BreakingTheWalls/iStock via Getty Images

Thesis

United States Steel (NYSE:X) posted a robust Q2 earnings release that came in well ahead of the consensus estimates. Moreover, it suggested that the panic that sent X stock tumbling from March to June was overstated, coupled with recessionary fears.

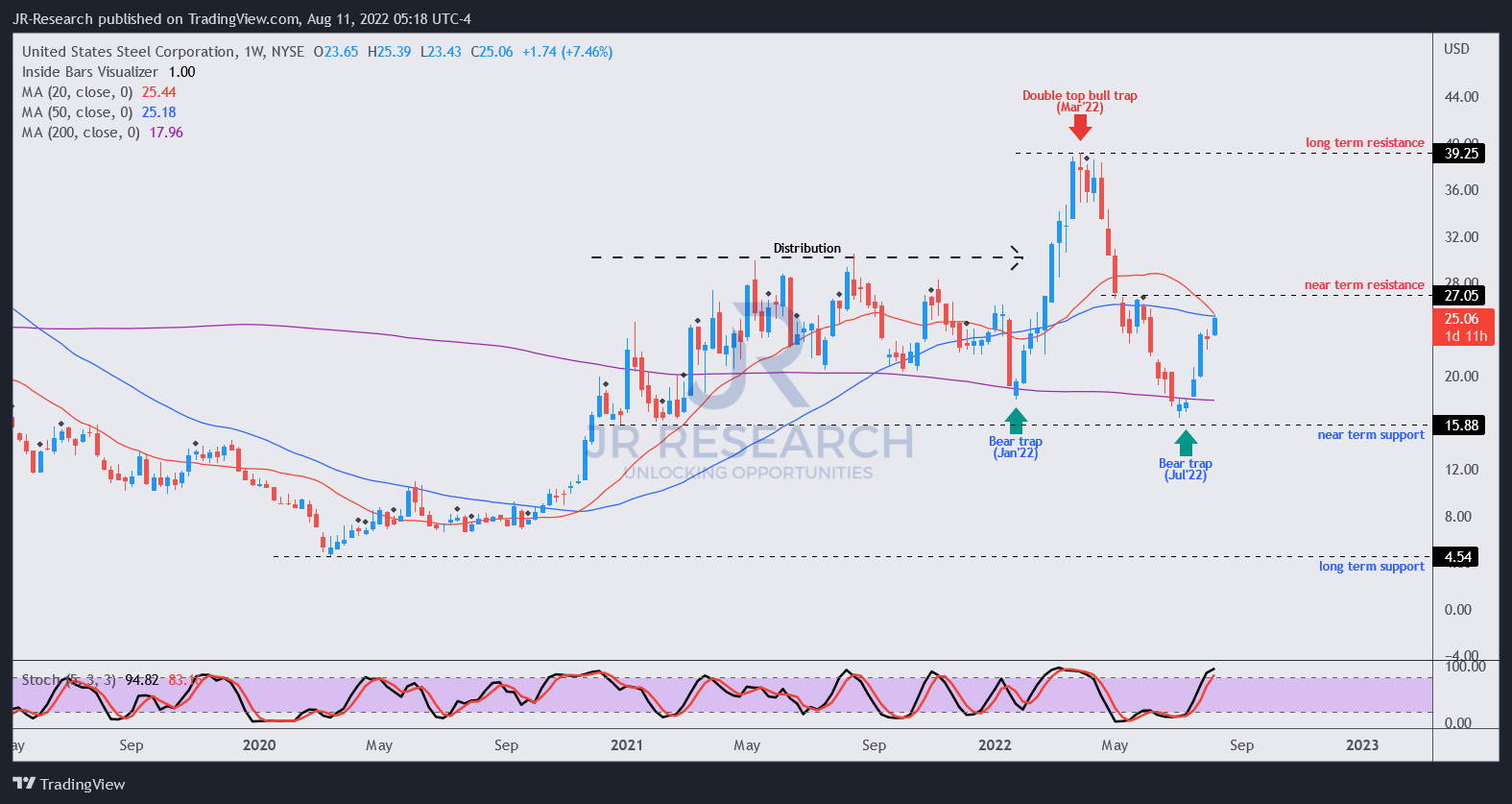

We noted that X was near its support in our previous article, which could help provide a short-term respite. Notably, it also formed a bear trap (indicating the market denied further selling downside) two weeks after our July article, as X staged a remarkable recovery since its July lows. While we had expected a near-term rebound, we didn’t expect the scale of it, as X outperformed the market significantly.

Notwithstanding, we do not encourage investors to add at the current levels as X has reached technically overbought levels. Also, we remain concerned about a marked drop in revenue and profitability metrics moving ahead, which could put further pressure on X to regain its 2022 highs.

Accordingly, we reiterate our Hold rating on X.

Superb Q2 Quelled Near-Term Fears

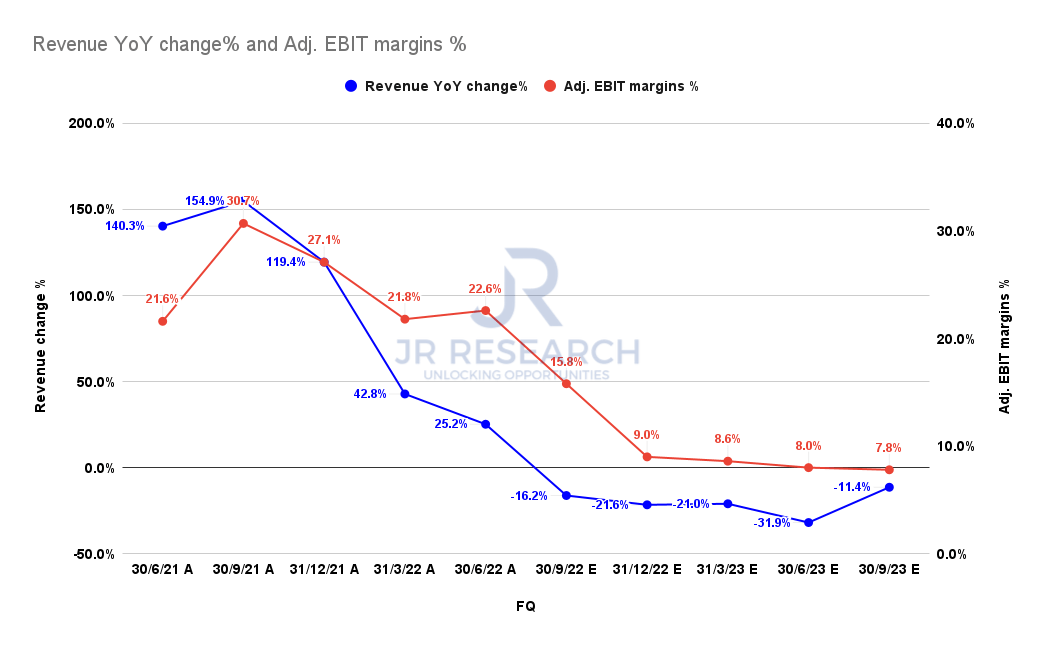

U.S. Steel posted revenue of $6.29B (up 25.2% YoY) and an adjusted EBITDA of $1.62B (up 26% YoY). The company also outperformed the consensus estimates markedly in Q2, demonstrating the strength of its diversified business segments. The company highlighted softness in consumer end markets but indicated strength in the energy markets. CEO David Burritt accentuated:

I think this diverse end market exposure really does keep us insulated from having too much dependence on just one set of customers. We got automotive with 30% to 35%. Construction, 15% to 20%. Tin, something like 15%. Appliance, 10%, energies, and line pipe to 10%. Importantly, we are uniquely positioned to serve the resurging energy market from our flat-rolled, mini mill and tubular segments. We continue to see growth in today’s order book for energy product while investing in capabilities to serve growing markets in the future. (U.S. Steel FQ2’22 earnings call)

U.S. Steel revenue change % and adjusted EBIT margins % consensus estimates (S&P Cap IQ)

Nonetheless, the revised consensus estimates (neutral) suggest that X’s revenue and profitability growth could moderate further through FY23. Therefore, we believe it’s important for investors to be cautious when considering adding exposure. Management also highlighted pressure from the current pricing dynamics. Outgoing CFO Christine Breves articulated:

The declining steel price environment through much of the second quarter and into the third quarter has kept some buyers on the sidelines. This is expected to result in sequentially lower EBITDA for our Flat-Rolled segment. Spot prices falling from high levels over the past several months are expected to negatively impact results in the third quarter. (U.S. Steel earnings)

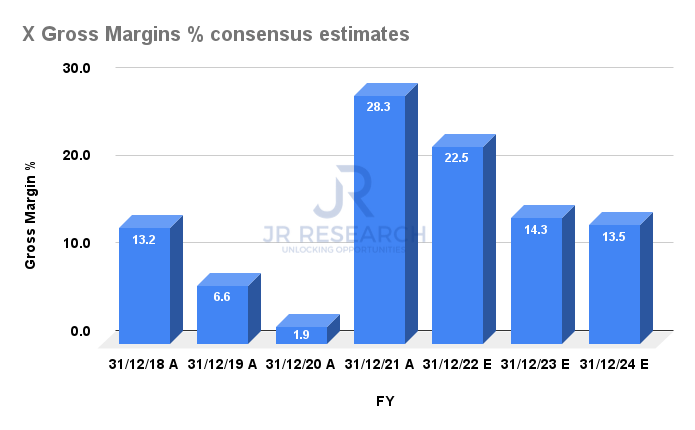

U.S. Steel gross margins % consensus estimates (S&P Cap IQ)

US Steel CapEx consensus estimates (S&P Cap IQ)

As seen above, U.S. Steel’s gross margins could continue to fall through FY24, impacting its bottom line. Furthermore, the company is also expected to be investing heavily through FY23, which could put further pressure on its ability to continue its attractive stock buybacks.

The company highlighted that it has exhausted its previous $800M stock repurchase authorizations and announced a new $500M authorization. With a market cap of $5.94B, the scale of the new authorization is quite significant. Notwithstanding, an analyst on the call sounded cautious about the buyback, coupled with high CapEx and a weaker macro environment. Burritt replied:

We will be opportunistic. We’re not going to commit to a certain amount by quarter, but we do feel very good where we are, and we’ll see how the economy unfolds and we’ll be, again, opportunistic within the framework. (U.S. Steel earnings)

Therefore, we believe that the company has reminded investors not to expect it to exhaust its new authorization with aggressive buybacks if the economic environment worsens, impacting its profitability.

Is U.S. Steel Stock A Buy, Sell, Or Hold?

X price chart (weekly) (TradingView)

X staged a bear trap on its medium-term chart two weeks after we published our previous article. But the scale of its recovery surprised us even though we expected a near-term recovery.

X is also closing in on its near-term resistance; therefore, we believe caution is warranted. Consequently, we do not encourage investors to chase the current rally.

We believe X is unlikely to retake its 2022 highs in the near term, given markedly falling revenue growth and profitability estimates. Therefore, an extended digestion period could occur before a sustained bottom in X could appear, lending credence to an attractive buying opportunity.

As such, we reiterate our Hold rating on X.

Be the first to comment