Manufacturing’s not that important

We do all have to remember that manufacturing is only about 10% or so of most advanced economies – more in China as it’s not so advanced. Thus what happens in manufacturing is not the be all and end all for the economy. It’s services that matter there.

We also, in the coronavirus recession, have some more detailed points about the two sectors. Customer facing services – the bars, entertainment business etc – are entirely shafted by social distancing rules. Manufacturing is hurt but workarounds are easier.

On the other hand manufacturing relies upon complex and globe spanning just in time supply chains in a manner that services really don’t. As disruption repeats around the world on different timescales then we can expect different parts of those chains to be disrupted at different times. Again, services we’d expect to find it easier to repair their supply chains.

That is, we’d expect, once social distancing rules are lifted, services to bounce back faster than manufacturing. Even if they do get hit harder by the rules in the interim.

That rather means that the effects upon manufacturing – in time terms only – are the worst we can expect, not the best.

China’s official manufacturing PMI

For the second month running China’s manufacturing PMI shows very modest expansion. Not, sadly, expansion from where we were before this all started for these figures are month on month. Rather, expansion from the depths of the problem:

China’s economic recovery seems to have already lost pace, as the official manufacturing PMI in April dropped to 50.8 from 52 in March.

(China official manufacturing PMI from Moody’s Analytics)

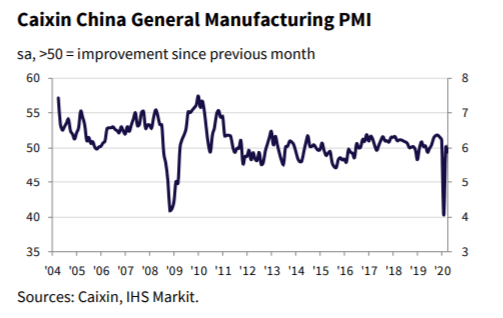

China’s private sector manufacturing PMI

We also have the private sector reading of the same manufacturing PMI:

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to provide a single-figure snapshot of operating conditions in the manufacturing economy – slipped from 50.1 in March to 49.4 in April, to indicate a renewed deterioration in operating conditions.

And

(China manufacturing PMI from IHS Markit)

Those are slightly different, yes, but the differences are only at the margin. And that the private sector and official numbers are very much the same does give us confidence, no? You know, given our general wariness of Chinese economic numbers.

However, the thing to note from both of these. The domestic market is doing very much better than the export one. Given that Europe and North America are largely closed right now and have been for at least the past month that makes sense too. But note what this means for our worries about recovery. The domestic manufacturing scene does seem to get its act back together quite quickly. Which is good, of course.

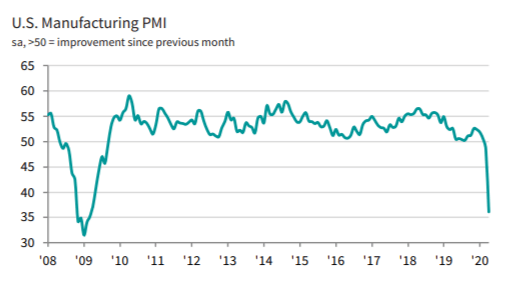

US manufacturing PMI

We also have the two different measures of the US manufacturing PMI. First, from the Institute for Supply Management:

“The April PMI® registered 41.5 percent, down 7.6 percentage points from the March reading of 49.1 percent.

Every component went to pot except:

The Supplier Deliveries Index registered 76 percent, up 11 percentage points from the March reading of 65 percent, limiting the decrease in the composite PMI

And that’s not exactly great, as it indicates slower deliveries. Not a great way to measure things to my mind but there we are.

(ISM manufacturing PMI from Moody’s Analytics)

(ISM manufacturing PMI from Moody’s Analytics)

We get a rather worse reading from the competing source, IHS Markit:

The seasonally adjusted IHS Markit final U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) posted 36.1 in April, down from 48.5 in March and the previously released ‘flash’ figure of 36.9. The headline reading was the lowest for just over eleven years, despite being buoyed by the greatest deterioration in suppliers’ delivery times since data collection began in May 2007 (ordinarily a signal of improving manufacturing demand but currently the result of virus-related supply constraints).

(IHS manufacturing PMI from IHS Markit)

The two measures are at least both pointing in the same direction which is not always the case.

So, what can we make of all this?

We’ve already seen what has happened in other paces as the lockdown arrives so there’s no surprise that there’s a significant fall in production and thus GDP. The thing that influences stock and bond values is how long is this going to last? Then, once it’s over, how fast is the recovery going to be?

My assumption has been that it will be short and fast respectively. From what we see in China, or from China, the short is true. It is, at maximum, a two month disruption. What happens after that, well, we’re still waiting to see really.

We can see that things don’t continue to get worse. Don’t forget, the PMI going back up to around 50 doesn’t mean we’re back to where we started from, only that there’s a slight expansion on the previous month. We can, should perhaps, explain that as the export markets going through their closedowns presently and so we’ll only really see when Europe and the US are open again. Perhaps the June numbers that is, maybe July.

What we can say with confidence is that the shutdown doesn’t set off a cascade of failure, rather, that production falls to a certain level that at worst stabilized. This is still better than the worst predictions out there.

My view

As Keynes said I should be I’m willing to change my mind when the facts do. So far I see no such facts which change my basic opinion, a deep recession caused by the lockdowns but a short one with a swift recovery.

I don’t say we’ll be back to where we were by the end of the year, indeed would insist we won’t be, we’ll be at least a few percent down on the whole year. But the figures for this next couple of months in the US are going to be horrendous in terms of GDP loss. My current thinking is that much of that, but not all, will be made up again by the end of the year.

The investor view

This stays as it has been recently. Big safe and boring is our friend here. Steady stocks with decent dividends. Risk rises in price in a crisis and it’s much later in the recovery that we want to switch back to the more exciting stocks.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment