da-kuk/E+ via Getty Images

I reported in numerous Seeking Alpha articles that U.S. semiconductor sanctions are proving to be a catalyst for enhanced China growth. In a recent December 8, 2022 Seeking Alpha article entitled “No Evidence U.S. Sanctions Against China Are Working, Thanks To ASML,” I noted that a slowdown in China chip production was more a result of Covid lockdowns then sanctions.

Sanctions to prevent China’s ability to make 7nm and lower chips also haven’t worked, which I was the first to reveal back on May 18, 2022 Seeking Alpha article entitled “Applied Materials: SMIC Move To 7nm Node Capability Another Headwind.”

A recent article in Reuters reported that China is now pushing for a 1 trillion Yuan ($142 billion) economic package to further enhance its semiconductor industry.

Critically important, one of the comments in the article was that the “Chinese could just flood the market with these [28nm] technologies” by a Techinsights analyst. Incidentally, it was Techinsights that published a breakdown of the SMIC chip made at 7nm, but that was two months after my reveal in the above article.

In my article, I present a deep dive into China’s current semiconductor fab plans and the impact it will have on the global chip capacity by node. I will also analyze the Reuters report of a 1 trillion Yuan fab expansion and whether Techinsights’ suggestion of a flooded 28nm market is without merit, as it could have far-reaching ramifications.

Importantly, the only winners in these sanctions to date have been Chinese Equipment companies. It was discussed in a December 8, 2022 Seeking Alpha article entitled “No Evidence U.S. Sanctions Against China Are Working, Thanks To ASML” that:

- The mean growth for non-Chinese companies for the nine-month period between January 2022 and September 2022 was 11.2%, and Applied Materials’ (AMAT) exhibited a revenue growth of just 8.7% for 3Qs 2022 vs. 3Qs 2021, indicating underperformance against other non-Chinese WFE competitors.

- Importantly, the mean growth for Chinese equipment companies was 62.8%, indicating that Chinese equipment companies are gaining in the market, although their revenues are significantly lower than non-Chinese counterparts.

- Equally important, the top eight Chinese equipment companies all sell products that compete directly against AMAT.

Expanding China Fab Construction

Table 1 shows planned fab construction in China between 2022 and 2025 for chip construction at the 28nm node and above. These fabs are primarily foundries, a model that has been embraced in China because of the success of SMIC. Total fab spend is $67.566 billion.

Keep in mind that the recent U.S. Department of Commerce restrictions are meant to deter China’s access to and ability to make advanced chips at the following thresholds:

- Logic chips with non-planar transistor architectures (i.e., FinFET or GAAFET) of 16nm or 14nm, or below;

- DRAM memory chips of 18nm half-pitch or less;

- NAND flash memory chips with 128 layers or more.

The Information Network

Why Build 28nm and Larger Node Fabs?

One may ask why build fabs at 28nm when chip companies are only restricted by U.S. sanctions at 16nm and below? TSMC (TSM), which made the first 28nm fab in 2011 and has been making more, even into 2022, describes the reasoning as:

“The 28nm process technology supports a wide range of applications, including Central Processing Units (CPUs), graphic processors (GPUs), high-speed networking chips, smart phones, application processors (APs), tablets, home entertainment, consumer electronics, automotive, and the Internet of Things.”

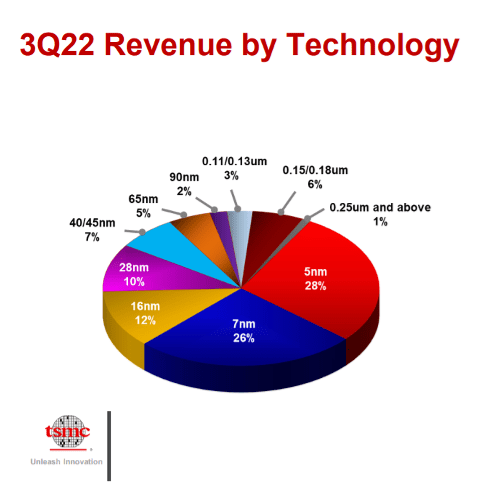

In fact, Taiwan’s TSMC, which dominates the IC foundry market with a 57% share, generated 10% of its revenues in 3Q 2022 from ICs made at the 28nm node, as shown in Chart 1, according to The Information Network’s report entitled “Hot ICs: A Market Analysis of Artificial Intelligence (“AI”), 5G, Automotive, and Memory Chips.”

TSMC

Chart 1

In addition to the 28nm node and below for TSMC, in the latest quarter TSMC generated 24% of its revenues from nodes above 28nm. This indicates that there are markets for Chinese fabs to produce devices at large dimensions even though ASPs (average selling prices) for the 32-90nm node range are 50% of the ASPs at the 28nm node and at the 90nm node ASPs drop to 30%.

- At 40nm, TSMC’s chips target smartphones, digital television (“DTV”), set-top box (Set-Top-Box), game and wireless connectivity applications.

- Its 65nm technology supports for a wide range of applications, such as mobile devices, computers, automotive electronics, IoT, and smart wearables.

- TSMC’s 130nm chips see broad application in consumer electronics, computers, mobile computing, automotive electronics, IoT, and smart wearables.

