helivideo

Due to its abundance, renewable nature, and low cost, wood has proven to be a remarkably important natural resource. Its physical strength and flexibility have also made it quite valuable for construction-related activities. One company that’s dedicated to utilizing wood for these various purposes is UFP Industries (NASDAQ:UFPI). In addition to producing wood decking and related accessories, the company also provides structural packaging solutions made out of wood, steel, and mixed material crates. It’s also involved in other areas related to wood and accessories that come from the wood products it creates. Although it’s possible that current market conditions for the enterprise will not remain as strong as they are today in perpetuity, shares do look very cheap on a forward basis. Even if we assume that financial performance takes a step back, I have a difficult time seeing the company as anything worse than fairly valued. This favorable risk-to-reward outlook causes me to feel confident enough in the enterprise to keep my ‘buy’ rating on the business for now.

Stellar performance

The last time I wrote an article about UFP Industries was back in June of this year. In that article, I called the company an interesting play on the construction space. I acknowledged that the company’s top and bottom lines had been performing really well, but I also said that investors are right to worry about a potential pullback in industry conditions. But given how attractively priced I said the company was, even if financial performance were to worsen, I ended up rating the business a ‘buy’, reflecting my belief that its shares would outperform the broader market for the foreseeable future. Although not much time has passed since then, this call has so far played out nicely. While the S&P 500 is down by 1.7%, shares of UFP Industries have generated a return for investors of 7.9%. If anything, that’s slightly better than what I would have anticipated in the short time we have experienced.

Author – SEC EDGAR Data

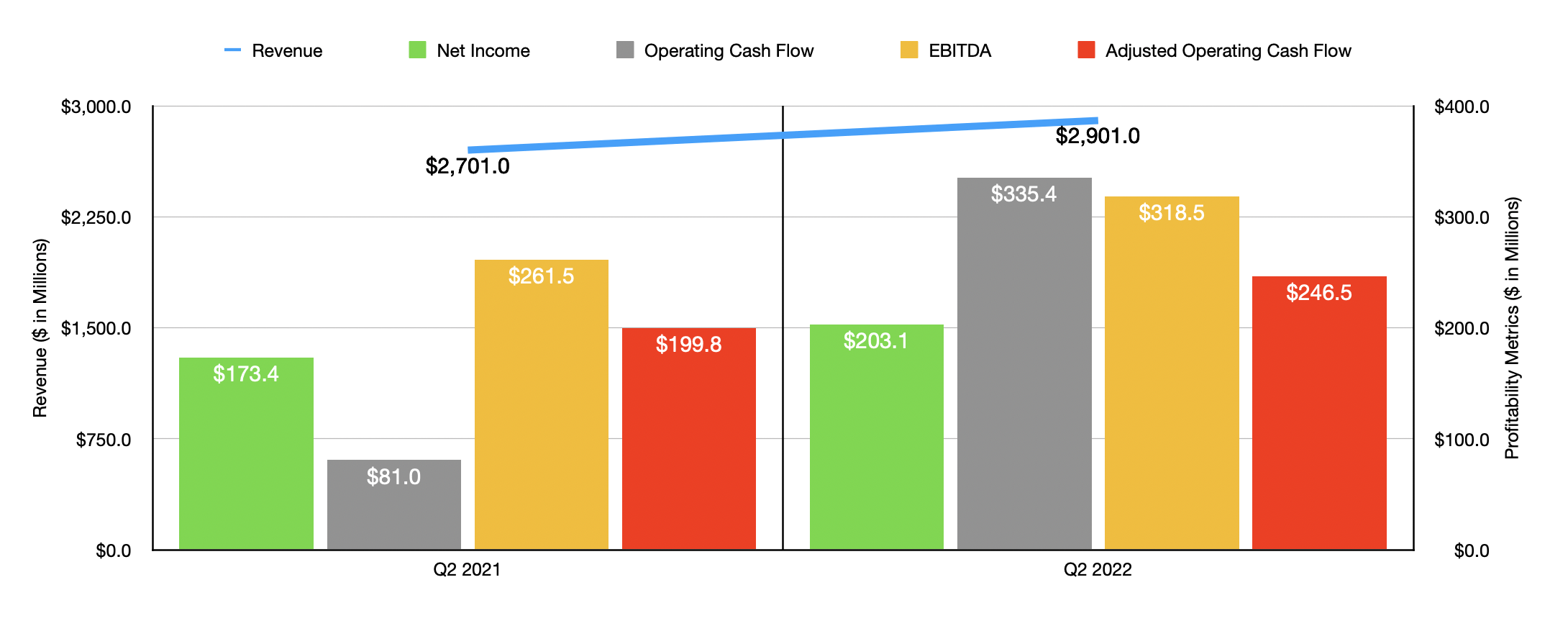

To be clear, this increase in share price was not unwarranted. When I last wrote about the company, we had data covering through the first quarter of the 2022 fiscal year. Today, that data extends through the second quarter as well. And what a quarter that was. During the quarter, the enterprise reported revenue of $2.90 billion. That represents an increase of 7.6% over the $2.70 billion generated the same quarter one year earlier. Management attributed this rise in revenue to three factors. First, and most importantly, was a 4% increase in prices on the products that it sold. The company also benefited to the tune of 1% from an increase in unit sales thanks to acquisitions completed since June of last year. And finally, it benefited to the tune of 2% from a rise in organic unit sales. On the sales pricing side, management said that one contributor was an improvement in the firm’s product mix of value-added products that are often sold at a fixed price. However, they also said that elevated end market demand and value-based selling initiatives helped as well. This is not to say that every portion of the enterprise performed well. Organic unit growth in the Construction segment of the company, for instance, was a robust 17%. That compared to a 7% decline in the Retail segment and a more modest 1% decline in the Industrial segment.

This rise in revenue, especially the portion associated with increased prices, helped the company’s bottom line significantly. Net income in the second quarter came in at $203.1 million. That stacks up nicely against the $173.4 million generated one year earlier. The company benefited here tremendously from an improvement in its gross profit margins from 15.6% to 17.4%, some of which was offset by higher selling, general, and administrative expenses relative to sales. The margin improvement was driven in large part by a decrease in lumber expense to the enterprise. In the second quarter, for instance, the price for random lengths framing lumber dropped from $1,284 per MBF (or thousand board feet) last year to $890 per MBF this year. And for southern yellow pine, the price declined from $1,041 per MBF to $736 per MBF.

Author – SEC EDGAR Data

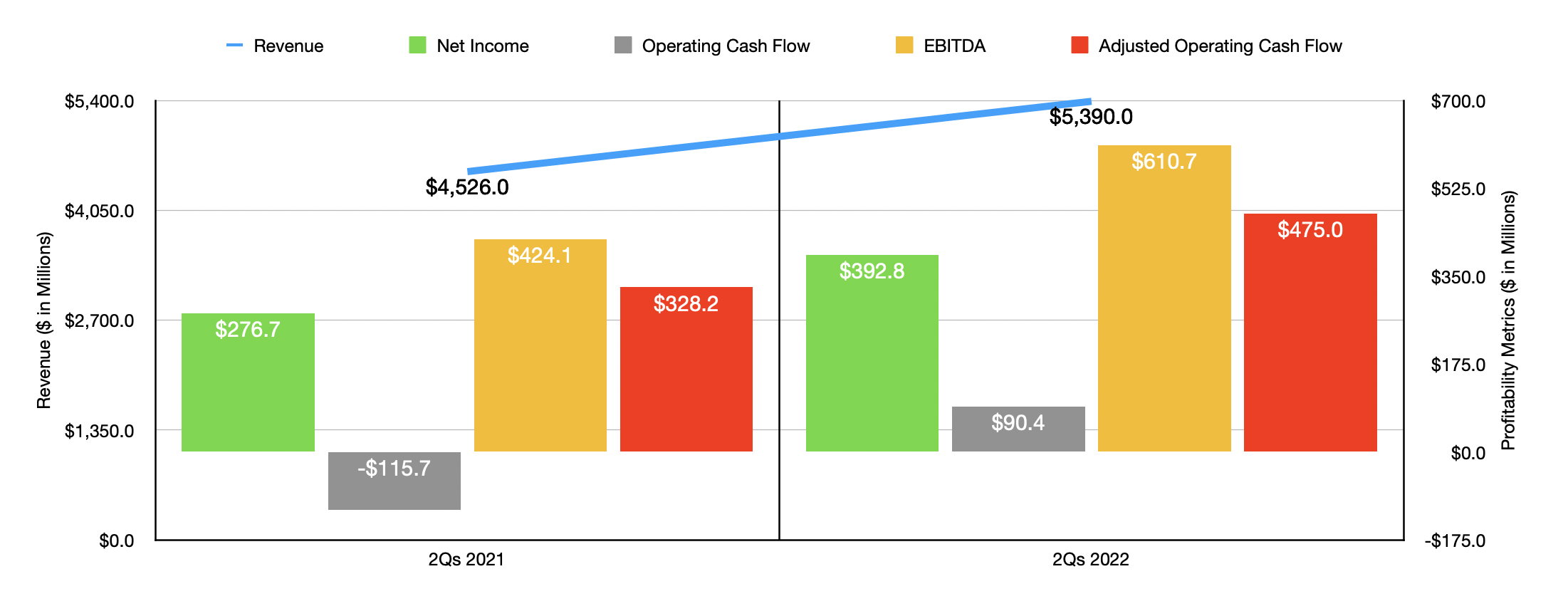

Naturally, this improvement in net income also translated to an improvement elsewhere. Operating cash flow for the company grew from $81 million in the second quarter of 2021 to $335.4 million at the same time this year. If we adjust for changes in working capital, the increase would have been more modest from $199.8 million to $246.5 million. Meanwhile, EBITDA for the company expanded from $261.5 million to $318.5 million. As you can see in one of the charts in this article, this strong bottom line performance for the company in the second quarter also helped the total results for the first half of the year as a whole. Unfortunately, we don’t know what to expect when it comes to the rest of the year. But if we were to use data from the first half of the year so far to project out what the rest of the year would look like, we should anticipate net income of $760.3 million, operating cash flow of $741.7 million, and EBITDA of $1.19 billion.

