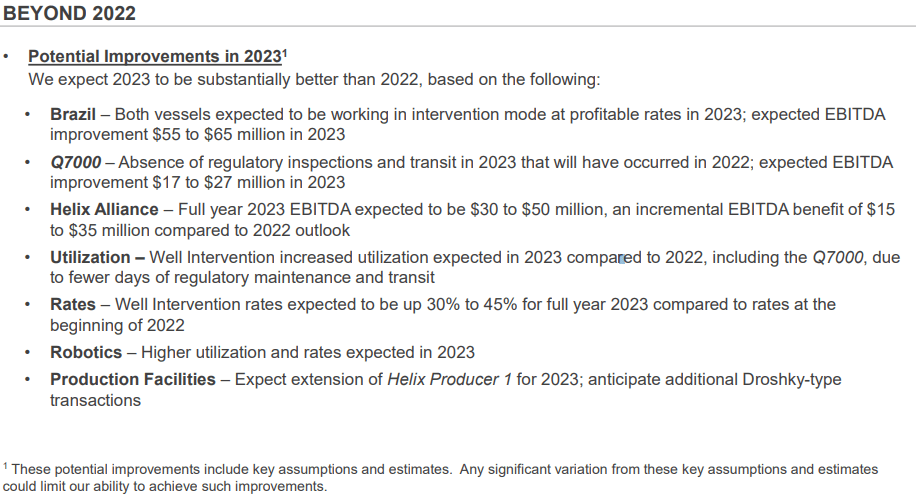

But things are expected to change for the better going into the second half and next year as business conditions are improving across all segments as stated by management on the Q2 conference call:

Stronger utilization, increasing rates and in certain areas of the business, rates are improving better and quicker than we expected along with better terms and conditions. We are securing longer term contracts and looking to see more work with some of the Well Intervention assets into 2025.

(…)

Not only have the uncertainties of 2022 becoming clear, we also have perhaps the best visibility in recent years at this point for what may happen next year in 2023.

(…)

We’ve called 2022 a transition year for Helix. We fully intend to transition from a weak market in ’22 to a high demand market in ’23 and beyond.

In the Q2 presentation, Helix projected up to $127 million in EBITDA improvements in 2023 based on expectations for well intervention rates being up between 30% and 45% for the full year compared to rates at the beginning of 2022.

The company also forecasted higher utilization and rates for the Robotics segment next year.

Company Presentation

Personally, I am expecting Adjusted EBITDA of at least $225 million in 2023, more than double the high end of the company’s projection for this year.

At this level, Helix should return to substantial free cash flow generation next year.

With the company trading at just 2.7x EV / Adjusted 2023 EBITDA despite current expectations for a multi-year recovery in the offshore oil and gas markets, Helix looks remarkably cheap.

Bottom Line

While 2022 will be nothing to write home about for Helix Energy Solutions, the company projects substantial improvement going into next year with the potential to at least double Adjusted EBITDA from anticipated 2022 levels.

Even after the recent acquisition of Alliance, Helix continues to have a solid balance sheet with low net debt levels and decent liquidity which should improve substantially over the next couple of quarters.

With the company trading at just 2.7x projected EV / Adjusted 2023 EBITDA, Helix looks very cheap.

That said, with shares up by almost 40% from recent lows, investors should consider waiting for a setback before opening a position.

Get long Helix Energy Solutions to gain exposure to the anticipated multi-year recovery in offshore oil and gas services. Assuming no major sell-off in oil prices, I would expect shares to double from current levels going into next year.

Be the first to comment