Noam Galai

Thesis

In early May I warned investors that it is not yet time to be a buyer of UiPath (NYSE:PATH) stock. Since then, PATH stock is down approximately 20%, versus a loss of only 4% for the S&P 500 (SPY).

Although PATH stock is slowly approaching an attractive risk/reward valuation, I still struggle to convince myself to be a buyer. In fact, as a consequence of higher risk premia for unprofitable tech stocks, as well as a softer earnings outlook for UiPath going into 2023, I lower my base case target price for PATH to $12.42/share, as compared to $14.34 prior.

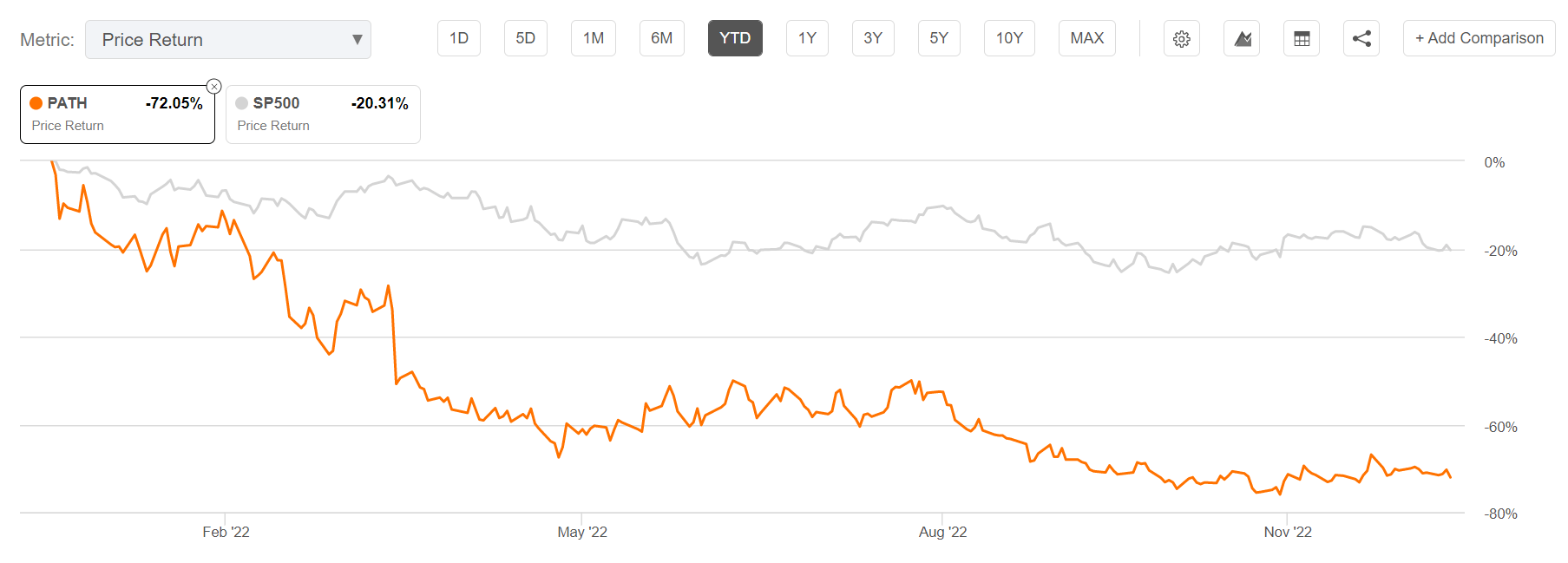

UiPath is one of the worst performing tech stocks YTD – down 72%.

Seeking Alpha

UiPath Q3 Results Fail To Match Expectations

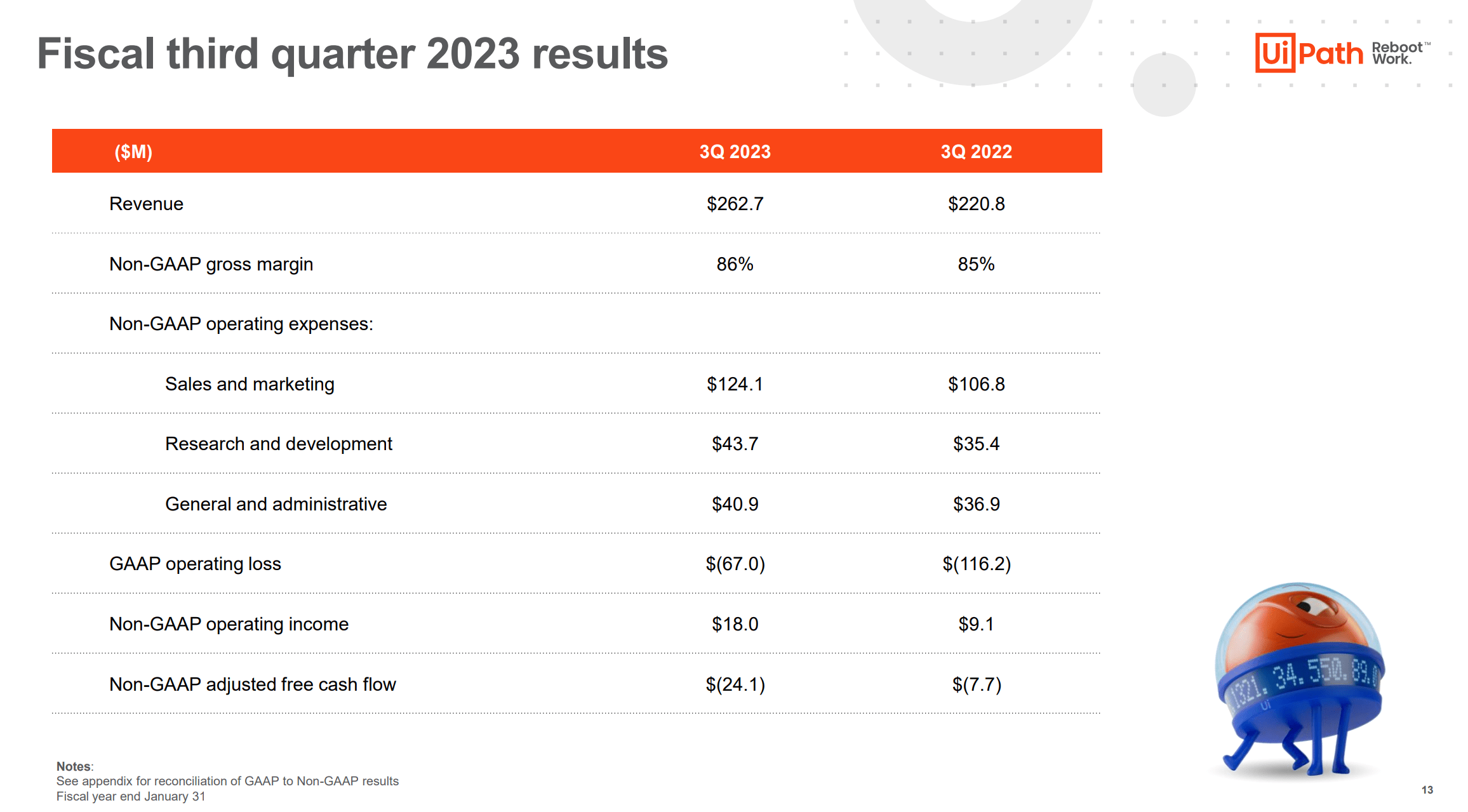

To be fair, UiPath’s FY 2023 Q3 results were not bad, but they were not stellar either. During the period from August to end of October, UiPath generated total revenues of $262.7 million, which compares to $220 million for the same period one year prior (approximately 19% year over year growth). Analyst consensus had expected revenues of $262.74 million – so UiPath actually delivered a slight beat. ARR increased 36% year over year, to $1,11 billion, adding net new ARR of $66.8 million.

Other highlights for Q3 FY 2023 include:

- Dollar based net retention rate of 126 percent. GAAP gross margin was 84 percent.

- Non-GAAP gross margin was 86 percent.

- Net cash used in operations was $27.3 million.

- Non-GAAP adjusted free cash flow was negative $24.1 million.

Although UiPath’s GAAP operating loss for Q3 2023 slightly narrowed as compared to the same period for FY 2022, the company still recorded a material loss of $67 million.

UiPath FY 2023 Q3 Results

UiPath ended Q3 FY 2023 with approximately $1.7 billion of cash and cash equivalents, including marketable securities, and total financial debt of $61.5 million. This should give investors comfort that even though the macro environment is challenging, and even though UiPath is still writing losses, the company has likely enough capital to bridge reasonable losses for multiple years.

Guidance Disappoints

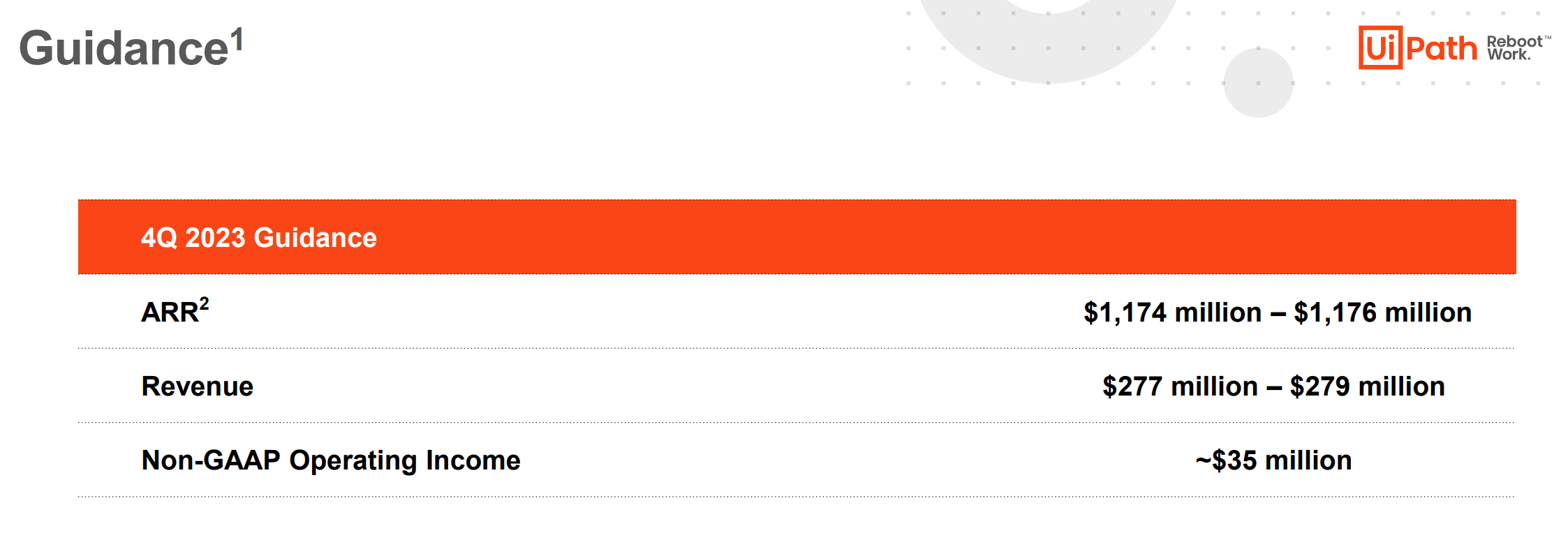

Although UiPath’s Q4 guidance projects quarter over quarter growth, and positive operating income (Non-GAAP), I argue that the outlook disappoints against what investors would reasonably expect from a x5 EV/Sales long-duration asset whose valuation is strongly anchored on growth.

For the Q4 2023 period ending January, UiPath expects that revenue will fall somewhere between $272 and $279 million, reflecting a 4% quarter over quarter growth. ARR is expected to expand to between $1,174 and $1,176 million, which would be a 5% growth respectively.

UiPath FY 2023 Q3 Results

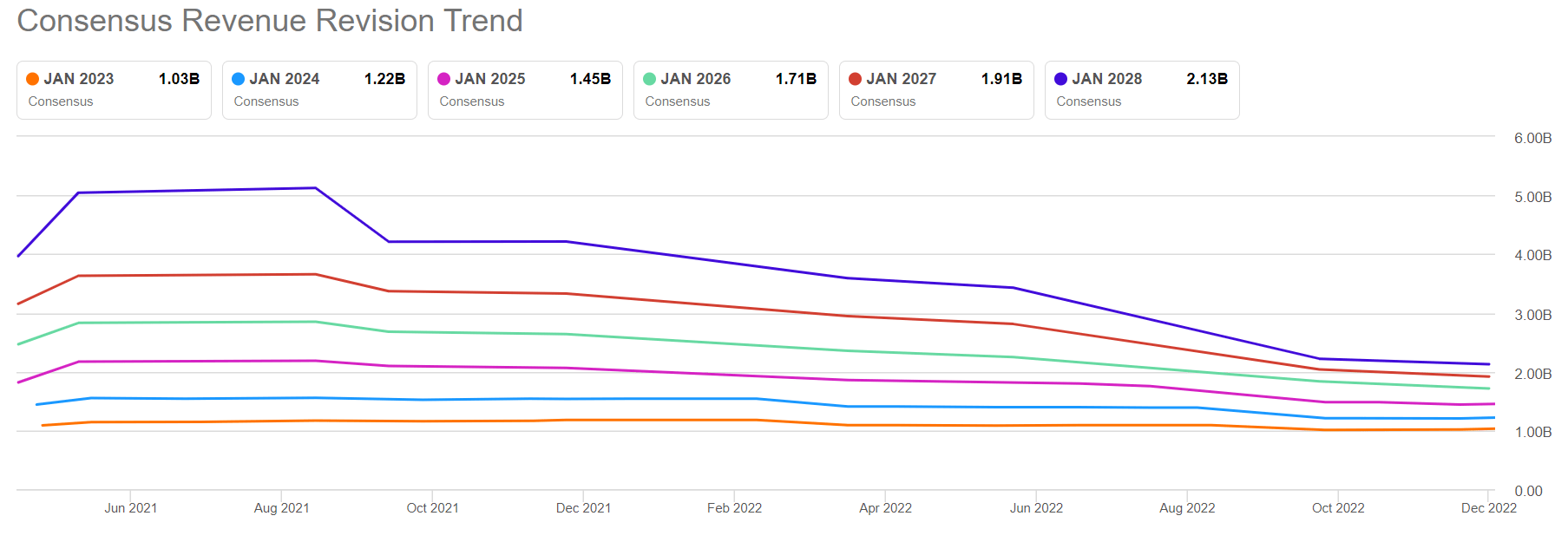

UiPath’s expected Q4 growth is notable. But investors should consider that Q4 guidance certainly does not help to support deteriorating analyst sentiment. Only a year ago, analyst had expected that UiPath would generate around $4 billion of revenues by 2028. This number has now been almost halved, down to only slightly more than $2 billion.

Seeking Alpha

Valuation: Lower TP

On the backdrop of a much softer macro outlook, as compared to May 2022, I lower my EPS expectations for PATH in 2023. Moreover, as a consequence of higher risk premia for unprofitable growth stocks, I also raise my cost of equity estimate for PATH to 10%, versus 9% prior.

I continue to anchor on a 3.25% terminal growth rate (one percentage point higher than estimated nominal global GDP growth).

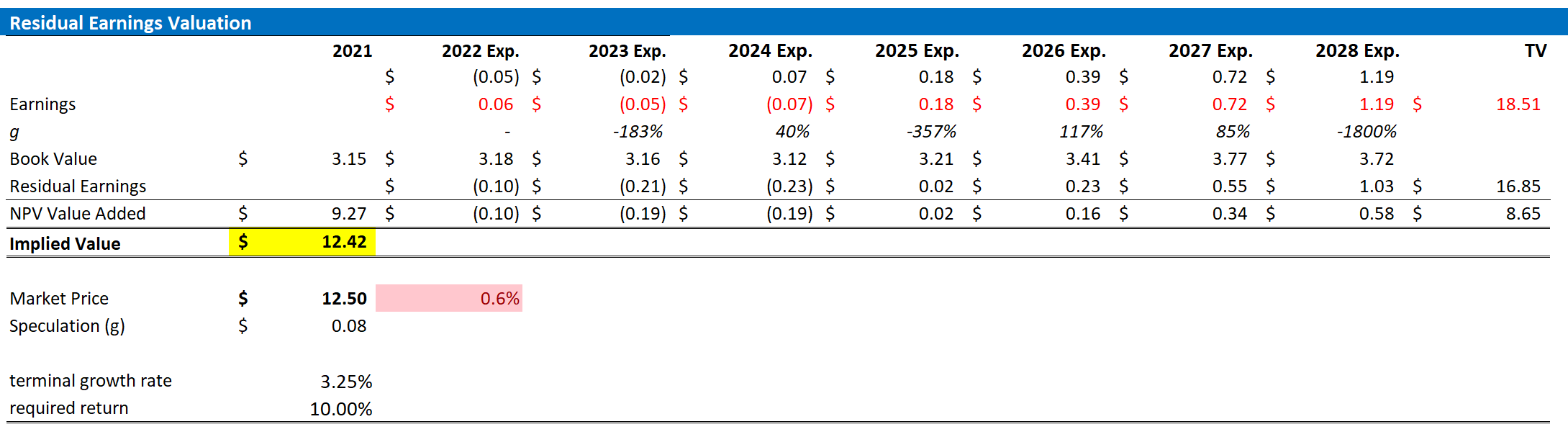

Given the EPS upgrades as highlighted below, I now calculate a fair implied share price for UiPath of $12.5, as compared to $14.34 prior.

Author’s Estimates; Author’s Calculation

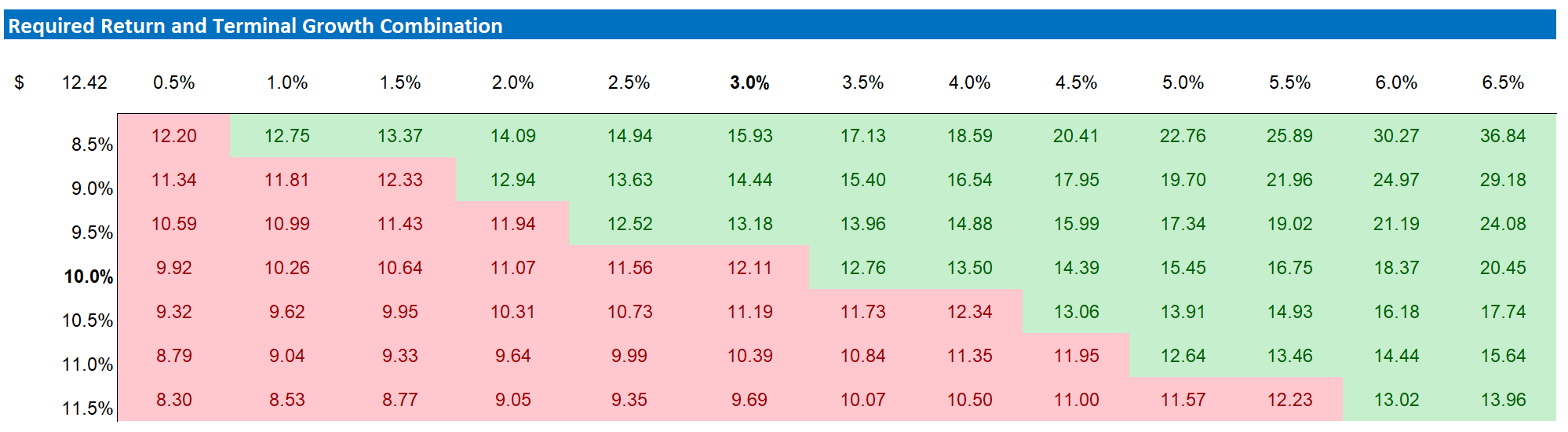

Below is also the updated sensitivity table, showing that at current valuation levels, the risk/reward for investing in PATH stock is very balanced.

Author’s Estimates; Author’s Calculation

Risks/Catalysts

As I see it, there has been no major risk-updated since I have last covered PATH stock. Thus, I would like to highlight what I have written before:

First, UiPath has a history of loss-making operations. There is no guarantee that the company will achieve significant profitability in the next few years, if ever. Second, competition is likely to intensify as big tech companies such as Microsoft (e.g., Power Automate) are aiming to increase their market share in automation software. Can UiPath compete with Microsoft’s human capital, distribution network, balance sheet and R&D spending? Third, with rising riel yields growth assets have experienced strong selling pressure. Although PATH stock is down significantly (-80%) since the IPO in April 2021, there is still a lot of speculation built into the current valuation. The selling party might not yet be over.

As potential upside catalysts I see three major factors: stronger top-line revenue growth than expected, likely due to strengthening macro-economic outlook; the cost of human capital increases further (see inflation), which accelerates the evolution towards the fully automated enterprise, and sentiment towards growth assets improves.

Conclusion

Although the need for low/no code process automation will likely continue to grow in the future, I argue that UiPath’s x5 EV/Sales valuation discounts too much of this growth already. In fact, in order not to disappoint investors (analyst consensus estimates) UiPath would need to materialize a greater than 20% revenue CAGR until at least 2022 – which is a very speculative prediction in my opinion.

As a consequence of higher risk premia for unprofitable tech stocks, as well as a softer earnings outlook for UiPath going into 2023, I lower my base case target price for PATH to $12.42/share, as compared to $14.34 prior.

Be the first to comment