umbertoleporini/iStock Editorial via Getty Images

We initiated our coverage of UniCredit (OTCPK:UNCFF) with a neutral rating and then, after the Q1 results and our deep dive into UniCredit’s activities in Russia, we move on with an outperform buy rating thanks to a recent analysis called: UniCredit could return its entire market capitalization in 4 years. Today, the bank released its three-month numbers, and we can clearly say that we are pleased with our recent rating upgrade.

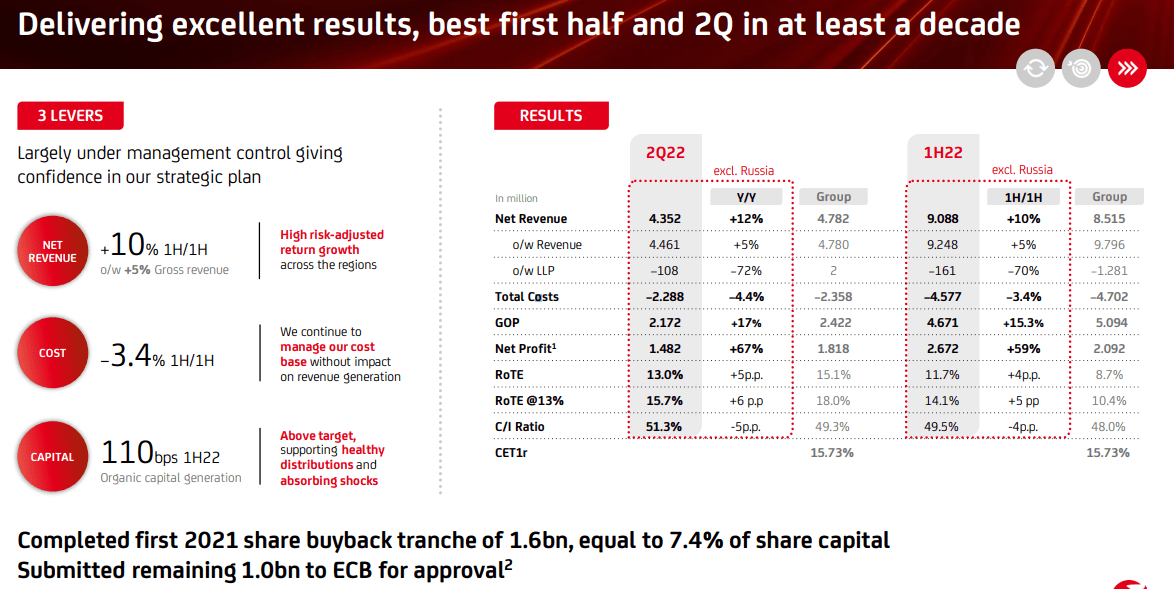

Looking at the accounts and quoting the CEO’s words – this was the best semester of the latest ten years. In the press release, CEO Orcel explained that these results were achieved “by profitability growth, solid organic generation of capital and reduction of the cost base despite the impact of inflation“.

Q2 Results

Revenue reached €4.780 billion (consensus was forecasting €4.512 billion), up 8.9% year-on-year, and in addition, net income was above Wall Street analyst expectations. The Italian bank recorded a net profit of €2.010 billion versus an average estimate of less than a billion euros. In the last quarter, the bottom line was impacted by the Russian write-down, whereas in the second quarter, Russian activities had a positive impact of almost €500 million. This was due to the ruble’s strength. Excluding the currency impact, the group’s net income should have been €1.5 billion but still a great performance versus consensus expectations. This was supported by net interest income growth, a decrease in loan loss provisions which reflects assets quality and lower operating costs which were reduced by 4.4%. This led to a CET1 ratio of 15.73% against analysts’ expectations of 14%, and the bank’s profitability is running now with ROTE at 15.1%, up 7.1% year-on-year thanks to a robust organic capital generation.

UniCredit Financial Snap (UniCredit Q2 Results)

Conclusion and Valuation

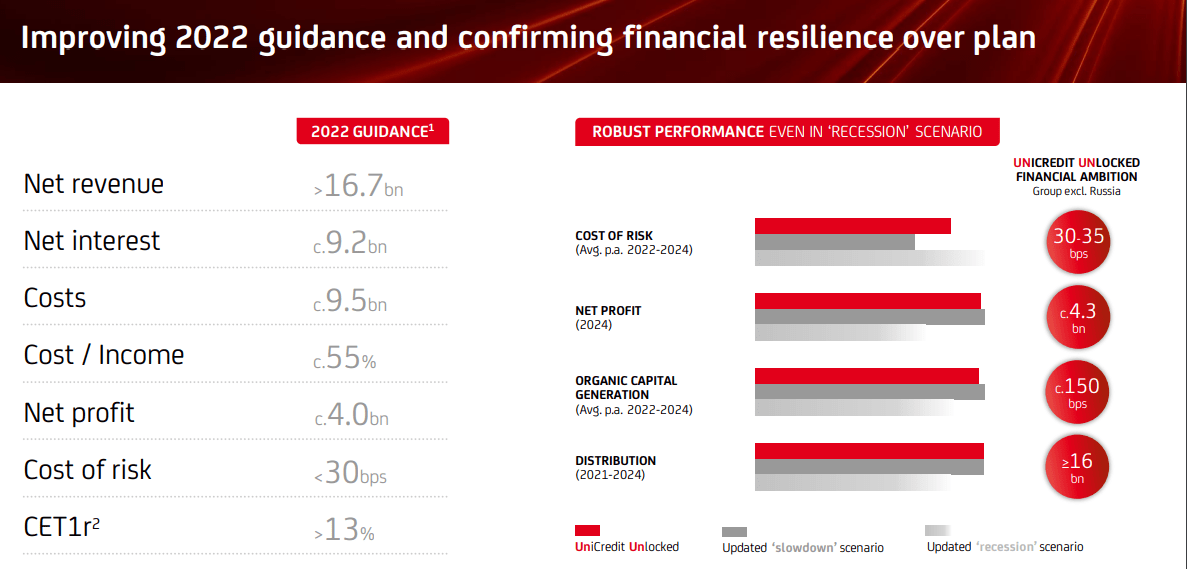

Recent economic indicators point to a deterioration in the macro outlook, especially in the manufacturing sector. In the euro area, economic activity is expected to be weak in the second half of the year due to a world trade slowdown, higher energy costs, growing uncertainties on energy supplies and a tightening of financing conditions. UniCredit currently also expects “a slowdown in the growth of private consumption in a context of deterioration in the purchasing power of households, partly offset by the possibility of tapping into the excess savings accumulated during the pandemic“. This will not support its guidance. However, in light of the recent results and the more favorable interest rate environment, UniCredit has improved its outlook. For 2022, expected revenues are above €16.7 billion (they were about €16 billion in the March guidance) and net profit is forecasted at approximately €4 billion (it was €3.3 billion in the previous guidance). The cost of risk is estimated below 30 basis points (it was at 30-35 basis points) and a CET1 ratio higher than 13% (it was between 12.5 and 13%).

Meanwhile, the bank has asked the ECB for a green light for an additional buyback of €1 billion, after having concluded the first purchase tranche.

Today, we expect a positive price appreciation, and we reaffirm our valuation at €13 per share. UniCredit’s current valuation is not justified, the company is trading at 30% of its tangible equity.

UniCredit Guidance Update (UniCredit Q2 Results)

Be the first to comment