Author – SEC EDGAR Data

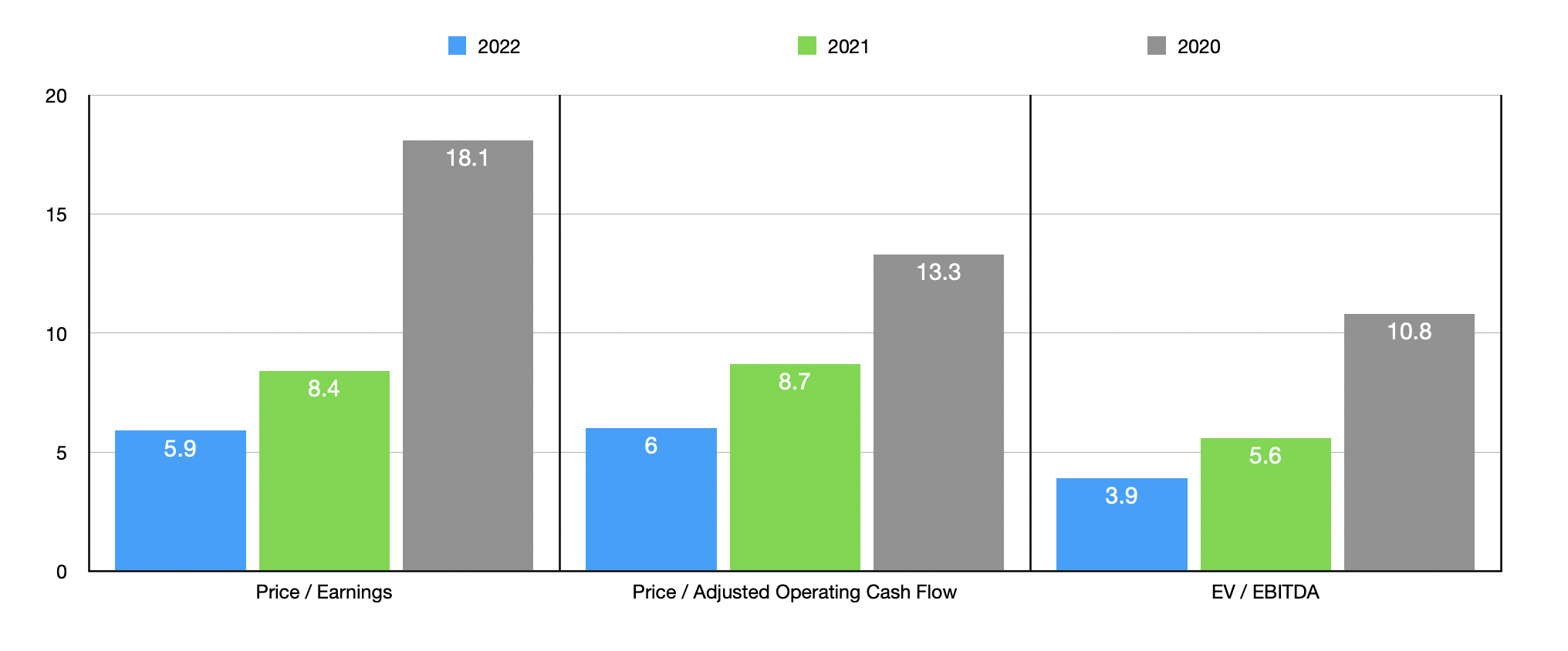

Using this data, we can easily value the firm. On a forward basis, UFP Industries is trading at a price-to-earnings multiple of 5.9. The price to operating cash flow multiple is only slightly higher at 6, while the EV to EBITDA multiple is remarkably low at 3.9. These numbers compare to the 8.4, 8.7, and 5.6, respectively, readings that we get if we use data from 2021. And if we were to use the data from 2020, these figures would be 18.1, 13.3, and 10.8, respectively. As part of my analysis, I compared the 2021 figures to the figures of five different businesses that are similar in nature. On a price-to-earnings basis, these companies ranged from a low of 9.7 to a high of 53.8. On a price to operating cash flow basis, the range is between 15.9 and 51.4. And using the EV to EBITDA approach, the range is between 7.1 and 129.7. In all three cases, UFP Industries was the cheapest of the group.

| Company | Price/Earnings | Price/Operating Cash Flow | EV/EBITDA |

| UFP Industries | 8.4 | 8.7 | 5.6 |

| Simpson Manufacturing (SSD) | 11.0 | 17.6 | 8.3 |

| Armstrong World Industries (AWI) | 20.9 | 23.4 | 12.7 |

| Zurn Elkay Water Solutions (ZWS) | 53.8 | 51.4 | 129.7 |

| Hayward Holdings (HAYW) | 9.7 | 19.0 | 7.8 |

| Resideo Technologies (REZI) | 9.7 | 15.9 | 7.1 |

Takeaway

The data shown so far for UFP Industries looks awfully promising. I understand, given the rise in interest rates that we have seen, high inflation, and concerns over the near-term future of the economy, why some investors will be hesitant to focus on a company like UFP Industries. But I see it as unlikely that results could get much worse than what they were in 2020. Even in that case, shares would likely be no worse off than fairly valued. This creates a favorable outcome most likely where the best case is a nice rise in share price while the worst case is a modest decline or even no decline at all for shareholders. Because of this, I have decided to keep my ‘buy’ rating on the company for now.

Be the first to comment