RichVintage

The S&P 500 has climbed as much as 17% from its bear-market low last October in what feels like the most hated rally on record. The vast majority of Wall Street strategists and market pundits continue to call it a bear-market bounce, which suggests that we will revisit the October low later this year. Last year this same group was convinced that consumption would roll over in the face of elevated prices, a deteriorating labor market, and rising interest rates, leading to a recession. It has not. This year they say economic resilience will force the Fed to keep raising interest rates higher than previously expected to rein in inflation, which will ultimately end in recession. I disagree. Either way, there seems to be no light at the end of their tunnel, as all news is bad news. Stocks fell sharply yesterday on news that US producer prices rebounded in January more than expected, but the bears had a helping hand from two Fed governors as well.

Finviz

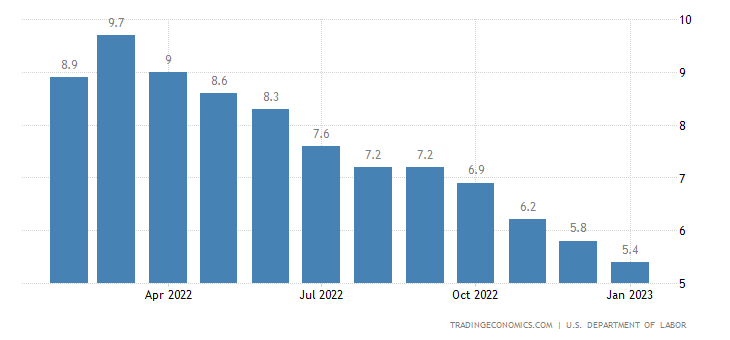

Yes, the monthly increase of 0.7% in January for the producer price index, as well as the core increase of 0.5%, were both more than expected. So what! This does not point to persistent inflationary pressure, as it was described by the financial media. Despite the monthly increase, the steady downtrend in the year-over-year rate continues with the overall index declining from 6.2% to 6%, and the core rate falling from 5.8% to 5.4%, as seen below. The strength in this monthly number is consistent with what we saw in the Consumer Price Index and retails sales. January looks more like an anomaly than an end to the disinflationary process that started last summer. Yet it serves as red meat for a bearish consensus that has sat on the sidelines of the market rally over the past four months, but it is also a good reason for a healthy pullback to consolidate gains.

TradingEconomics

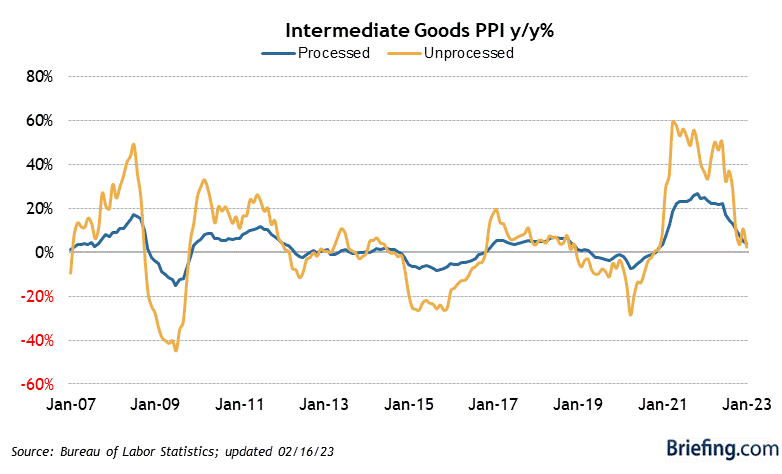

If the rate of increase in wholesale prices was going to start rising again, we would not be seeing the prices of intermediate goods, which reflect prices earlier in the production pipeline, collapse to negligible gains. This tells us that producer prices should continue declining as we move forward. Still, nothing moves in a straight line, and any minor deviation from the downtrend in any component of the index seems to bring the bears out of hibernation with skittish central bankers piling on.

Briefing.com

Yesterday, in what appeared to be an “I told you so” moment, Fed Presidents Loretta Mester and James Bullard indicated that they voted for a 50-basis-point rate increase at the Fed’s last meeting on February 1. I am glad more sensible minds prevailed. Yet investors didn’t like the fact that both now say they see a compelling case for raising rates 50 basis points at the next meeting. I seriously doubt that will happen. This looks like another attempt to wrestle down inflation expectations, as well as recent enthusiasm for risk assets.

Bloomberg

As the major market averages have recovered, and the high frequency economic data has come in better than expected, investors have brought back to life some of the more speculative corners of the market. That includes some of the most expensive technology stocks, a handful of meme names, and cryptocurrencies, led by Bitcoin. Again, nothing moves in a straight line in either direction, and the bears are pointing to this recent revival of speculation as a sign that the bear market has not yet run its course, but I think they continue to grasp for straws to explain why the market has not done what they think it should do. This is why the rally is so hated.

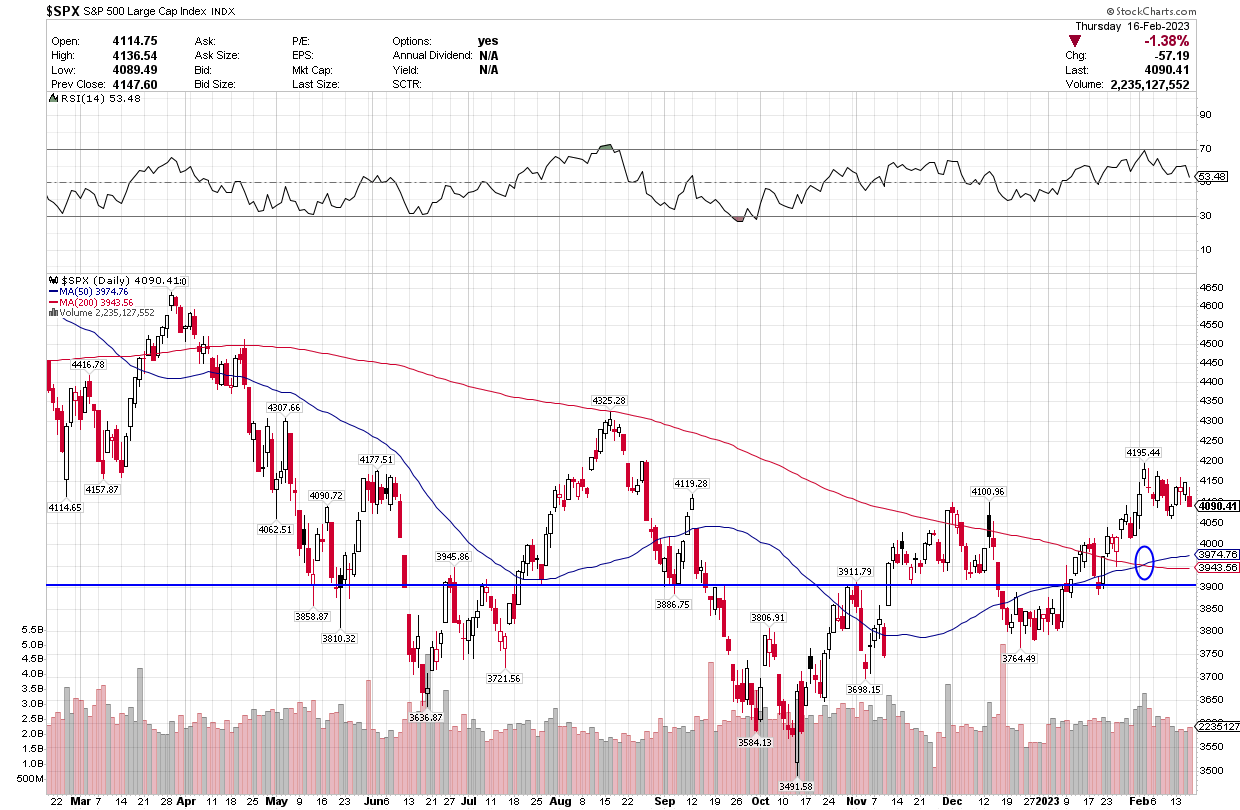

We have been in need of a pullback or pause to refresh that resolves the overbought condition in the market. In my view, that is what is happening. Early last week, I identified this need in Preparing For A Pullback To 3,900 in the S&P 500, and I think that level still looks reasonable. That should shake out a lot of the weak shareholders who might succumb to the emotions of fear perpetuated by the bearish consensus. Their chorus will grow louder as the index pulls back, reaching its highest pitch as we carve out a higher bottom, but that should position us for higher index levels as the year proceeds.

Stockcharts

Be the first to comment