eyecrave productions/E+ via Getty Images

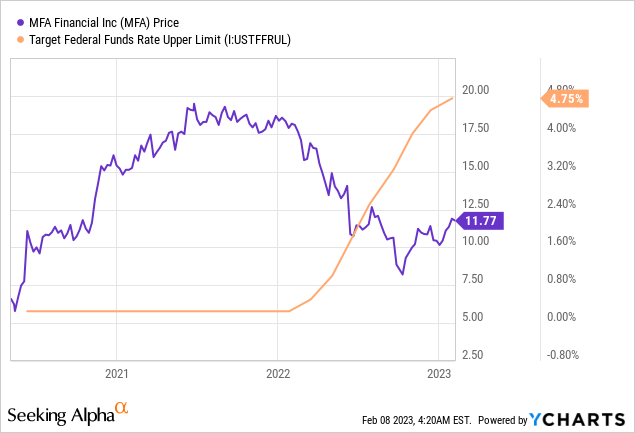

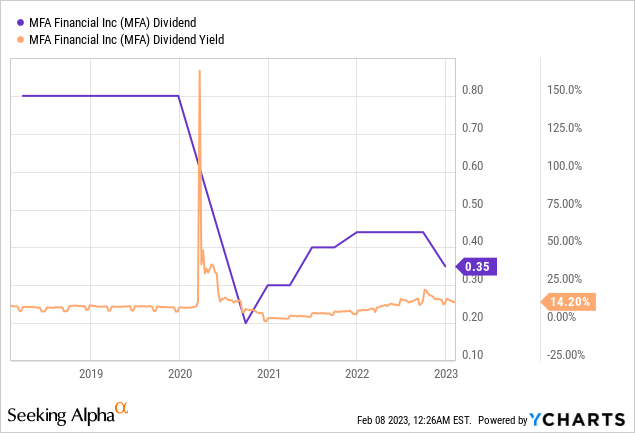

MFA Financial (NYSE:MFA) recently declared a quarterly per share cash dividend of $0.35, a 20% decline from its prior payout for a forward annualized yield of 11.88%. This is down from a retrospective yield of 14.2% and comes as still-rising Fed fund rates continue to increase the financing costs for highly leveraged companies. The business is straightforward, MFA is engaged in the business of investing on a highly leveraged basis in residential mortgages, including residential mortgage-backed securities and residential whole loans. Mortgage REITs, or mREITS, unlike their non-mortgage REIT counterparts, employ an outsized level of gearing which makes them even more sensitive to interest rate movements.

The mREIT has moved in somewhat of an inverse correlation with a Fed funds rate that is set for two further 25 basis points hikes, with inflation seemingly peaking. This sets the backdrop for the performance of MFA this year. The end of the hike cycle would lead to further stabilization of a stock price that has fallen by 35% from its 52-week high. However, MFA’s investors are in the mREIT because of its income. Hence, the broader gyrations from its stock price might be noise in the long term. This is why the cut has proved so destructive, as it has been aggregated with a low stock price whilst opening up the specter of further cuts, especially against the torrid macroeconomic context.

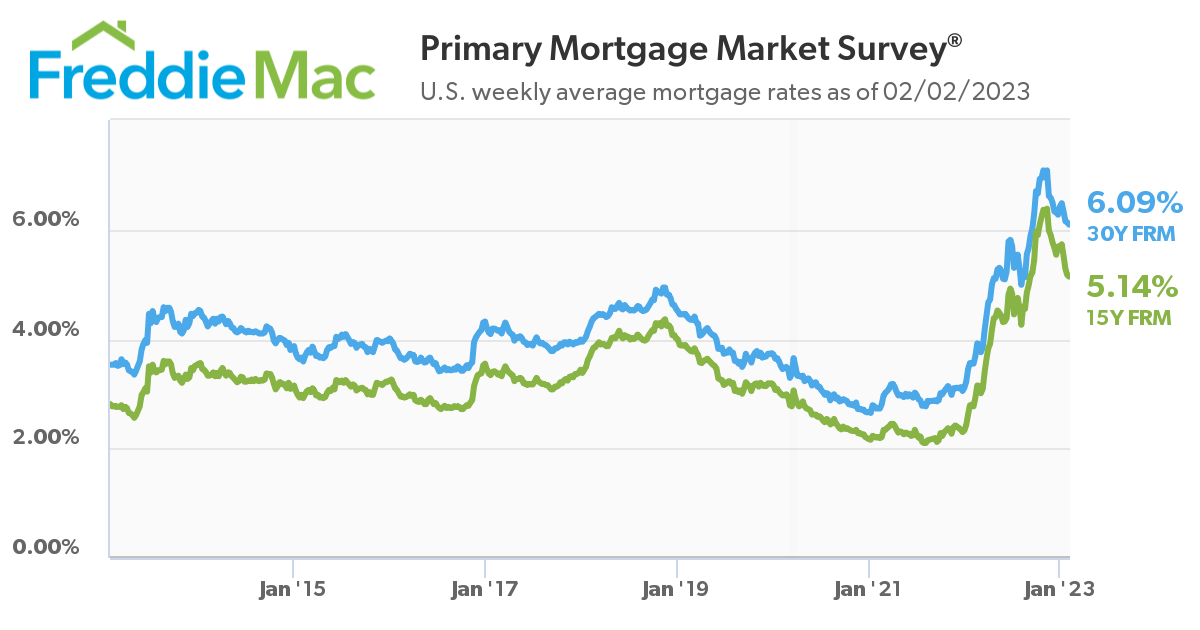

The Economic Situation Looks Set To Normalize, But Housing Is Being Discombobulated

Freddie Mac

US home sales are set to drop by 16% in 2023 to their lowest level since 2011 as higher mortgage rates work through the economy. This is as the 30-year primary mortgage rate currently sits a 6.09%, the highest since 2008, albeit down from highs of around 7%. Fundamentally, the mix of rising Fed fund rates and a weakening economy, potentially set to avoid a soft landing for a deep recession, will continue to place pressure on MFA.

The internally managed New York-based hybrid mREIT held a portfolio with a total equity value of $2 billion as of the end of its last reported fiscal 2022 third quarter. This was for a GAAP book value of $15.31 per share, down from $19.28 in the year-ago comp. It’s important to note that MFA instituted a 1-for-4 reverse stock split back in April 2022 that would see shareholders swap each four shares of MFA they owned pre-split for one share.

The mREIT’s net interest income at $52.29 million was a 15.4% decline from its year-ago quarter and a miss by $610,000 on consensus estimates. Distributable earnings came in at $28.2 million, or $0.28 per share, versus a GAAP net loss of $63.2 million during the quarter. Distributable earnings are still lower than the reduced $0.35 per share dividend. MFA’s management was somber during the earnings call, indicating that whilst they held cash of around $435 million as of the end of the third quarter, their previous quarterly dividend level was unsustainable from an earnings perspective. The cut was unexpected in that this was enough cash to maintain the previous payout for two and a half years. Shareholders will now be hoping that the rightsizing of the payout is in the rearview mirror, even as continued economic headwinds negatively impact the mREIT’s portfolio.

Grab An 9.3% Yield With MFA’s Series B Preferreds

Preferreds almost always offer a more structurally sound alternative for mREITs with a near-term history of underperformance, and MFA’s is no different. MFA Financial 7.50% Series B Cumulative Preferred Stock (NYSE:MFA.PB) pays out a $1.88 annual coupon for a 9.3% yield on cost. Currently trading at $20.12, they’re almost five years past their April 15, 2018 redemption date and come with a number of attractive features.

QuantumOnline

Firstly, they’re cumulative, reducing the likelihood of their quarterly distribution being suspended as the mREIT would have these accrue as a liability for repayment at a future redemption event. However, there was a brief suspension at the onset of the pandemic as mREITs were being margin called across the board during the initial meltdown. MFA issued $175 million worth of these preferreds back in 2013, almost a decade ago, and the current interest rate environment likely reduces the likelihood of them being called in the near term.

Secondly, they’re trading at a 19.5% discount to their $25 par value. Hence, prospective investors could grab these for just over 80 cents on the dollar whilst being paid a 9.3% yield. The hard $25 intrinsic value forms an anchor point for prospective investors and de-risks the overall investment. Whilst the yield is lower than the commons, they come with lower volatility and a potential 20% uplift when they’re eventually redeemed. So who are these for? Risk-averse income investors looking for a form of fixed-income exposure.

I’m not a fan of the commons, as the recent cut reverses what’s been a healthy recovery of the payout since 2020. Further, whilst the current economic indicators have placed the US on track for a soft landing, the situation could turn if inflation remains sticky. Against the broader macro risks and near-term history of dividend cuts, the preferreds would be the better consideration here.

Be the first to comment