Analysis of Wafer Starts by Node

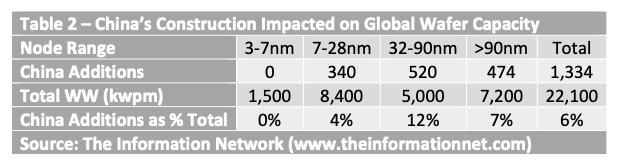

It is important to notice that of the total 1,333 kwpm (thousand wafers per month) planned in Table 1, just 340 kwpm are at 28nm and are planned by Semiconductor Manufacturing International Corporation (SMIC) (OTCQX:SIUIF). An additional 520 kwpm are planned for the 32-90nm node range. The final 474 kwpm will be from new fabs above the 90nm node.

Table 2 sums the impacts of the China fab additions, which increases China’s total by 6%, but with a 12% growth impact at the 32-90nm node range. At the much ballyhooed 28nm node, China additions from SMIC will account for just a 4% increase.

The Information Network

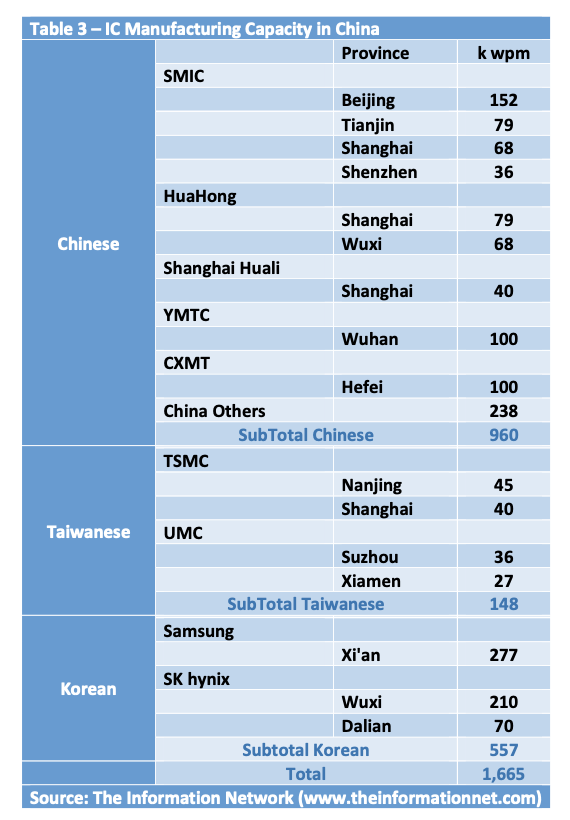

Table 3 shows current IC manufacturing capacity in China for domestic Chinese manufacturers plus Korean and Taiwanese. Total production capacity is 1,665 kwpm. While the 1,334 kwpm additions from new China fabs will result in only a 6% increase in Global capacity, it will:

- Nearly equal the total current 1,665 kwpm capacity inside China.

- Nearly double the domestic Chinese 960 kwpm capacity

- Double the foreign 705 kwpm capacity inside China

The Information Network

Also, it is important to note that U.S. sanctions are imposed on Korean memory companies Samsung Electronics (OTCPK:SSNLF) and SK Hynix (OTC:HXSCL), with a one-year waiver to keep upgrading their fabs in China before they will not be permitted to purchase advanced equipment.

Samsung’s and SK Hynix’s fabs in China produce a substantial portion of the global 3D NAND and DRAM supply. Samsung makes some 40% of its 3D NAND chips in China, whereas SK Hynix produces around 40% of its DRAMs

Investor Takeaway

Currently we don’t know whether the Reuters article about a 1 trillion Yuan ($142 billion) investment in fabs by the Chinese government is real, as they were from un-named sources. On the basis of announced fabs to be constructed in the next few years (Table 1), that total fab spend is $67.6 billion. Yet it hardly moves the needle, increasing China’s additions by just 6% of the global wafer capacity and just 4% of 28nm.

If the Reuters article is correct, we can use my analysis in this article to assume that a fab spend of $142 billion, which is 2X the current fab spend, will be 2X the impact on the global capacity. Thus, China additions would add 12% to the global capacity. This clearly would not be sufficient to “flood the market with cheap 28nm chips,” as has been suggested.

Another “rumor” is that Huawei, the first company that faced U.S. sanctions, has reportedly filed a patent for an EUV lithography system, which has been sanctioned and would enable sub-5nm chip production, and would compete directly against ASML. I will continue to monitor the development.

This small growth is another indication that U.S. sanctions are minimally working, but only serve as a catalyst for China to promote its drive for self-sufficiency in chip making. This expansion in fabs follows an expansion of Chinese chip companies in purchasing fab equipment from Chinese companies. While the growth in these domestic equipment companies has been impressive, it has hardly moved the needle for overall equipment purchases by U.S. and other foreign companies. I’ve published numerous Seeking Alpha articles on this topic, and the most recent is from December 8, 2022 entitled “No Evidence U.S. Sanctions Against China Are Working, Thanks To ASML.”

For investors, the greatest erosion is with equipment companies, particularly Applied Materials, with the greatest exposure to revenues coming from China. Chinese semiconductor companies are reacting to sanctions and threats of sanctions by buying equipment from domestic suppliers such as:

- ALD – Naura

- CMP Huahai Qingke Co

- Epitaxy – Naura

- PECVD – Piotech

- PVD – Naura

- RTP – Mattson (parent company Beijing E-Town)

- Dielectric Etch – AMEC

- Conductor Etch – Naura

Each of these Chinese companies make equipment that competes directly with AMAT. Significantly, the mean growth of these companies for the 3Qs of 2022 over 3Qs of 2021 increased 62.8% while AMAT has grown 8.7%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment